Uninsured and Underinsured Motorist Insurance (Claims and Settlements)

Justin Ziegler, Lawyer

Today I’m going to show you if uninsured or underinsured motorist insurance coverage will pay your personal injury claim.

I’ll also give you tips on how to potentially increase your uninsured motorist (UM) payout.

Let’s start by looking at some frequently asked questions (FAQs) about UM coverage.

We’ll then look at some of my many uninsured and underinsured motorist settlements.

Here are some frequently asked questions about uninsured motorist insurance settlements:

What is uninsured motorist coverage?

Uninsured motorist (UM) coverage pays you for personal injury caused by the negligence of a driver of an uninsured motor vehicle. It also covers wrongful death damages.

These damages can often include pain, suffering, medical bills, lost wages and more.

Similarly, underinsured motorist coverage pays you if a careless underinsured driver caused your injury.

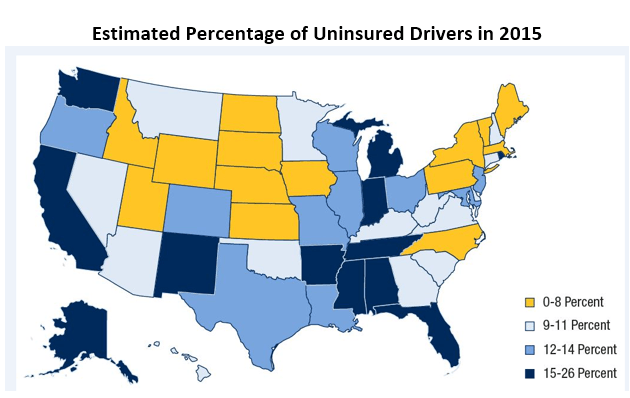

Unfortunately, there is a large percentage of uninsured drivers in each state. Just look at this map below.

In a state like Florida, between 15 to 26 percent of drivers are uninsured. That is off the charts!

In order for you to be entitled to UM coverage, you must be an insured under a policy that has UM coverage.

What is the average uninsured motorist insurance settlement?

Under $15,000. Fortunately, most car accidents don’t result in bad injuries. And minor injuries usually result in small payouts.

The most common complaint after a car accident is whiplash, which usually doesn’t result in a huge settlement. This is especially true if there is minor damage to the cars involved in the accident. If the cars were not badly damaged, most uninsured motorist insurers make a small offer for whiplash. GEICO, Progressive and State Farm typically won’t offer much for an uninsured motorist bodily injury insurance claim for whiplash if there is no (or very little) damage to the vehicles.

If you want a big payout in a minor impact whiplash case, you’ll likely have to take the case to trial. There, you’ll hope for the best. However, it usually costs at least $10,000 to get an uninsured motorist insurance case to trial.

Also, in many uninsured motorist insurance claims, the injured person has already received payment from the at fault driver. If this occurs, the uninsured motorist insurer is entitled to a credit for any payment from the at fault driver. This results in a smaller uninsured motorist settlements.

On the other hand, if you broke a bone in the car accident, the average uninsured motorist insurance settlement is usually above $15,000. If you’ve had surgery to fix the broken bone, the average settlement is often $100,000 (or more). This assumes that there is enough uninsured motorist insurance to pay for the fair value of the case.

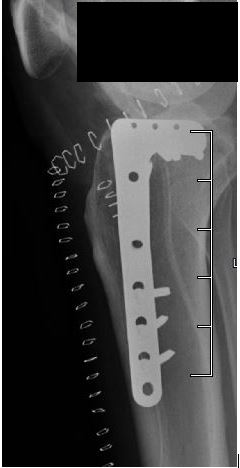

In the photo below, you’ll see my client who broke his leg in a car crash. I settled his claim against his underinsured motorist insurer for for $200,000. I settled the entire case for $300,000. He had surgery on his broken leg.

How much can I get from an uninsured motorist claim?

You can get up to the uninsured motorist (UM) bodily injury limits. This is for any UM policies to which you are an insured.

Some states (like Florida) that have stacking and non stacking uninsured limits. In the case of stacked uninsured motorist bodily injury coverage, you may be able to get more than the UM limits on one car.

With stacked UM coverage, sometimes you add the UM limits from more than one vehicle. This gives you more uninsured motorist coverage.

In a perfect world, your UM insurer should offer you the fair value of your UM claim. However, most of the time they do not. Uninsured motorist insurance companies often lowball you with a small offer. Sadly, they do whatever they can to save money.

To win the uninsured motorist bodily injury policy limits, your UM claim needs to be worth the limits.

In some cases, you may be able to get more than the uninsured motorist insurance limits if the insurer acts in bad faith. I talk about this later in this article.

Stacking uninsured motorist coverage covers you anytime an uninsured or underinsured vehicle hits you. Stacking coverage is much broader than non-stacking UM coverage.

In fact, stacking UM coverage would cover you if an uninsured car hit you while you were in a submarine.

How long does it take to settle an uninsured motorist claim?

It varies from a case to case. That said, there are two factors that determine the time that it takes to get an uninsured motorist bodily injury settlement. They are how badly you are hurt, and the amount of the UM insurance limits.

All things equal, the worse your injury, and the lower the uninsured motorist coverage limits, the faster the settlement.

Why?

Because the uninsured motorist bodily injury insurer has more pressure to pay. They don’t want to keep an uninsured motorist claim open if they know that they will eventually have to pay the limits. It’s in their best interest to settle the UM claim if it is worth more than the limits.

But why?

Because uninsured motorist insurers don’t want to get sued.

Now:

If you don’t have a lawyer, you can expect the UM insurer to delay any payout. My advice is to get an attorney as soon as possible if you have a serious injury and want to make an uninsured motorist claim.

Which uninsured motorist (UM) insurance payouts are the biggest?

The largest UM insurance payouts are usually those where the claimant has had surgery. Just look at my five biggest uninsured motorist insurance settlements. In all of them, the injured person had surgery to repair a broken bone.

It’s no secret that surgery cases have a higher full value for settlement purposes. And uninsured motorist bodily injury insurance cases are no exception.

This is for three reasons. With surgery, the pain and suffering award is usually much higher. Also, surgery results in higher medical billed charges. Many surgeries also leave a scar, which adds value to the case.

Why would you reject uninsured motorist coverage?

The only benefit of rejecting uninsured motorist coverage (UM) is that your car insurance premium will be lower. Other than that, it is a bad decision to reject UM coverage.

Even someone who has the best other insurance coverages can benefit by getting uninsured motorist coverage.

For example, let’s assume that someone has long term disability coverage, long term care insurance, and health insurance. This individual can still benefit with UM coverage. This is because uninsured motorist coverage fills it gaps that other insurance does not cover.

Here is how:

Long-term disability (LTD) insurance usually only cover 60% of your income when you have become seriously injured. If you have uninsured motorist coverage, it pays the 40% of your income that LTD insurance does not cover. If you are in a bad accident, that 40% can be a huge benefit to you.

However, the reality is that most Americans don’t have long term disability insurance. That means that uninsured motorist bodily injury coverage will often pay 100% of your lost wages from an accident. Additionally, many Americans are uninsured. Therefore, UM coverage often pays for medical bills that are due to a car accident.

How do you find out the at fault driver’s insurance limit?

You send a letter to the careless driver’s insurer asking for the driver’s bodily injury liability coverage limits. (The letter should typically ask for additional information but that is outside the scope of this article).

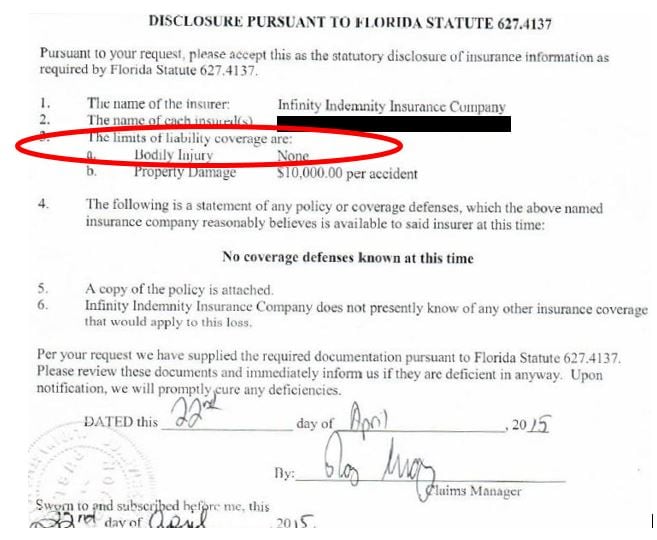

The above image is an insurance disclosure where the insured didn’t have any bodily injury liability insurance. Unfortunately, all too often drivers have no BIL insurance.

Can you win more than the UM insurance limits in your Florida case?

Yes, but you need two things to happen.

The first involves the state where the UM policy was issued. The good news is that Florida has more generous UM bad faith laws than some other states.

Florida has good UM bad faith laws but you need to follow a specific procedure. Otherwise, you can’t get paid above the UM insurance policy limit.

In Florida, you need to file a civil remedy notice (CRN) of insurer violation for the UM insurance company to be liable above the limits. You also need to send the CRN to the uninsured motorist insurance company. The UM insurer then has 60 days to pay you the limits. If they pay you in 60 days, they don’t owe you money above the UM limits.

If you’re dealing with UM coverage from another state, the other state’s bad faith will apply to the UM portion of that claim. See Higgins v. W. Bend Mut. Ins. Co., 85 So. 3d 1156 (Fla. 5th DCA 2012).

Some sates allow bad faith claims against UM coverage. Others don’t. And even for some states that allow bad faith, the damages are capped at certain amounts. And some are much less generous than Florida.

The second thing you’ll need is for the UM insurer to have acted in bad faith. Basically, they need to have not settled the case when they could and should have.

If a driver caused your crash but left the scene, can you make an uninsured motorist insurance claim?

In Florida, most policies include vehicles operated by hit-and-run drivers and “phantom” vehicles in the definition of “uninsured motor vehicle.” This is true even if the at fault vehicle cannot be identified, or physical contact did not occurr. Brown v. Progressive Mutual Insurance Co., 249 So.2d 429 (Fla. 1971); Denoia v. Hartford Fire Insurance Co., 843 So.2d 285 (Fla. 3d DCA 2003); Taylor v. Phoenix Insurance Co., 622 So.2d 506 (Fla. 5th DCA 1993).

This means that most people injured in Florida can make a claim for uninsured motorist insurance (if its available) even if a hit and run driver left the scene. The same is true if a driver did something wrong but did not strike you or your vehicle.

On the other hand, if you are visiting Florida from another state and were injured by a hit and run vehicle or phantom vehicle, your out of state policy may require physical contact to provide uninsured motorist benefits. In this instance, you or your lawyer needs to review your auto insurance policy.

If your policy does not require physical contact, it may require an independent witness who can confirm that the other vehicle caused your accident.

As promised, we’ll now look at some of my many uninsured motorist insurance settlements.

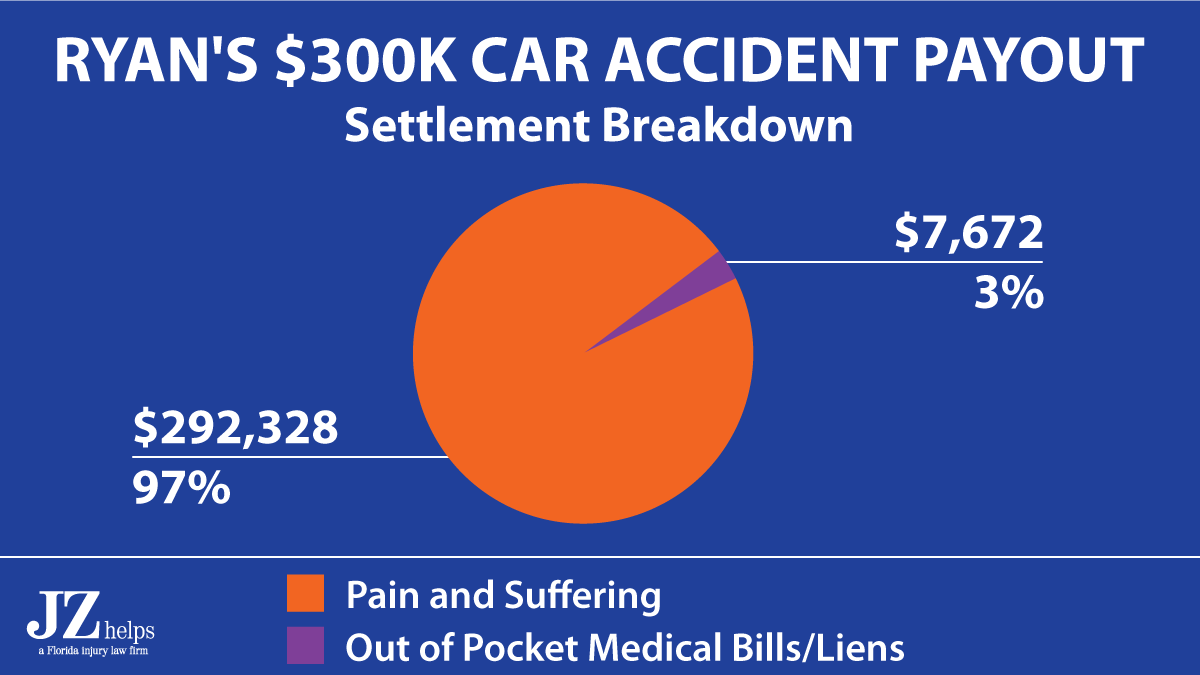

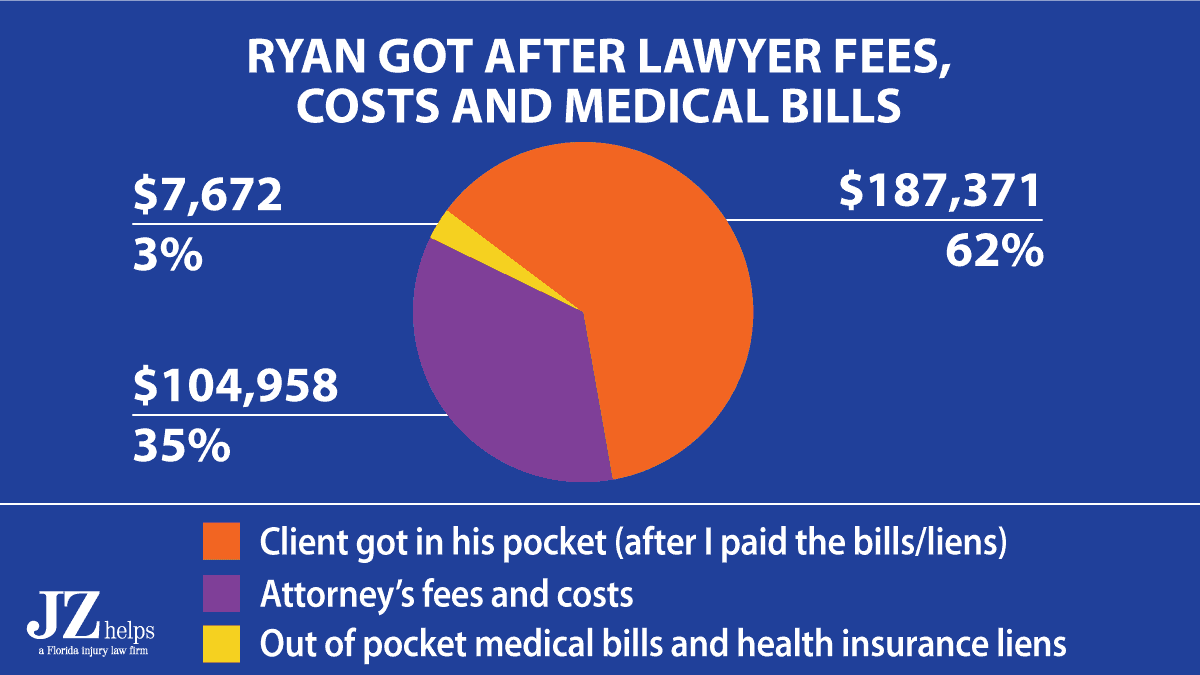

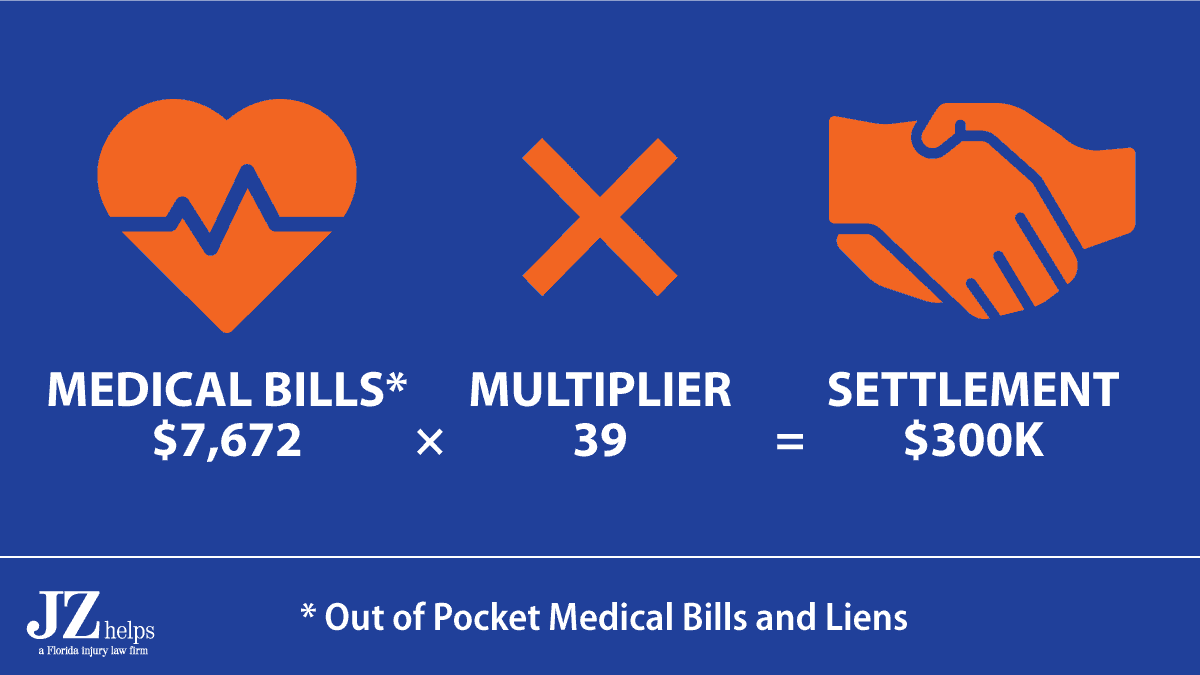

$300K Settlement After Suing Underinsured Motorist and UIM Insurance Company

Ryan lived in Georgia. However, he was in Florida for a business trip. While in Florida, Ryan rented a car from Avis rental car.

Ryan was driving the rental car in Clearwater, Pinellas County, Florida. When doing so, another car was coming in the opposite direction.

Allstate insured the driver who received a ticket for causing the crash. They paid his $100,000 BIL insurance limits.

In Georgia, Ryan owned a car. Travelers Insurance Company insured it. In fact, Ryan had underinsured motorist insurance on his car.

I explained to Ryan the possible benefit of suing the uninsured motorist insurance company. He gave me consent to sue. I sued Travelers in Pinellas County, Florida.

After suing the underinsured motorist and Travelers, we settled the entire case. Specifically, Travelers paid us $200,000 to settle Ryan’s uninsured motorist insurance lawsuit. This is much larger than the average underinsured motorist settlement.

Specifically, on how Georgia uninsured motorist insurance works for a Florida car accident.

In addition, the at fault driver died. I made a claim against his estate.

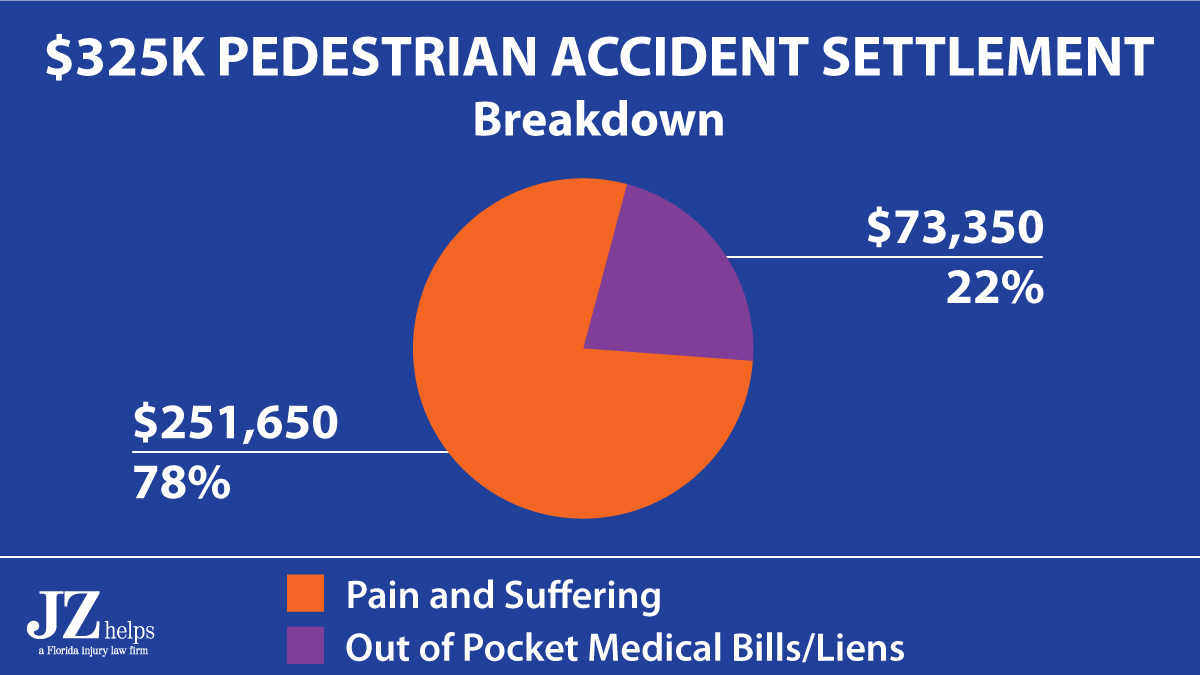

$100K Underinsured Motorist Coverage Settlement ($325K Total Payout)

Here is a short video about this settlement:

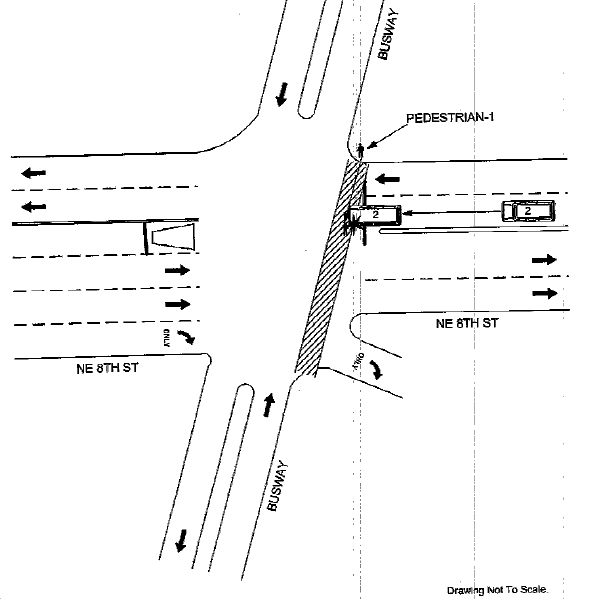

A Switzerland resident was in Miami for vacation. He had rented a car from Alamo Rent a Car. A federal government employee was driving a rental car in Miami, Florida.

While the Swiss man was standing next to his rental car, the driver hit him. As a result of the impact, the pedestrian fractured his leg bone (tibia). Shortly after the accident, the international visitor got a free consultation with me.

The driver rented a car with Hertz Car Rental. At the time, the federal government had a contract with Hertz that gave drivers $100,000 in bodily injury liability (BIL) coverage. Philadelphia Indemnity Insurance Company insured Hertz. I made a claim with Philadelphia. They paid me the $100,000 BIL limits.

When my client rented a car with Alamo, he purchased liability coverage. This means that he was also entitled to $100,000 of uninsured motorist bodily injury coverage. Ace American Insurance Company insured his rental car.

I made an underinsured motorist claim with Ace American

I argued that the government car was “uninsured” since the federal government is self-insured. Therefore, I argued that my client had an underinsured motorist claim against Ace American.

However, Ace American Insurance Company is likely most insurance companies. They are cheap. They did not pay. In fact, they did not offer me a penny.

Next, I filed a civil remedy notice of insurer violation. They hired attorney Dan Santaniello (Luks & Santaniello) to defend them. Instead of suing the uninsured motorist insurance company, I gave it chance to settle for $100,000 limits. About 60 days later, Ace paid me the $100,000 UM limits. This is much bigger than the average underinsured motorist settlement.

I then sued the United States of America because the federal employee driver was underinsured. During the lawsuit, I settled with the United States government for $125,000.

The total settlement against all parties was for $325,000.

When the insurance companies paid this claim, I estimate that 78% of the settlement was for pain and suffering. The rest was likely designated for medical bills.

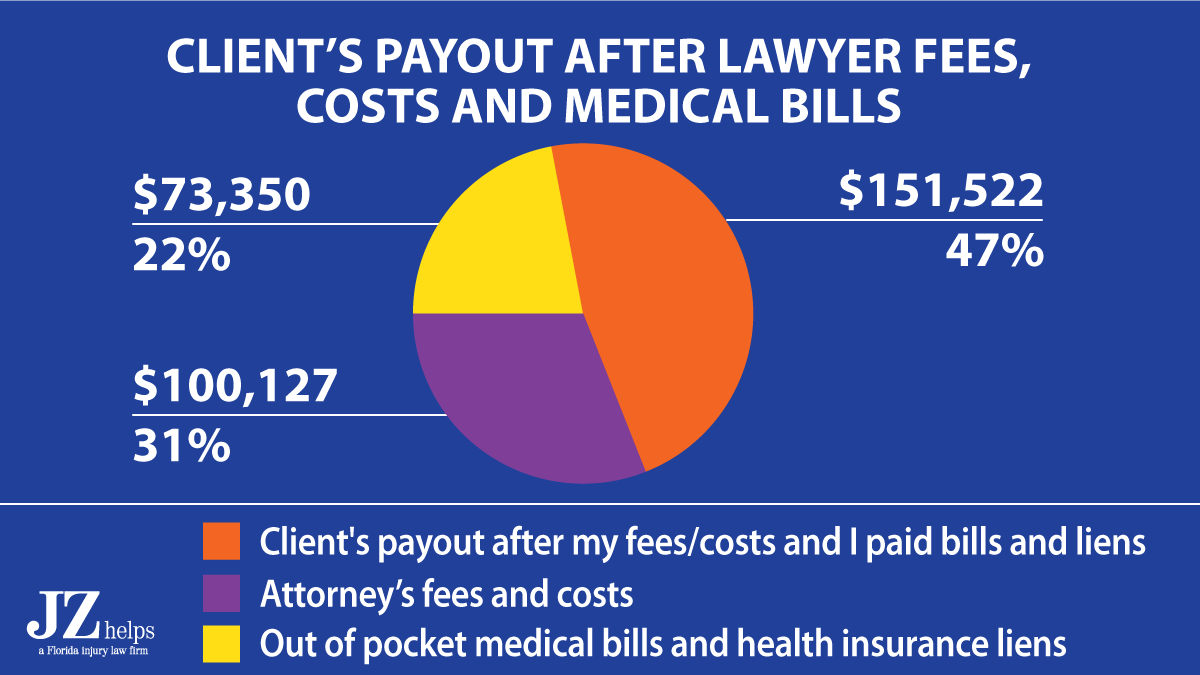

After my attorney’s fees, costs and paying the workers’ compensation lien and out of pocket medical bills, my client got a check for $151,522.

Take a look at the breakdown:

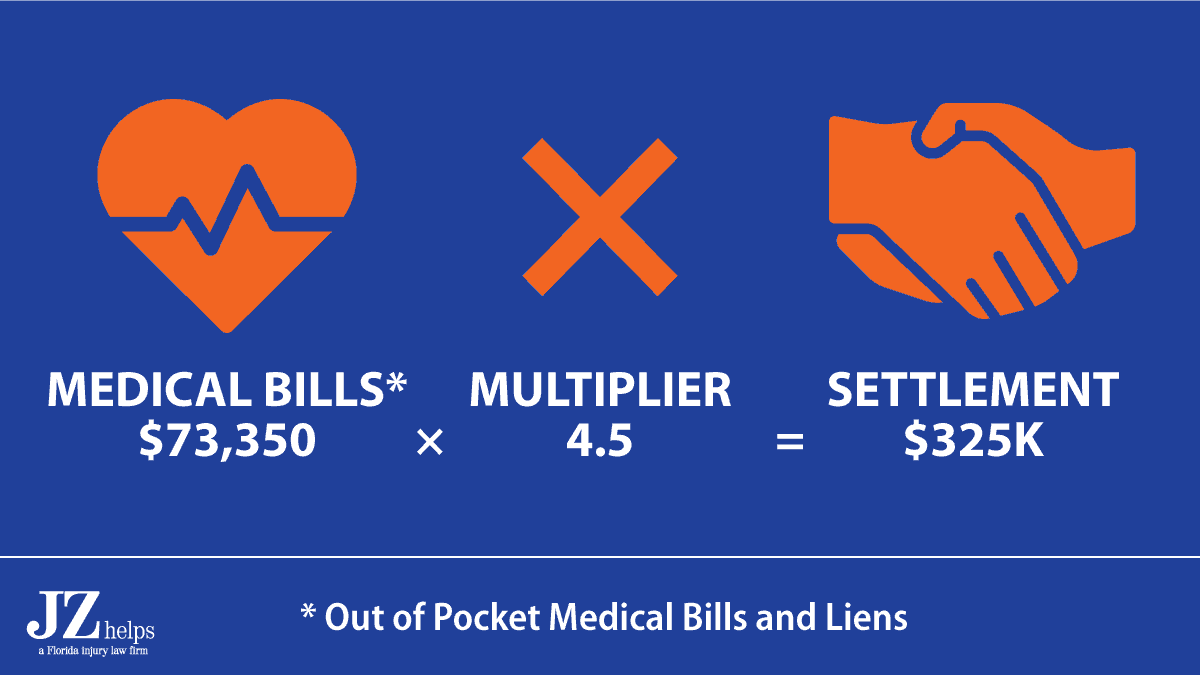

The total $325 payout was about 4.5 times my client’s final health insurance lien that we paid back.

Most uninsured motorist bodily injury insurance settlements for a pedestrian hit by a car are not this high. This is because most car accidents don’t result in a broken bone and surgery.

A woman was a passenger in a car on a highway in Bonifay, Florida. An uninsured car hit them. After the accident, the passenger had shoulder pain. She reached out to my office for a free consultation.

I spoke with her. After we spoke, she hired me. She claimed the the crash caused or worsened her rotator cuff tear.

She made a claim against her UM insurer, and the UM insurer of the car that she was in (“host car”). Nationwide Insurance Company insured each.

Nationwide paid the host car’s $100,000 UM insurance limits, and $30,000 of the passenger’s UM insurance policy. The total settlement was for $130,000. I was able to get this settlement without suing the underinsured motorist or the insurance companies.

Uninsured Motorist Claim Leads to $150K Total Settlement

Ron (not real name) was a passenger in a car in Miami, Florida. Another car was heading in the opposite direction. The other car made a left hand turn. They crashed.

Paramedics came to the scene. An ambulance took Ron to the hospital. After Ron left the hospital, he contacted my office. After I gave him a free consultation, he hired me.

Progressive insured the careless driver with $50,000 in bodily injury liability coverage. Progressive paid its $50k limits to settle. They did so without me suing the underinsured driver.

The pedestrian was a named insured on a car insurance policy with $100,000 in UM coverage with Progressive. Without me suing the underinsured motorist insurer (Progressive), it paid me $100,000 UIM insurance limits.

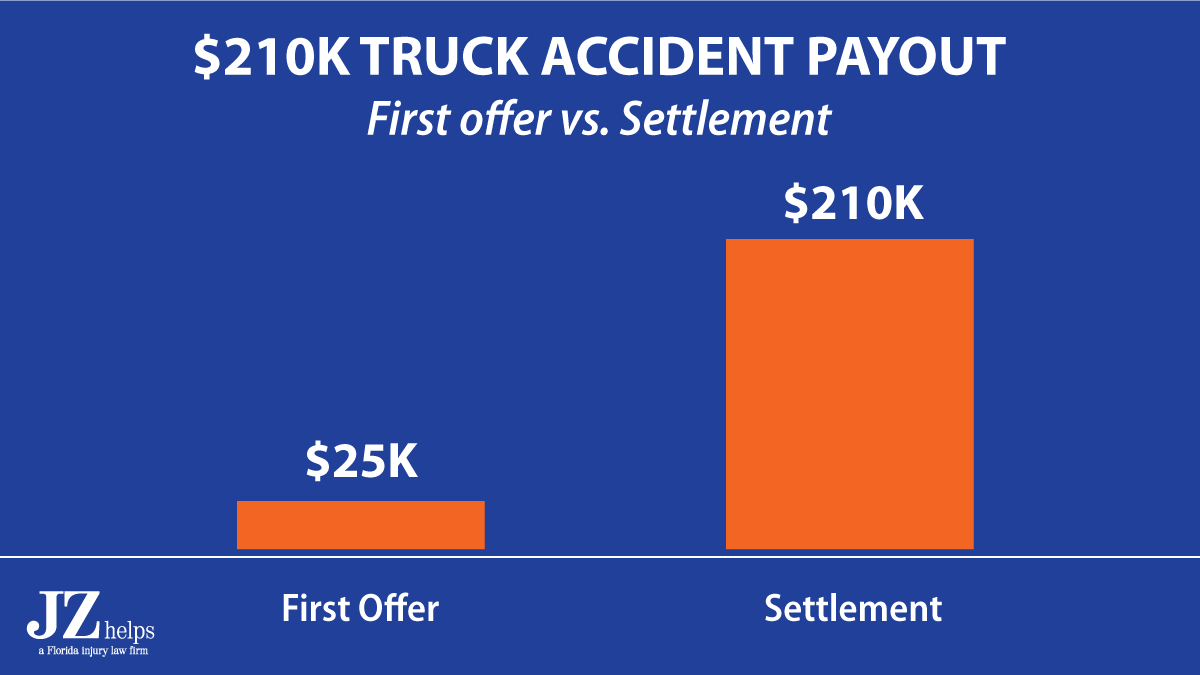

$10K Uninsured Motorist Bodily Injury Payout (Part of $210K Total Settlement)

Bob (not real name) was driving a truck for work. The front of his truck smashed into the back of a truck that Mike was driving for work. In the photo above, you can see the front of Bob’s truck.

Mike hurt his shoulder. Bob’s employer, a trucking company, had a $2 Million dollar BI policy with a $250,000 self-insured retention with Travelers Insurance.

We argued that the trucking company was “uninsured” under Florida law, since the trucking company had a self-insured retention.

Travelers first offer was $25,000. Travelers paid $200,000 to settle my client’s personal injury claim.

Mike had a $10,000 of Progressive UM insurance on his personal car. Even though Mike was driving a work vehicle, Mike’s Progressive Insurance paid the truck driver its $10,000 UM limits.

This chart shows the difference between the first offer and the settlement amount.

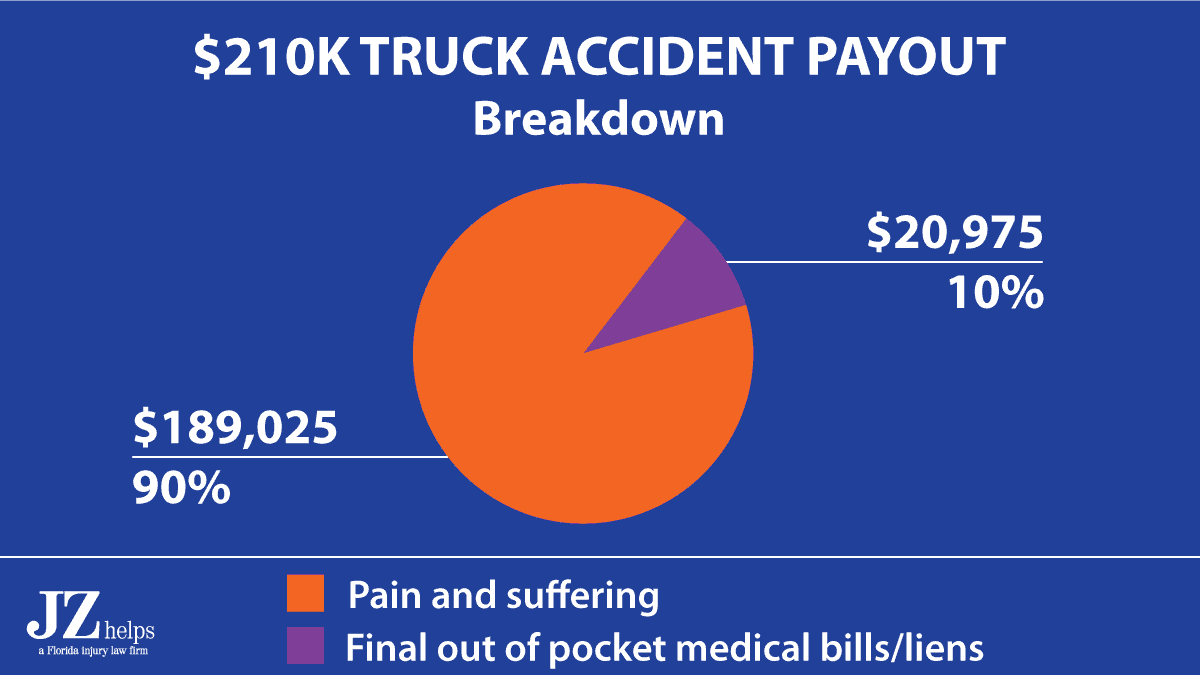

Most of the uninsured motorist settlement and bodily injury settlement was for pain and suffering:

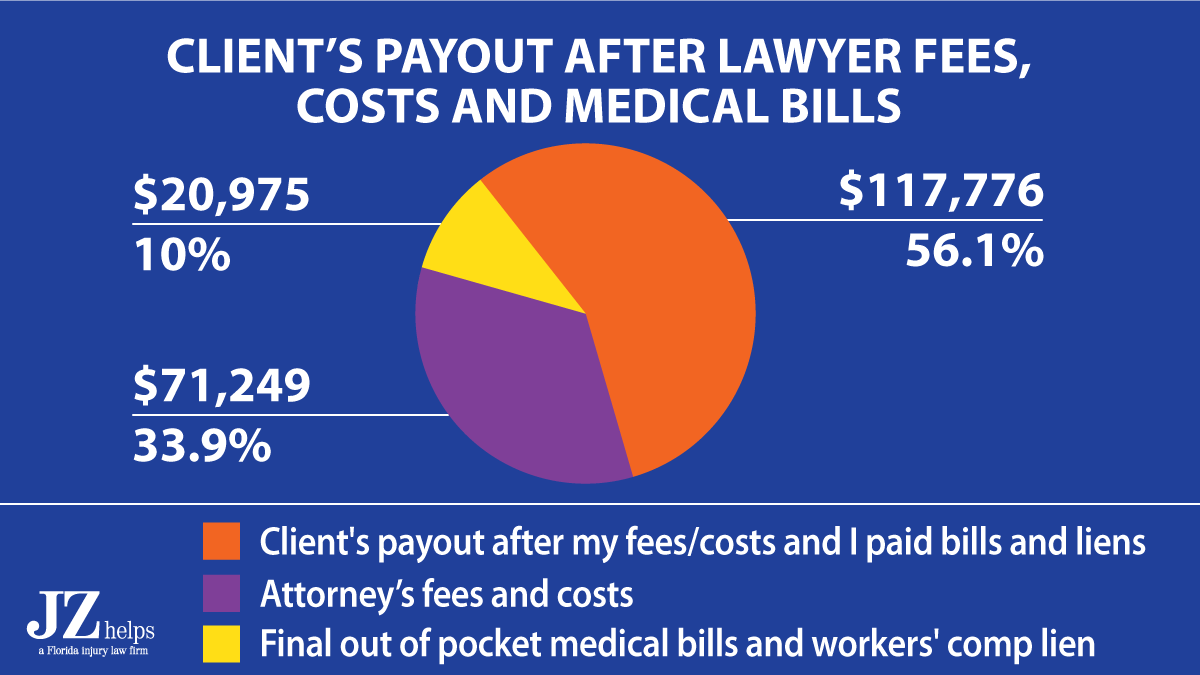

After my injury attorney fees, costs and paying his out of pocket medical bills and workers’ compensation lien, Mike got $117,776 in his pocket.

The doctor recommended that Eddie have an MRI of his right ankle.

About 7 days after the accident, Eddie had the MRI of his ankle. It showed that he had complete tears of two ligaments with associated soft edema indicating recent injury.

He also had a tear of the deep fibers of another ligament in his ankle.

Fortunately, he did not need ankle surgery. Since the other driver left the scene, he was considered uninsured.

GEICO told us that there was no uninsured motorist insurance on the policy. I told GEICO that the uninsured motorist rejection was invalid, and Eddie was entitled to $50,000 of UM insurance coverage

I demanded the policy limits from GEICO, and GEICO paid us the $50,000 uninsured motorist bodily injury policy limits.

$50K Uninsured Motorist Claim Payout

Type of hip fracture that my client had.

A young driver (Andrew) lost control of his car. He crashed into the guardrail. He suffered a hip fracture. An ambulance took him to the hospital.

Doctors performed surgery on him. Specifically, they put hardware put inside his hip.

Andrew told the police officer that another car cut him off. He said that the other car left the scene.

Andrew received a ticket.

He actually hired us for another accident. He had a broken wrist from that other accident. We settled his case for $35,000 (policy limits). During that claim, we learned about his hip fracture.

He didn’t know that he had an uninsured motorist bodily injury insurance claim. Fortunately, his mother had purchased $10,000 worth of stacking uninsured motorist (“UM”) coverage with GEICO. She had five vehicles under the GEICO policy. Thus, there was $50,000 in uninsured motorist insurance.

We settled his hip fracture case for the $50,000 uninsured motorist insurance limits. GEICO quickly paid me the limits. The uninsured motorist insurance adjuster didn’t even take Andrew’s statement.

$45K Underinsured Motorist Coverage Settlement with Lyft ($70k Total Payout)

In Florida, if an Uber vehicle has a passenger(s), there is $250,000 in available uninsured motorist insurance. That is good news for passengers and drivers.

In Florida, Lyft does not have uninsured motorist coverage on its vehicles.

Underinsured Motorist Insurance Pays $47K of $57K Settlement

A police officer suffered back injury, while he was on duty, when he was rear ended in a car accident in Medley, Miami-Dade County, Florida.

The driver who caused the accident received a ticket for following too closely. We received the policy limits of $10,000 from the at fault party’s insurance company, State Farm.

My client suffered a bulging disc and was a candidate for back surgery (lumbar laminectomy). He had epidural shots to his lower back.

Epidural steroid injection

Travelers Insurance insured the police officer’s personal car with uninsured motorist insurance. Even though he was working at the time of the accident, Travelers UIM paid $47,000 to settle the case.

Since the cop was working at the time of the crash, workers compensation for the police department paid over $17,000 in indemnity (lost wages) and medical benefits.

Bicyclist’s Underinsured Motorist Insurance Pays $42,500 of $52,000 Settlement for Back Injury

A bicyclist was riding his bike in Miami-Dade County, Florida. A car cut him off and they crashed.

USAA insured the bicyclist’s car with UIM insurance. USAA paid $42,500 to settle.

Underinsured Motorist Insurance Pays $19K of $39K Settlement

Eric (not real name), a man in his 30’s, was diagnosed with a herniated disc in his lower back following an auto accident. The damage to his pickup truck is below.

The crash happened in Pinecrest, Miami-Dade County, Florida. Before this crash, he received years of chiropractic treatment on the same levels in his lower back that he claimed were injured in this accident.

He had epidurals to his lower back after this accident. GEICO insured the negligent driver with $20,000 of bodily injury (BI) liability coverage.

GEICO paid its $20,000 limits. My client had UIM insurance coverage with Star & Shield Casualty (NARS).

North American Risk Services (NARS) handled the claim for Star & Shield.

NARS paid $19,000 to settle his personal injury claim. The total settlement was $39,000.

$10K Uninsured Motorist Claim Payout (At Fault Driver’s Insurance Paid an Extra $25K)

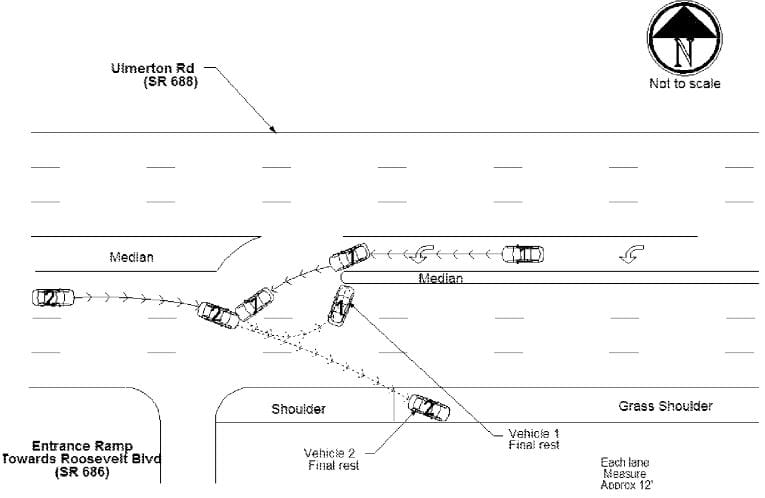

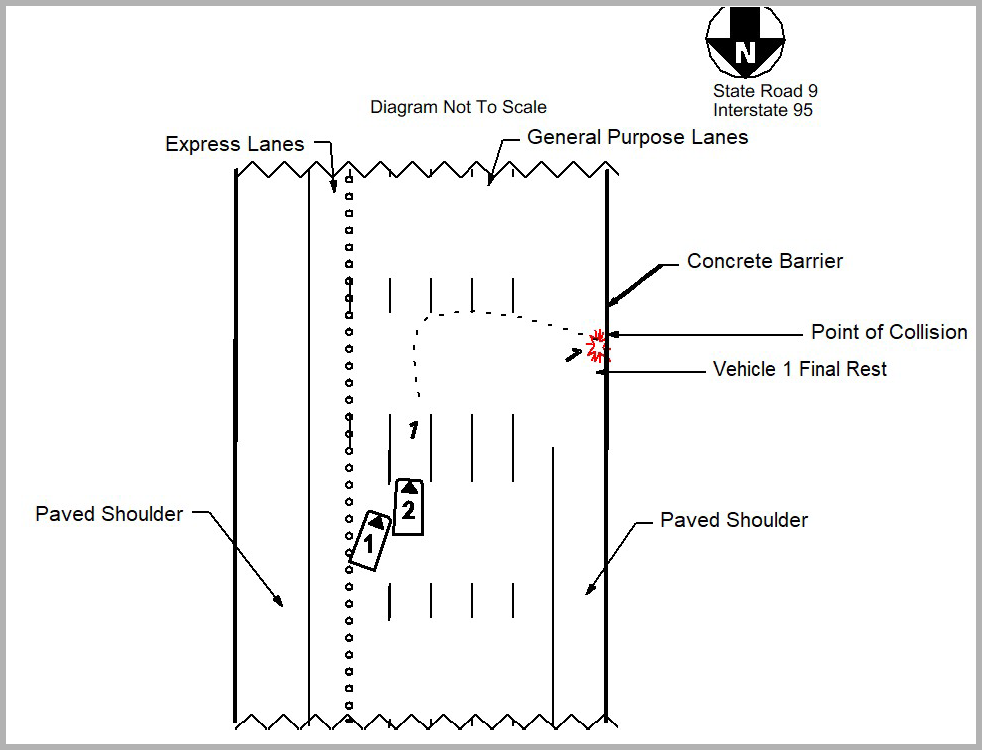

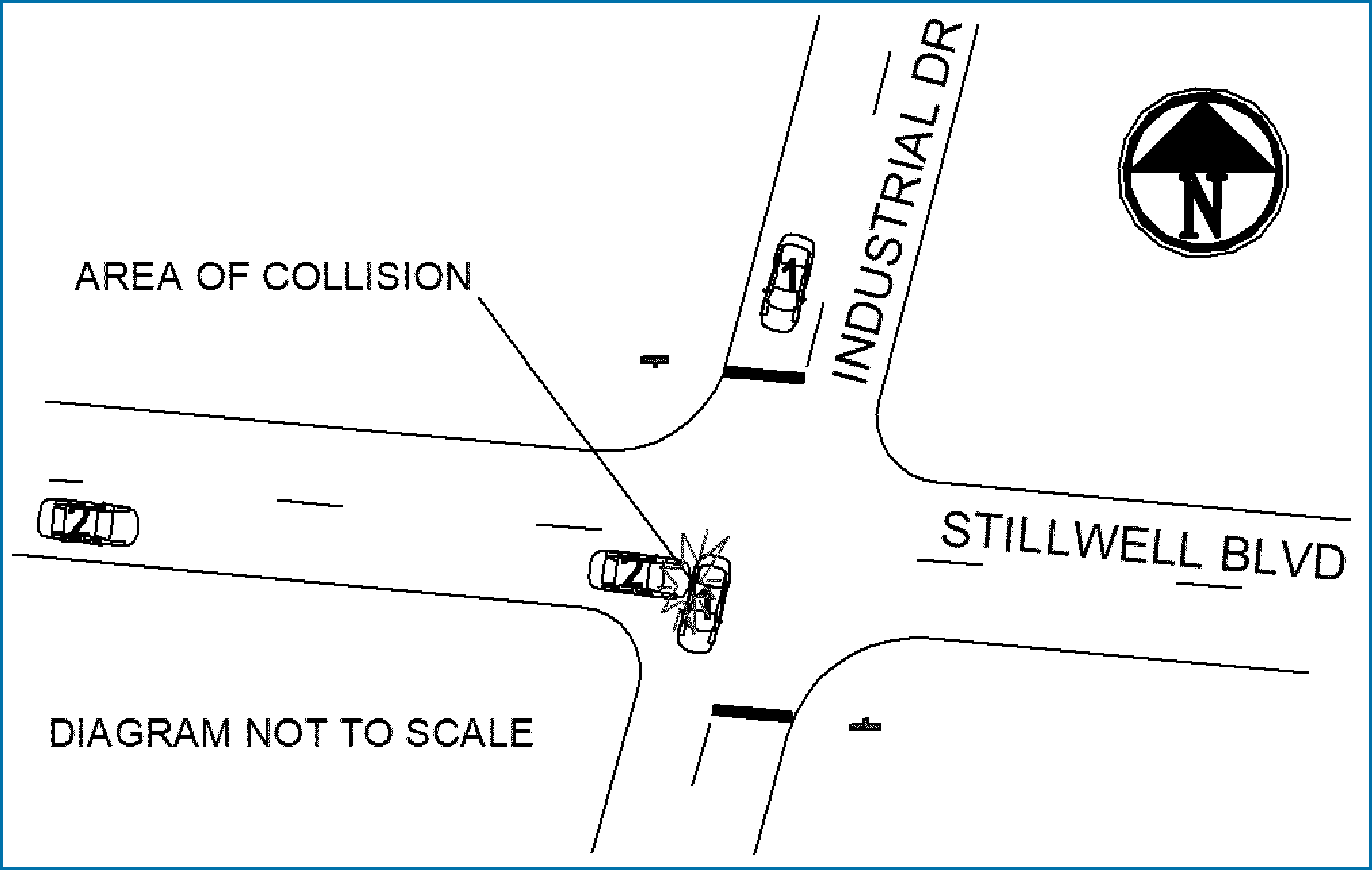

Sandra’s employer gave her a car to use for work. In August 2020, Sandra was driving east in Crestview (near Pensacola), Florida. Daniel was in a car heading south. He ran a stop sign.

As a result, the front of Sandra’s car struck the passenger side of Daniel’s car.

You can see the damage to Sandra’s car here:

You can see the actual diagram from the crash report here:

State Farm insured Daniel’s car (#1 in the diagram) with $25,000 in bodily injury liability insurance coverage.

After the accident, Sandra had back and neck pain. She said that her workers’ compensation insurance company gave her limited information about how wage loss worked.

Sandra searched Google for how wage loss works with workers’ compensation. She found my website my website. She got a free consultation with me.

Sandra was working at the time of her accident. Thus, her workers’ compensation paid all of her medical bills.

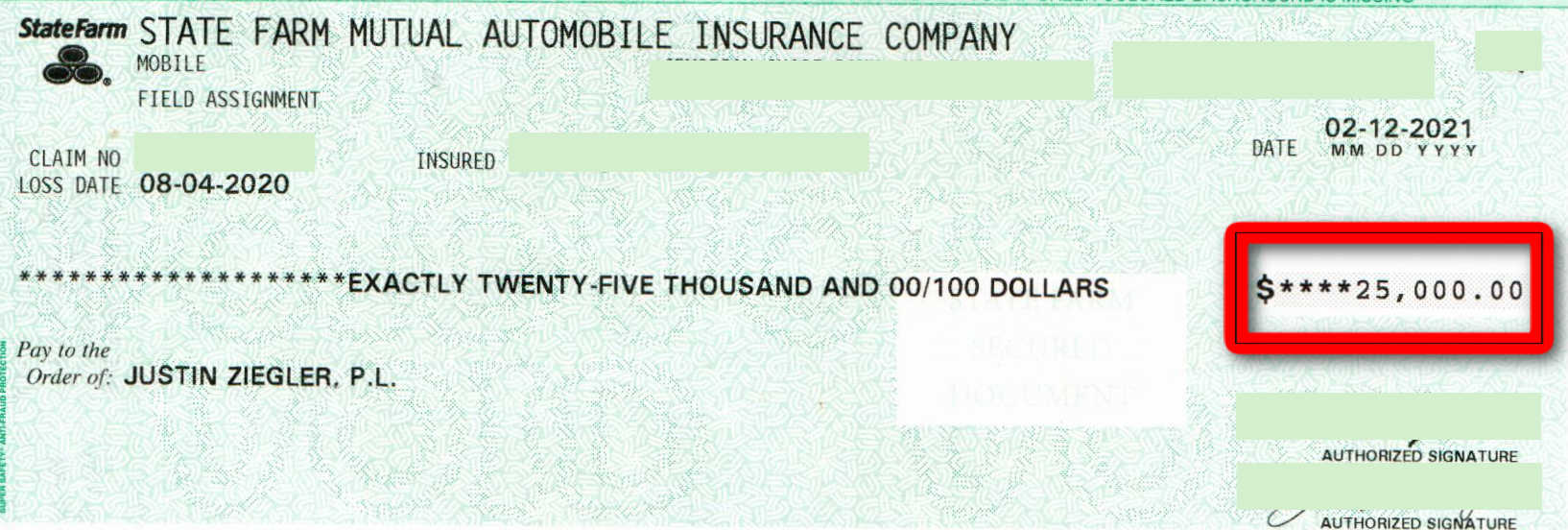

I got State Farm to pay me its driver’s $25,000 BIL insurance policy limits. You can see the settlement check:

This was about 6 months after the car accident.

It gets better:

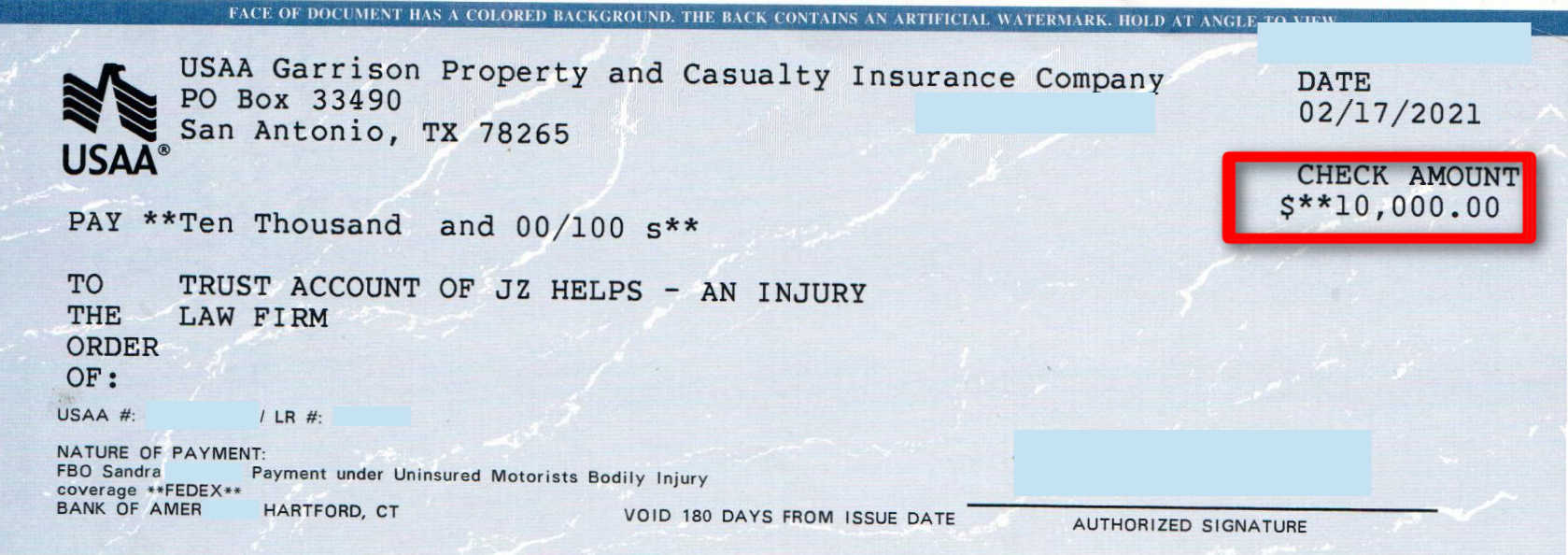

USAA insured Sandra’s personal car with $10,000 of uninsured motorist insurance coverage. At the time of this accident, Sandra was not driving her personal car. However, her underinsured motorist insurance (from her personal car) covered her for this accident.

In February 2021, I got USAA to pay me Sandra’s $10,000 limit of uninsured motorist coverage.

Normally, you have to pay back the workers’ compensation insurance company from your personal injury settlement. However, they must reduce their claim (lien) by your attorney’s fees and costs and other factors.

Here, Sandra’s workers’ compensation lawyer got the workers comp insurer to waive it’s lien. Sandra was happy with our personal injury settlement.

Sandra also settled a workers’ compensation claim with her employer’s insurance company.

Underinsured Motorist Insurance Pays $25K of $33K Settlement

On July 30, 2018, Shankeva was a passenger in her boyfriend’s car in Holly Hill, Florida.

Another driver (vehicle 1) hit another car (vehicle 2) head-on. Vehicle 2 then struck the car in which Shankeva was a passenger.

Unfortunately, vehicle 1 only had $10,000 per person in BIL insurance. This was a multi-car accident. We got $8,000 of the $10,000 BIL insurance limit.

Shankeva was a passenger in a car that State Farm insured.

The good news?

Specifically, the car had $25,000 per person in uninsured motorist insurance coverage.

My client claimed that a rear end crash caused her herniated disc.

The accident happened in Miami, Florida.

$28K Uninsured Motorist Bodily Injury Settlement

In 2020, Cordario was driving his car in Flemington, Marion County, Florida. A driver rear ended Cordario’s car. This sent Cordario’s car off the side of the road where he struck a pole.

You can see the rear end damage here:

Below, you can see the damage to the front of his car when he struck the pole:

His airbag did not deploy. This was a hit and run accident.

An ambulance took Cordario to Shands Hospital in Gainesville, Florida.

Codario had a traumatic fracture of ulnar styloid with minimal displacement. The ulnar styloid is a bone at the end of your forearm closest to the wrist.

This was to his non-dominant arm. Your uninsured motorist insurance case is worth more if your break a bone in your dominant arm. This is because it has a bigger effect on your daily activities.

Fortunately, Cordario did not need surgery for this broken bone.

This was not a serious fracture. In fact, the hospital radiologist said that the x-ray showed that he may have a small and difficult to see avulsion fracture. In other words, he was not certain that it was a fracture.

He searched for a hit and run lawyers. He saw my videos and client testimonials. He called me and I gave him a free consultation.

After we spoke, he hired me. Cordario also had lower back pain. He received physical therapy for it.

Progressive insured Cordario’s car with uninsured motorist insurance. In 2021, I settled his case for $28,000 without his suing his uninsured motorist insurance company, Progressive.

After my lawyer fees, costs and paying his medical bills, we gave him a check for $15,496.

He gave us this review:

⭐⭐⭐⭐⭐

Rating: 5 out of 5.

Lying in the hospital bed I wasn’t even sure if i even had a case for a hit and run accident. I searched for hit and run lawyers and Justin was the first name to come up. I watched his videos and testimonies. Justin and Jenny [paralegal] were awesome. They kept me up to date during the whole process. There was never a grey area. Things got really tough financially for me and Justin came in clutch at the right time. This process was as smooth as can be. Thank you guys so much for your help.

Google 5 star review on April 12, 2021

$25K Uninsured Motorist Insurance Settlement

See a case where a passenger was rear ended by an uninsured driver. The crash happened in Key Largo, Florida.

What Happens if the Careless Driver Has BIL Insurance, But Not Enough?

Assume that the tortfeasor (careless) driver has BIL insurance, but not enough to fully compensate the injured person or in the case of death, the personal representative, for personal injuries or wrongful death.

The careless driver’s BIL insurer should send the injured person a check for the careless driver’s BIL insurance limits. They will usually also send you a settlement release.

You then need to decide if you are willing to release the careless driver from all personal injury liability in exchange for his or her BIL insurance limits. If you are, and you want to make a UM insurance claim, you need to follow a procedure. Florida Statute 627.727(6)(a)

You send a copy of the settlement check, and the written disclosure of BIL insurance limits, to all underinsured motorist insurers that provide coverage. This written notice of the proposed settlement must be sent by certified or registered mail.

The UM insurer has 30 days to match the BIL insurer’s offer, or waive subrogation. Either way, you still have a UM claim against the UM insurer.

Example (Careless Driver is Underinsured; UM Covers You)

Mike is driving a car. Assume Mike is entitled to uninsured motorist insurance coverage. (Perhaps he had UM insurance on the car that he was driving. Maybe he was driving the car of a relative that Mike lived with, and the car had UM coverage on it.)

A driver of another car rear ends you and you are injured.

The other driver or owner has $10,000 in liability coverage, which is the most common scenario in Miami and throughout Florida.

Assume your bodily injury claim is worth $20,000. You can make a claim against the uninsured motorist insurance because the tortfeasor does not have enough liability coverage to pay for your bodily injury.

What if You’re Hurt in YourCar With Nonstacking UM, But You Have Stacking UM on Another Car That You Own?

In this instance, your total available UM coverage is your stacking UM coverage plus your non-stacking coverage. Here is what the court said in a Florida appeals case:

If, as in this case, Mr. Swan paid a premium for stacked coverage on the Honda, but rejected UM coverage on the Acura then it does not matter which vehicle he and his wife were occupying at the time of the accident. He and his wife would be entitled to UM benefits under the Honda policy, even if they were occupying the Acura.

However, under Coleman they would be entitled to receive only $100,000 per person, for a total of $200,000, under the Honda policy because they only paid a premium for stacked coverage on that vehicle. The Swans could not also recover UM benefits under the Acura policy because they rejected UM coverage and paid no additional premium for it.

You need to collect the uninsured motorist bodily injury limit under your car’s non-stacking policy first, before you demand to settle for the uninsured motorist insurance stacking policy limits. If you collect the stacking policy’s uninsured first, the non-stacking UM policy likely won’t owe you money. Hoffman v. Progressive Express Ins. Co., 294 So. 3d 448, 451 (Fla. 1st DCA 2020).

What if You’re Hurt in Your Car (Without UM), But You Have UM on Another Car That You Own?

Assume that Bob is driving his own car in Florida. He doesn’t have uninsured motorist insurance on it.

Bob is hurt due to the negligence of an underinsured car. If Bob has non-stacking UM on another car that he owns, can he use that UM for this accident?

To answer this question, you have to read the car insurance policy (that has the UM) to see if it has an “owned auto” exclusion. If it does, Bob can’t use his UM from the vehicle that wasn’t involved in the accident.

There was a recent case where a motorcycle was not defined as an auto for the “owned auto” exclusion. Rather the “owned auto” was defined as four or more wheels. Thus, in that instance, there was UM coverage. However, if it had been an auto, there would have been no coverage. (If you know the case name, please let me know in the comments below and I will add it here.)

For example, let’s say that Bob was visiting from Georgia but was driving his Florida car without UM. In this instance, I think Bob’s Georgia uninsured motorist insurance (on the car that wasn’t involved in the accident) wouldn’t pay for his injuries. This is because Bob was driving his own car without UM coverage.

What if You’re Hurt in Your Car (Without UM), But Your Relative (Who You Live With) Has UM on a Car That They Own?

In this case, your relative’s (who you live with) uninsured motorist insurance will cover you only if it is stacking coverage.

So let’s assume the following:

You were driving your car (without UM coverage) and another driver hits you. You break a few bones and have surgery. At the time of the accident you were living with your brother or sister.

They have stacking UM insurance on their car. This stacking UM will cover you for your personal injury claim.

The same is true if you were living with your:

Father and mother

Grandparents, grandchildren, great grandparents, great-grandchildren

Aunts, uncles, nieces and nephews

But what happens if your relative’s (who live with) UM coverage is non-stacking?

In this scenario, you’re out of luck. I’ve seen injured accident victims lose out on huge potential claims because their relative had non-stacking UM coverage in this instance.

You’re Driving Your Live-in Girlfriend’s Car. Will her UM Cover You?

Yes, you’re covered under your girlfriend’s UM. This assumes that she did not make a material misrepresentation or concealment when she completed her insurance application. Even if she didn’t tell her car insurance company that you lived together when she applied for insurance, the better insurance companies are unlikely or less likely to deny coverage.

On the other hand, companies like Windhaven, United Auto, and others are much more likely to deny coverage if your girlfriend didn’t tell them that you lived with her when she applied for coverage.

This is true regardless of whether your girlfriend has non-stacking UM, or stacking UM.

Amount of Insurance Coverage (Per-Person vs Per-Occurrence Limit)

The per-person and and per-occurrence limits (e.g., $200,000/$300,000) are handled just like the normal bodily injury liability limits. The UM limits are not changed by the number of causes of action that might accrue as a result of bodily injury or wrongful death to one person.

For example, in the case of wrongful death to an insured with $200,000/$300,000 limits, recovery is limited to $200,000 regardless of the number of survivors making a claim for the wrongful death. GEICO General Insurance Co. v. Arnold, 730 So.2d 782 (Fla. 3d DCA 1999); Mackoul v. Fidelity & Casualty Company of New York, 402 So.2d 1259 (Fla. 1st DCA 1981). See also Florida Insurance Guaranty Ass’n v. Cope, 405 So.2d 292 (Fla. 2d DCA 1981).

If you’re covered by an out of state UM insurance policy, the out of state law will determine whether two or more survivors (of someone who is killed in a car accident) can get the per person or per accident UM limits.

Does an Uber driver get uninsured motorist coverage from his own policy?

Let’s assume that you are driving an Uber with the app on in Florida. However, you have not yet accepted a ride. Another car hits you and takes off.

In a state like Florida, there is some bad news:

If you read Uber’s insurance policy, you’ll see that Uber won’t give you uninsured motorist (UM) benefits in this instance. This is because you had not accepted a ride when you were hit.

Let’s assume that you have insurance with your personal auto insurer. Maybe you have insurance with State Farm or another company. And we’ll assume that purchased UM coverage on this policy.

The bad news?

State Farm may try to claim that your policy does not provide UM coverage in this instance. They may argue that the following clause in your personal policy excludes UM coverage:

We do not provide Uninsured Motorists Coverage for bodily injury sustained by any insured:

While occupying your covered auto when it is being used as a public or livery conveyance. This exclusion (A.2.) does not apply to a share-the-experience car pool.

Your own car insurance policy language

In this instance, you need to know the your state’s law regarding uninsured motorist bodily injury coverage. Since this accident happened in Florida, you should look for an Uber accident lawyer in Florida who can review your policy’s UM coverage. When doing so, your rideshare accident lawyer can see if your car insurance company is correct in denying you UM coverage.

Will I Get an UM Insurance Settlement if I’m Injured While on a Motorcycle?

Possibly. There will need to be uninsured motorist insurance on the motorcycle. If not, if the motorcyclist owns a car with uninsured motorist insurance, it may pay the rider.

Likewise, if the motorcycle rider lives with a relative who had uninsured motorist insurance, it may pay compensation.

Whether or not the injured person will be entitled to the relative’s uninsured motorist insurance depends on how the term “insured” is defined in under the liability and uninsured motorist coverage in the policy.

Some insurance policies have said that a relative who owns a car isn’t an insured under the policy. In that instance, the injured motorcycle rider isn’t entitled to his relative’s uninsured motorist insurance.

Years ago, Dairyland Insurance Company’s auto insurance policy said that a relative who owned car couldn’t claim uninsured motorist insurance under their relative’s auto policy. The court agreed. The case is Dairyland Insurance Co. v. Kriz, 495 So.2d 892 (Fla. 1st DCA 1986).

The injured person (or his attorney) needs to get a copy of the complete auto insurance policy.

Additionally, for uninsured motorist insurance to apply, another’s driver’s negligence must have caused the motorcycle rider’s injury. Otherwise, the rider won’t be entitled to a motorcycle accident settlement. At least not from uninsured motorist insurance.

Will a Rental Car Driver’s Personal UM Insurance Cover You if You’re Injured While a Passenger?

No, if you are not a relative of the rental car driver.

Let me give an example to explain this.

Assume Amy has uninsured motorist coverage on her personal car. Amy is not related to Bob.

While on vacation in Florida, Amy rents a car. Amy and Bob are in the rental car. An uninsured driver (of another car) hits Amy’s rental car. The other driver was negligent. As a result, Bob is injured.

Will Amy’s uninsured motorist insurance pay for Bob’s medical bills? Will Amy’s uninsured motorist insurance pay compensation for Bob’s lost wages? What about Bob’s pain and suffering?

In this example, the answer is No. Amy’s uninsured motorist insurance will not pay for Bob’s injury.

Why not?

Because Bob is a a Class II insured. In other words, Bob is not a relative of Amy’s.

A class II insured only gets the benefit of uninsured motorist insurance on the car itself. A class II insured can’t tap into the rental car driver’s personal uninsured motorist coverage.

What if Bob was a relative of Amy, and he lived with her?

In this instance, Bob may be able to get a settlement with Amy’s uninsured motorist insurance company.

Why?

Because resident relatives are considered Class I insureds. A Class I insured is entitled to the rental car driver’s personal uninsured motorist bodily injury insurance.

Which Rental Car Companies Offer $1 Million in Uninsured Motorist Insurance?

If you purchased Liability Insurance Supplement (LIS) with Thrifty, Dollar or Hertz, it includes $1 million in uninsured/underinsured (UM/UIM) motorist coverage. This can be huge if the at fault driver is uninsured, and you’re badly injured.

The UM/UIM coverage applies (while occupying the car) for bodily injury and property damage.

Who insures Thrifty, Dollar and Hertz?

Ace American Insurance insures Thrifty. You should hire an attorney that can show you his past settlements with Ace. I’ve settled case with Ace. ESIS handles Thrifty’s car accident claims and settlements.

Most uninsured motorist cases aren’t worth anywhere near $1 million. That is a lot of money.

Which Uninsured Motorist Insurance Cases are Worth $1 Million or More?

Some uninsured motorist insurance claims may be worth $1 million (or more). The most common cases that have a full settlement value above $1 million (or more) are if you’ve suffered one of the following:

Why does a brain injury (with surgery) case have a full settlement value of over $1 million?

First, the hospital charges may easily be over $500,000. Additionally, the neurosurgeon and other doctors will have high bills.

Brain injuries often come with serious issues like dizziness, memory loss, balance issues, anxiety, depression, personality changes and headaches. Uninsured motorist insurance companies often put a high value on brain injuries. The biggest damage component of a brain injury is for pain and suffering.

Additionally, if the injured person was a big wage earner, that adds tremendous value. The past lost wage claim will be big. The future lost earning capacity claim may be even bigger.

Rental Car Occupants Should Not Quickly Settle With the At Fault Driver

Assume that the at fault driver has $50,000 in BIL coverage. Assume that the an injured rental car occupant has a brain injury and surgery. Here, the injured person’s claim is worth much more than the at fault driver’s $50,000 BIL coverage limit. In this instance, he or she should not quickly settle his or her injury case for $50,000 with the at fault driver.

Why not?

First, the injured person does not want to give up the right to make a UM claim. This can happen if the you don’t follow a particular UM claim procedure. The tourist can also lose his UM claim if the settlement release with the at fault driver’s insurer is poorly worded.

Second, the injured person does not want to end up in Federal court. He or she wants to keep the case in Florida state court. There are many advantages to keeping your case state court (instead of Federal court).

Which Rental Car Companies Offer $100K in UM Coverage in Florida?

Alamo Rent a Car and National Car Rental. If you rented a car from Alamo Rent a Car, hopefully you purchased Extended Protection (EP). EP is optional. It is not required.

EP includes UM/UIM coverage for bodily injury and property damage in an amount equal to the minimum financial responsibility limits applicable to the Vehicle (the Primary Protection).

EP also includes additional coverage through an excess liability policy, with limits for the difference between the statutory minimum underlying limits and $100,000 per accident.

Again, Florida doesn’t have a minimum UM limit. Thus, Alamo’s UM limit is $100,000 per accident.

Like Alamo’s EP insurance coverage is underwritten by Ace American Insurance Company.

Thus, I assume that Avis does not offer UM coverage in Florida.

Some Other Rental Car Companies Don’t Offer UM Coverage (in Florida)

Unfortunately, some Florida rental car companies don’t offer uninsured motorist coverage. This is tru even if you purchase LIS coverage when you rent a car. Examples of companies that I’ve seen who don’t offer UM coverage are small (mom and pop) rental companies, Enterprise Rent a Car, Sixt, Advantage Rent a Car.

Basically, if you want to be able to make an uninsured motorist claim for a car accident in Florida, don’t rent a car through Sixt or Advantage Rent a Car.

Sixt Personal Accident Insurance (PAI) is underwritten by ACE USA.

How Long Does It Take to Get an Uninsured Motorist Insurance Settlement?

It varies from a case to case. I know people don’t want to hear that answer. But it’s the truth.

You’ve now seen some of my uninsured motorist settlements. Please take a look at some of my personal injury settlements.

Which insurance companies make the smallest uninsured motorist claim payouts?

When it comes to uninsured motorist claims, the cheapest insurance companies are Progressive, Allstate, Farmers. They offer the least compensation for pain and suffering.

The best paying uninsured motorist insurance companies are The Hartford, Nationwide, Hanover, Travelers and USAA. They pay above average but will still fight you hard.

As far as uninsured and underinsured motorist claim payouts, GEICO and State Farm are currently average. They have years where they are really cheap, and other years when they are just average.

Will you get a big uninsured motorist bodily injury settlement if you’re a passenger in an Uber of Lyft car?

Only if you have serious injuries and your have uninsured motorist on your personal auto insurance policy. Or if you live with a relative who has uninsured motorist insurance on their car insurance policy.

Uber and Lyft no longer have uninsured motorist insurance on their insurance policies.

In most accidents, the best case scenario for badly injured rideshare passengers is if the Uber of Lyft driver is at fault. This is because Uber and Lyft carry a $1 million liability policy that covers the passengers if the rideshare driver is at fault.

Which states require uninsured motorist insurance?

Editor’s note: I periodically update this article. You should always speak with a Florida car accident lawyer for questions about uninsured motorist insurance for Florida accidents or insurance policies. This article is NOT legal advice.