Out-of-State Visitors in Florida Car Accidents (Settlements)

Justin Ziegler, Lawyer

Got hurt in a car crash in Florida, but you’re not from here?

Good news – you might have a strong case! Whether it’s a typical car crash or a ride in Uber or Lyft, if you’re visiting Florida and get into an accident, things may be simpler than you think.

Here’s the cool part: I’ve helped many people just like you win big.

I’ve settled cases worth over $900,000 for visitors hurt in Florida.

And guess what? Handling your case from another state isn’t as hard as it seems.

I’ll reveal some real settlement stories that’ll clear up how things work. I’ll also expose some unique rules that apply, and get into the specifics of accidents involving rental cars and ride-share services like Uber and Lyft.

Ready to find out how you can turn your bad luck into a possible win?

Travelers Insurance insured Ryan’s personal cars in Georgia.

Medpay from an Out of State Policy Pays Medical Bills from a Car Accident (But Not for Work)

On Ryan’s auto policy, he had $5,000 in medical payments (Medpay) coverage. We made a Medpay claim for Travelers. However, Travelers denied Medpay coverage because Ryan was working when the accident happened.

If Ryan wouldn’t have been working at the time of the crash, his Medpay coverage would’ve paid $5,000 to his medical providers. This brings me to an interesting point.

Many tourists or out of state visitors who are hurt in a Florida car accident are confused as to how to get their medical bills paid. And rightfully so. Understanding which insurances apply is complicated.

Just click on the image above.

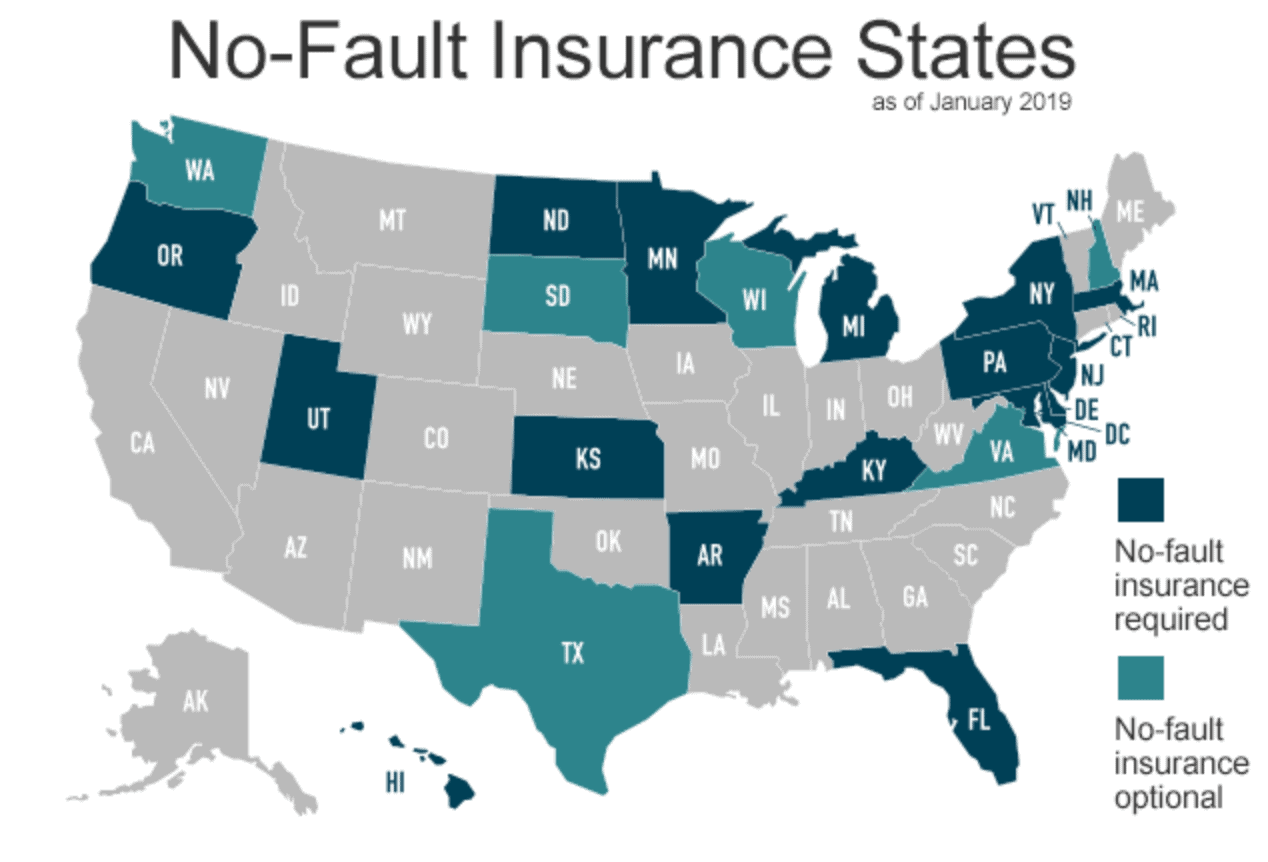

Out of State Visitors to Florida May Get PIP Insurance from the Rental Car

Florida is one of a few No Fault states. Here is a map that shows which states are No Fault states:

Therefore, I made a personal injury protection claim (PIP) with Ryan’s rental car company. PIP insurance pays up to $10,000 of medical bills and lost wages after an accident. And PIP pays regardless of fault. PIP is also known as no-fault insurance.

Many people have a hard time understanding why the rental car’s PIP insurance pays if someone else caused the accident. The answer is simple:

That’s what the law says. Again, Florida is a no-fault state.

Remember:

If you’re hurt while occupying a rental car in Florida, you get the rental car’s PIP coverage. This assumes that there isn’t another PIP source that should pay first.

The rental car’s PIP coverage pays even if you are visiting from another state. Thus, the rental car’s PIP pays even if you are a tourist visiting Florida.

It gets better:

The rental car’s PIP coverage may be in addition to the Medpay coverage on your car insurance policy. In a moment, I’ll talk about how we got Ryan $10,000 of rental car PIP benefits. But first, let me talk about the settlement.

Ryan also had Georgia underinsured (UIM) insurance with Travelers. They paid $200,000 to settle. This was in addition to the $100,000 personal injury settlement with the other driver’s Allstate.

Some people think that an injured person’s attorney gets most of the injury settlement. I’m happy to report that this is rarely true.

After my attorney’s fees and costs, Ryan received $191,200. He got 63% of the settlement his pocket.

OK. As promised, let’s get back to the PIP benefits. The rental car company agreed that Ryan was entitled to $10,000 in PIP benefits.

As I mentioned earlier, Ryan was working at the time of the accident. This means that workers’ compensation (Sedgwick Claims) basically paid all of Ryan’s medical bills. If workers’ comp applies, the injured workers doesn’t have to pay any medical bills out of pocket.

In total, workers comp paid about $85,000 to the hospital and Ryan’s doctors.

We agreed to pay them a little over $10,000. But I didn’t stop there.

I used the $10,000 in PIP benefits to pay most off the workers compensation lien.

The result?

It put an extra $10,000 in Ryan’s pocket! And boy was he happy.

I’ve given you the short version of Ryan’s car accident settlement. We’ve touched on some insurance and claim issues that can arise when an out of state visitor is hurt in Florida.

Throughout this article, you’ll see many other examples of claims for out of state visitors who were hurt in Florida car accidents.

I hired Justin to help me with my automobile personal injury case. He responded to me right away and he got started protecting my rights.

My case was very complicated involving my severe injury, multi-state involvement, car rental companies, several different insurance companies, workers comp, and probate issues due to the other driver passing away.

Justin and his assistant, Jenny, worked hard the whole way through and, importantly, were always responsive to me, even at night or weekends. I would highly recommend that you hire JZ Helps to handle your case!

Should I hire an attorney if I am injured in Florida, and I live in another state?

Yes, if you were injured in the car accident. There are many reasons to hire an attorney after a car accident. However, if you were injured while traveling from another state, there are additional reasons to get a lawyer.

First, you are going to be dealing with the laws of at least two states. These laws are confusing. Understanding which laws apply is not easy. Heck, I’ve been handling car accident cases for 16 years, and I still do legal research.

And if you were injured while in a rental car, you will likely be dealing with 6 (or more) claim adjusters. To complicate matters, these adjusters will likely be from 3 different insurance companies. If you don’t have a perfect understanding of car accident coverage, you may be giving up valuable rights (and money).

Do not expect these insurance companies to explain the law to you. The auto insurance adjusters’ goal is to close out your claim as fast they can (for the least amount of money possible, or in some cases no money). Do not expect the adjuster to tell you that there is additional insurance coverage that you have not discovered. It won’t happen.

What’s the solution if you were hurt in a Florida, while visiting from another state?

Get a free consultation from me to see if I can represent you. I love representing people from other states who are injured in Florida car accidents.

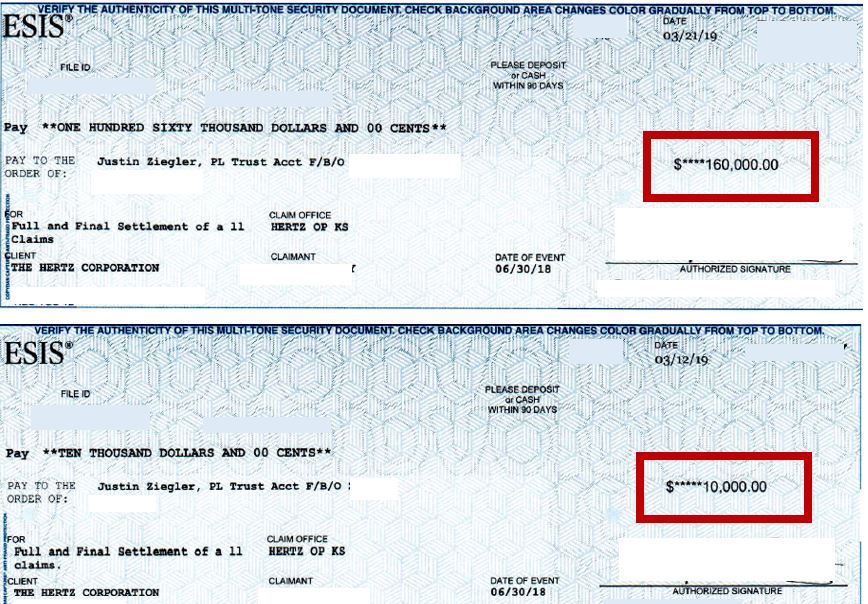

$170K Settlement for West Virginia Man (Hurt in Florida Car Accident)

Zach lives in West Virginia. In June 2018, he was visiting Florida with his family.

He was a passenger in a Thrifty rental car in Sarasota, Florida.

The driver crashed into the back of a car ahead of them.

Zach broke his arm (humerus). Zach’s mom hired me as his personal injury attorney.

He had surgery. We made a claim against the insurance company (Ace American Insurance Company) for the Thrifty rental car. ESIS handles claims for Thrifty (Ace American Insurance).

The rental car driver purchased Liability Insurance Supplement (LIS) when he rented the car. This means that Ace American insured the rental driver for up to $2 million for liability (injuries or property damage) to others.

Further below, I explain (in detail) how rental car insurance coverage works for out of state visitors who are injured in Florida car accidents.

Here is an image from Zach’s 5 star Google review of my law firm:

Here’s Zach’s entire review:

I definitely recommend Justin Ziegler. He was there for me after my I broke my arm in low impact collision on Sarasota, Florida.

He helped me receive a very sizable settlement. Should I ever need a lawyer again, I will go to Justin first.

Just click on the image above.

Out of State Visitor Gets $135K for in Miami-Dade (Florida) Car Accident

A passenger was visiting Florida from another state. While she was in a car in Miami-Dade County, Florida, another car t-boned that car that she was in.

Additionally, Maria had a car insurance policy with Nationwide Insurance Company on her car in the state where she lives. Maria also had uninsured motorist insurance on her car.

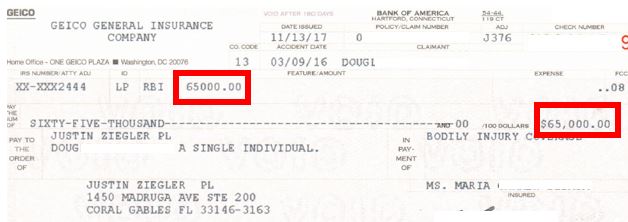

$65K Settlement for Pedestrian from California (Hit By Car in Miami)

Doug, who lived in California, was on vacation in Miami Beach. While he was walking in a crosswalk, a car hit him. (My description below explains your rights when you’re hurt while on vacation in Florida.)

The pedestrian found me after seeing our online ratings and looking out our website/blog. He hired me to represent him in his personal injury claim against GEICO.

Pursuant to Florida Statute 627.4137, I sent GEICO a letter asking for the driver’s insurance information.

Remember, he was from California. California doesn’t have PIP.

Many other states don’t have PIP. States like Indiana, Iowa, Tennessee, West Virginia and many others don’t have PIP. Earlier in this article, I shared a map that shows the states that don’t require PIP.

Doug gave my personal injury law firm a 5 star review on Google. He said:

Justin Ziegler did an excellent job handling my auto accident case. He and his senior paralegal, Jenny, kept me abreast on its progress throughout. I give his firm my highest recommendation.

$65K Settlement for Visitor from North-Central US (Orlando Car Accident)

She was rear ended in Orlando, Florida while visiting from another state.

$10K Settlement for Michigan Resident Who Was Injured in Florida Car Accident

My client was visiting Florida from Michigan. She was driving her car.

Another driver crashed into her. She went to the hospital in Fort Pierce, St. Lucie County, Florida.

She later went to a chiropractor for several months in her home state. She had a soft tissue lumber (lower back) strain and sprain. GEICO insured the at fault driver.

GEICO initially offered $500. They then increased their offer to $800. We refused both offers. We later settled with GEICO for $10,000.

This case involved a tourist from another state in the United States.

You’re Resident Relative’s UM Insurance Follows You To Florida

Perhaps you live with a relative in another state, and that relative has uninsured motorist insurance on a car.

If a careless driver caused your crash in Florida, your resident relative’s UM insurance should cover you. This is true even if you aren’t in your resident relative’s car at the time of the crash in Florida.

I settled a case for an out of state resident who was hurt while in a Hialeah, Miami-Dade County, Florida car crash. She was in someone else’s car at the time of collision.

To better illustrate the 90 out of 365 day rule, I’ll use this example:

Kate owns a car. It’s registered in Maine. State Farm insures it. When Kate got her auto insurance policy, she told State Farm that the car is garaged in Maine. (Garaged simply means that the car is kept there.) Since State Farm believes that the car is garaged in Maine, it issues a Maine auto insurance policy for Kate.

In the past year, Kate was working in Florida for 200 days out of the past 365 days. And during those 200 days, her car was in Florida. Maybe she is a seasonal employee, who sometimes works in Florida, and at other times works in Connecticut.

In this instance, Kate’s car must have PIP insurance.

Why?

Because it was kept in Florida for over 90 days out of the prior 365-day period.

However, there’s likely a bigger issue for her personal injury or insurance claim. The bigger issue is that when bought her Maine auto policy, Kate didn’t tell State Farm that the car was kept in Florida.

Thus, if Kate is hurt in a Florida car accident, State Farm may deny coverage. If State Farm asks what Kate was doing in Florida at the time of the accident, she must tell the truth. In other words, she should not say that she was on vacation or visiting a friend if it’s not true.

Why Does Kate need to tell State Farm (or any insurance company) the truth?

Because lying to an insurance company is considered insurance fraud. Insurance fraud is a 3rd degree felony! It’s serious business.

It’s better than Kate tells the truth, rather than her winding up in jail.

If you happen to be someone like Kate, and are considering hiring me as your lawyer, and you want me to go along with your lie to the insurance company about why you were in Florida at the time of your crash, please don’t contact me. I won’t take your claim. I don’t represent people who commit insurance fraud.

No one case is worth my integrity or law license. Not even a million dollar case.

Out of State Car’s UM Insurance Will Cover You in Florida

Take the first example above with Maria. She was a passenger in a friend’s, Sara. Sara owned and kept the car in another state.

It’s being driven in Florida. Sara’s uninsured motorist insurance should cover Maria, even if the crash happens in Florida.

This is true even if you live in another state and were visiting Florida.

Nonresidents May Not Need To Meet No-Fault Threshold for Pain and Suffering…If They Have UM.

In Florida, UM coverage typically doesn’t cover you for your pain and sufferingunless you meet the tort threshold requirement. Sternberg v. Allstate Insurance Co., 900 So.2d 732 (Fla. 4th DCA 2005).

However, if you live in a “fault state” ( without no-fault insurance), and an uninsured vehicle driver’s negligence causes your injury in Florida, you don’t have to meet the no-fault threshold in order to get money for pain and suffering from your UM insurer. Dauksis v. State Farm Mutual Automobile Insurance Co., 623 So.2d 455, 456 (Fla. 1993).

In a soft tissue injury or smaller injury case, the pain and suffering component of a nonresident’s (from a fault state) case may be worth more if he or she has UM insurance and the careless driver is uninsured.

This is because your out of state UM car insurance likely won’t require that you have a threshold injury in order to get money for pain and suffering.

NonresidentPedestrians Hit By Car in Florida May Have an Easier Case

Out of State UM Insurance May Not Apply if No Impact With Other Car

There are exceptions to the general rule of UM coverage for out of state residents who are hurt in Florida car wrecks.

Some out of state insurance policies require that there must be physical contact between two vehicles for UM insurance to apply.

Georgia UM insurance law has this requirement. However, it has an exception. If there is no contact between the 2 vehicles, but there is an independent corroborating witness, this should qualify you for UM coverage.

In addition to the above corroborating witness requirement, if there is no contact with another vehicle, some other states have two additional requirements.

For example, Oregon uninsured motorist coverage requires the accident to be reported to the police within 72 hours of the accident. Additionally, a statement under oath must be filed with the uninsured motorist insurer within 30 days stating that the insured or his or her attorney has a claim arising out of the accident against a phantom vehicle. The insured must give facts in support as well. 2017 Oregon Laws Chapter 742.504

If you miss these requirements, you lose your uninsured motorist coverage. You don’t want to lose this valuable coverage. After all, uninsured motorist coverage can be very valuable. To the tunes of hundreds of thousands or millions of dollars.

You’re Covered by Your UM Insurance (Even if You’re Driving a Rental Vehicle in Florida)

If you live in a state other than Florida, and you’re an occupant of a rental car, you UM insurance on your out of state auto policy should cover you. This is true even if you’re working.

If You Live in Another State, and Are Hurt in a Florida Car Accident, How Long Do You Have to Sue?

The time limit to sue the at fault party from an auto accident in Florida is usually 4 years from the date of the crash. Cases against a governmental entity have shorter deadlines.

If the visitor to Florida has an out of state UM insurance policy, the out of state law will determine how long the visitor has to sue that UM insurer. Many states have time limits to sue an UM insurer that are shorter than Florida’s 5 year UM statute of limitations (time limit to sue). Some are much shorter.

For example, North Carolina give you three years (from the accident date) you to serve the UM insurer with the summons and complaint in the lawsuit against the uninsured motorist. N.C. Gen. Stat. § 20-279.21(b)(3). Thus, if you are from North Carolina and you are hurt in a Florida car accident, you only have three years to sue the NC UM insurer.

What If You’re Injured in an Uber or Lyft Accident While Visiting Florida?

If you’re injured in an Uber or Lyft accident in Florida, while visiting from another state, the claim gets more complex. The out of state visitor is typically in Florida for one of two reasons.

They are either here for a:

Vacation (or pleasure)

Business (work related)

In either instance, the injured person is even more likely to need a Uber or Lyft personal injury lawyer to protect their rights. This is because you’ll be dealing with multiple insurance coverages and different state laws.

The injured Uber or Lyft passenger should make a Personal Injury Protection (PIP) or Medpay claim with his or her personal auto insurance. This is true even though the injured person was not in his or her own automobile at the time of the accident.

If the out of state visitor was within the course of his or her employment at the time of the accident, the out of state Medpay insurance likely won’t cover the visitor.

However, he or she should still make a claim for PIP or Medpay with his or her personal auto insurance so that they can deny coverage.

Why do you want a letter denying PIP or Medpay coverage?

Because this denial can be given to your health insurance company (and Lyft’s insurance company) so that they can pay benefits. Otherwise, the health insurance company (or Lyft’s insurance company) may continue to deny paying medical bills that they believe your auto insurer (or Lyft’s insurer) should pay.

Lyft’s PIP insurer will pay a Lyft passenger’s PIP benefits before the passenger’s health insurance pays medical bills. Thus, an injured Lyft passenger should also make a PIP claim with Lyft.

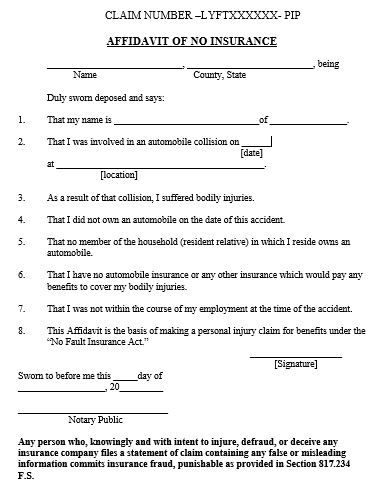

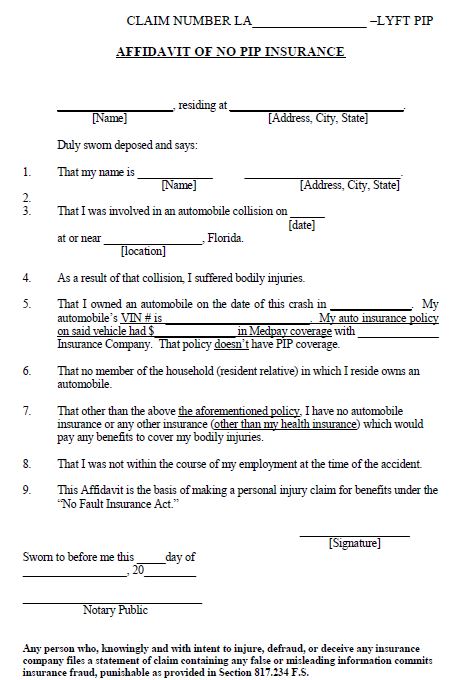

The injured person should quickly send Lyft an affidavit of no insurance if appropriate. I use different affidavits depending on whether or not the injured passenger owned an automobile on the date of the accident.

Here is a Lyft PIP affidavit that I may use if my client didn’t own an automobile on the date of the accident:

If the injured passenger only owned an automobile in his home state, I change the affidavit so that it looks more like this one:

However, the Lyft “No PIP” Insurance affidavit’s wording will depend on the specific circumstances of the injured person. Thus, it needs to be a custom fit.

Don’t wait for Lyft’s claim handler (State Farm) to send you this form. You needs to edit the form (as appropriate) and sign it in front of a notary.

If the injured person has a Lyft accident attorney, he or she should do this quickly. This is one of the many advantages to hiring an injury lawyer.

How Could Quickly Completing a PIP Affidavit Lead to a Faster Injury Settlement?

Because the medical bills will get processed (and paid) faster. Thus, the injured person will know the amount of his or her out of pocket medical bills. In order to value a personal injury case in Florida, the injured person needs to know their out of pocket medical bills.

In Florida, the injured person is only entitled to compensation for their out of pocket medical bills (and any liens). The injured person can’t get compensation for the full billed charges. This Florida law is different from that of many other states.

The injured person may also be entitled lost wages and pain and suffering.

Uber’s Medpay Insurance Will Only Pay if You Don’t Have Your Own Medpay

If you’re visiting Florida from another state and get hurt in a car accident while riding in an Uber, the Uber may have medical payments coverage (MedPay) to help with your medical bills.

However, Uber’s MedPay will only pay if you don’t have MedPay on your own car insurance policy.

Uber’s insurance won’t pay PIP Benefits to passengers in Florida.

Uber’s Insurance Won’t Pay PIP Benefits to Passengers in Florida

Also, Florida’s rideshare law doesn’t require PIP.

However, the injured passenger should still make a claim with Uber’s insurance company. Uber’s insurer will deny PIP coverage in a letter to the injured passenger.

Here is what the PIP denial letter looks like:

That letter was from an insurance company that insured Uber a while back. However, Progressive’s letter will look similar.

Regardless, you should quickly send the insurance company PIP coverage denial letter to your health insurance company. Otherwise, your health insurer might not pay medical bills.

If You’re Relative was Driving and Caused Your Injury, Will His Insurance Company Pay You?

It depends on whether you were living with your relative. It will also depend on whether the out of state law allows insurance companies to exclude BIL insurance coverage for resident relatives.

On the other hand, some other state’s do not allow an insurance company to exclude BIL coverage if a driver causes injury to his resident relative. It really all depends on the state where the driver’s policy was issued.

Whether You Have to Pay a Health Insurer From the Settlement Depends on Out of State Law

Many injured people use their health insurance to pay their medical bills related to the accident. As you can imagine, sometimes health insurance pays a large amount of medical bills. This is particularly true if the injured person had surgery.

The type of health plan that you have will determine if you have to pay back your health “insurer”.

The first question that must be asked is:

Was the health “insurance” secured through someone’s job?

If the answer is “Yes”, and it is not a government job, then the member needs to find out if the health plan is self-funded.

Assuming the health plan is self-funded, then the plan language will determine how much the member is required to reimburse the health insurer.

Large employers typically have self-funded health plans. Examples of large employers are Walmart, Target, Publix, Costco, CVS, Whole Foods, big banks (Bank of America, etc.) and others.

If the health plan is self-funded, then the reimbursement aspect of the visitor’s claim is treating just like a Florida resident.

Example – Out of State Law Determines if Injured Person Must Repay Health Insurance (Acquired via Work)

However, if the health insurance isn’t self-funded, then the state law that governs the contract will determine if reimbursement is required.

As an example, let’s assume John lives and works in New York. He works for an accountant with 3 other employees. He purchased his health insurance through his job.

John’s health insurer pays $10,000 of his medical bills. John makes a claim against the Uber driver for his medical bills, lost wages and pain and suffering.

The Uber car’s insurer, James River Insurance Company, pays $45,000 to settle John’s injury claim.

In this case, John doesn’t have to pay back his health insurer any of the $10,000 that they paid for his medical bills. This saves John $10,000!

Why Doesn’t John Have to Repay His Health Insurance Company?

He doesn’t have to pay back his health insurer from because John’s health plan is an insured health plan. I know that it is insured because John’s employer is very small (4 employees). Since John worked in New York (NY), the health insurance company is subject to NY’s antisubrogation law.

The result is the same if John got his health insurance because he (or a family member) was a city or state employee. This is because city and state health insurance plans are subject to the out of state law.

And again, New York has a very good antisubrogation law for people who are injured in Florida.

I used Uber in the example above. However, the result would be the same if it was Lyft or any car insurance company.

(Fun fact: I settled a similar case for $70,000 except it wasn’t against Uber. It was against Lyft’s underinsured motorist insurance for $45,000, and GEICO’S policyholder for $25,000. There were some other different facts, such as John (not real name) was a Florida resident. Also, the Lyft driver wasn’t at fault.

Ok. Let’s get back to health insurance repayment.

Will your health insurance company argue that Florida’s law determines if you have to pay them back from a car accident settlement?

Possibly. The health insurance company may argue that if you’re injured in Florida, Florida law applies to their reimbursement claim. They may claim that Lincoln National Health & Casualty Insurance Co. v. Mitsubishi Motor Sales of America, Inc., 666 So. 2d 159 (Fla. 5th DCA 1995) says that Florida law applies to their reimbursement claim against you because the crash happened in Florida.

Don’t fall for this argument. They are wrong!

Here’s why:

Lincoln concerned a dispute between an insurer and the at fault party. Lincoln specifically says that the choice of law rule does NOT apply to a dispute between an insured and her insurer involving a reimbursement claim. And you are an insured.

Reimbursement from you is different from subrogation against the at fault driver.

Even if you signed a settlement release with indemnification language that may cover the subrogation claim then in a state like New York there are many cases saying stating that even that settlement release does not allow a New York health insurance company to require you to pay it back.

Out of State Law Determines if Injured Person Has to Repay Health Insurance (That Wasn’t Purchased Through Work)

If the health insurance wasn’t purchased through work, then the state law of the health insurance contract will determine the amount of reimbursement. For example, individual and ACA (Obamacare) plans are subject to the state law of the resident.

Let’s change the facts of the case involving John a little bit. Assume John didn’t buy his health insurance through work.

Assume he got his own individual plan or an Affordable Care Act (ACA) health insurance. Since New York state law applies to individual and ACA health insurance plans for New Yorkers, John doesn’t have to repay his health insurer. This saves John $10,000.

If the injured person lives in a state with antisubrogation laws, and he or she has an individual or non-ERISA health plan, it usually results in a bigger net settlement for the injured person. This assumes that the case has settlement value.

Some states with antisubrogation laws in regards to health insurance are:

Out of State Law Will Determine If You have to Pay Back Medpay Benefits

Let’s assume that an out of state visitor is hurt in a Florida car accident. His Medpay from his out of state car insurance policy pays some of his medical bills. The out of state law will likely determine if he has to repay the Medpay insurer.

However, some states do not allow the Medpay insurer to claim a lien on the settlement. Virginia is one state that follows this rule. Code of Virginia § 38.2-2209

Let me give you an example. Assume Mike lives in Virginia. While visiting Florida, he is injured in a car accident. He breaks his wrist, or suffers a herniated disc.

Assume Mike’s Virginia car insurance company pays some of his bills under its Medpay coverage. If this happens, Mike doesn’t have to pay his car insurance company back if he settles his personal injury case with the responsible party.

North Carolina doesn’t allow a car insurance company to require its insured to pay it back for Medical Payments coverage if he or she settles an injury case. 11 N.C.A.C. § 12.0319. Thus, a North Carolina resident who is injured in Florida doesn’t have to pay back his or her auto insurer if he reaches a settlement with a driver.

States that require the injured person to repay the Medpay auto insurer are:

The UM/UIM coverage applies (while occupying the car) for bodily injury and property damage.

Who insures Thrifty, Dollar and Hertz?

Ace American Insurance insures Thrifty. You should hire an attorney that can show you his past settlements with Ace. I’ve settled case with Ace. ESIS handles Thrifty’s car accident claims and settlements.

Some claims may be worth $1 million (or more). The most common cases that have a full settlement value above $1 million (or more) are if you’ve suffered one of the following:

Brain injury that required surgery to your skull

Several surgeries to a body part and you’ve developed chronic regional pain syndrome (CRPS)

Out of State Visitors to Florida Should Not Quickly Settle With the At Fault Driver

Assume that the at fault driver has $50,000 in BIL coverage. Assume that the out of state visitor to Florida has a brain injury and surgery. Here, the out of state visitor’s (to Florida) personal injury claim is worth much more than the at fault driver’s $50,000 BIL coverage limit.

In this instance, the out of state visitor should not quickly settle his or her injury case for $50,000 with the at fault driver.

Why not?

First, the injured out of state visitor does not want to give up the right to make a UM claim. This can happen if the you don’t follow a particular UM claim procedure. The tourist can also lose his UM claim if the settlement release with the at fault driver’s insurer is poorly worded.

Second, the injured out of state visitor does not want to end up in Federal court in Florida. He or she wants to keep the case in Florida state court. There are many advantages to keeping your case state court (instead of Federal court).

Which Rental Car Companies Offer $100K in UM Coverage in Florida?

Alamo Rent a Car and National Car Rental. If you rented a car from Alamo Rent a Car, hopefully you purchased Extended Protection (EP). EP is optional. It is not required.

EP includes UM/UIM coverage for bodily injury and property damage in an amount equal to the minimum financial responsibility limits applicable to the Vehicle (the Primary Protection).

EP also includes additional coverage through an excess liability policy, with limits for the difference between the statutory minimum underlying limits and $100,000 per accident.

Again, Florida doesn’t have a minimum UM limit. Thus, Alamo’s UM limit is $100,000 per accident.

Like Alamo’s EP insurance coverage is underwritten by Ace American Insurance Company.

Thus, I assume that Avis does not offer UM coverage in Florida.

Some Other Rental Car Companies Don’t Offer UM Coverage (in Florida)

Unfortunately, some Florida rental car companies don’t offer uninsured motorist coverage. This is true even if you purchase LIS coverage when you rent a car. Examples of companies that I’ve seen who don’t offer UM coverage are small (mom and pop) rental companies, Enterprise Rent a Car, Sixt, Advantage Rent a Car.

Basically, if you want to be able to make an UM claim for a car accident in Florida, don’t rent a car through Sixt or Advantage Rent a Car.

Sixt Personal Accident Insurance (PAI) is underwritten by ACE USA.

If You Live in Another State, and You’re Injured in Florida, Do You Have to Pay Back Your Disability Insurer for Benefits It Paid?

I use the same analysis for short or long term disability “insurance” as I do for health insurance above.

Some states have antisubrogation laws in regards to disability insurance are:

Let’s assume a North Carolina resident is injured in a Florida car accident.

If the North Carolina resident has a individual disability insurance, he or she doesn’t have to pay the disability insurer back if he settles a personal injury case.

People From Connecticut Who are Injured in Florida Car Accidents

Let’s look at another state, Connecticut. Connecticut Medicaid can allegedly collect not only medical bills paid for the injury, but also any cash assistance from the Connecticut’s state department of social services.

The law says that the 50 percent of the amount recovered is “after payment of all expenses connected with the cause of action.”

For example, assume that a Connecticut Medicaid beneficiary is hurt in a Florida car crash. He settles against the at- fault driver, before a lawsuit, for $10,000. Medicaid paid $400 in medical bills.

Connecticut Medicaid can’t get more than 50 percent of the settlement (minus costs). In this example, Medicaid can’t get more than the half of $5,000.

Delaware Residents Injured in Florida Car Accidents

Unlike Florida, a Delaware PIP insurer has a right of subrogation for reimbursement against the third-party insurance company. 21 Del. C. § 2118(g) This means that your Delaware car insurer will try to recoup its PIP payments from any settlement that you reach with the at fault car insurance company. Delaware residents may get a higher total settlement than Florida residents in the same case.

Let me explain.

Let’s assume that you live in Delaware and are injured in a Florida car accident. Another driver was at fault. You have a Delaware auto insurance policy. Your Delaware PIP coverage pays $15,000 of your medical bills.

You want to settle your case against the at fault insurance company. Your Delaware car insurance company will likely want to recoup the $15,000 in PIP that it paid from your personal injury settlement with the at fault driver’s insurance company. If they assert this right, then you can argue to the at fault driver’s insurer that they need to pay you for this $15,000 in addition to your pain, suffering and other medical bills.

If you have PIP on a Florida car insurance policy, the PIP insurer generally does not have a right for subrogation.

Ohio Residents Hurt in Florida Car Accidents Benefit by Hiring a Lawyer

Many Ohio residents get a big benefit by hiring an attorney for a Florida car accident. Here’s why:

Ohio law allows a pro-rata reduction of a health or disability insurance by the injured person’s attorney’s fees and costs. Hoeppner v. Jess Howard Elect. Co., 780 N.E.2d 290 (Ohio App. 2002). Therefore, if an Ohio resident is injured in a Florida car accident, the Ohio health insurer must reduce it’s lien by the claimant’s attorney’s fees and costs.

Let me illustrate. Assume that Mike lives in Ohio. Mike works for a local or state government job. Or perhaps he has his health insurance through a small employer.

While on vacation in Florida, Mike is involved in a rear end accident. Another driver is at fault. Let’s say that Mike’s health plan pays $5,000 to his medical providers for accident related treatment.

Mike settles his personal injury case against the driver for $15,000. Mike will likely have to pay back his health insurance company from his personal injury settlement.

The good news?

The health plan will have to reduce its lien by Mike’s pro-rata attorney’s fees and costs. This assumes that he made the wise decision of hiring a lawyer.

Therefore, Mike’s owes his health insurance company $3,333 from the settlement. In this instance alone, Mike saves $1,666 by hiring an attorney. If Mike did not have a lawyer, he would owe the health plan the full $5,000 lien!

That said, if Mike’s health insurance plan is an ERISA self-funded plan, it usually does not have to reduce its lien. This assumes the plan language states this.

Visitors from Indiana Injured in Florida Car Accidents

If you’re visiting from Indiana and get into a car accident in Florida, your underinsured motorist (UIM) coverage will apply only if your UIM policy limit is higher than the at-fault driver’s bodily injury (BI) liability limit.

If you’re hit by a car while walking in Florida, your medical payments (MedPay) coverage from your Indiana auto insurance may help pay your medical bills, up to your policy limit. Additionally, you may have a UIM claim if your UIM limit is higher than the at-fault driver’s BI limit.

If your Indiana health insurance covers your medical bills for a car accident in Florida, you might have to pay them back if you settle your injury case. You’re in a better position if you got your health insurance through the private marketplace or your employer is the county, city or state. In these cases, the insurer must reduce its payback by the percentage of your lawyer’s fees. This can be a big advantage of hiring a lawyer.

If the at-fault driver’s insurance is limited, your health insurance might need to further reduce its repayment demand.

Visitors from Tennessee Residents Hurt in Florida Car Accidents

If you live in Tennessee but you’re injured in a Florida car accident, there are several very important things to know. I’ll discuss two of them here.

First, don’t settle the personal injury claim against the at fault driver if you want to make a UM claims based on a Tennessee car insurance policy. Doing so could kill your UM claim.

Do Massachusetts Residents Have to Pay MassHealth from a Florida Car Accident Settlement?

Yes, for medical assistance benefits that MassHealth paid. Massachusetts General Laws Chapter 118, Section 22(b). In Massachusetts, Medicaid and the Children’s Health Insurance Program (CHIP) are combined into one program called MassHealth.

Additionally, the claimant must repay the costs attributable to services provided to the claimant that were paid by the Health Safety Net Trust Fund established in section 66. Massachusetts General Laws Chapter 118, Section 22(e).

Moreover, if the claimant was not receiving financial assistance benefits before the accident, then the claimant must repay the total of all financial assistance benefits provided by the department on and after the date of the accident to or on behalf of the claimant. Massachusetts General Laws Chapter 118, Section 22(f).

So far I’ve focused on claims for people who live out of state, and are injured in Florida.

I’ve discussed several fact patterns where someone from a particular state was hurt in a Florida car accident. However, I haven’t included examples of people from every state. In the near future, I hope to add fact patterns for people who are hurt in Florida car accidents while visiting from:

Alabama, Alaska, Arizona, Arkansas

Colorado, Delaware, Hawaii, Idaho, Indiana

Kansas, Kentucky, Louisiana, Maryland

Minnesota, Mississippi, Missouri, Montana

Nebraska, New Hampshire, New Mexico, North Dakota

Ohio, Oklahoma, Pennsylvania, Rhode Island, South Carolina

South Dakota, Utah, Vermont, Washington, Wisconsin, Wyoming

Injured in a Florida Car Accident While Visiting from Another State?