Lyft Accidents that Occur on March 30, 2020 through June 30, 2021

I have some bad news:

For accidents from March 30, 2020 to possibly June 30, 2021, Lyft appears to have no uninsured motorist coverage. I’m talking about accidents in Florida. Uninsured motorist insurance covers you if an uninsured driver (not the Lyft driver) caused your injury.

The acronyms UM/UIM (uninsured/underinsured motorist) are no longer on Lyft’s Florida certificate of liability insurance. This will greatly affect many Lyft drivers and passengers in Florida for accidents beginning March 30, 2020.

As an example, I settled a Lyft passenger’s case for $70,000 a few years ago. If that accident happened today, he would have only gotten a $25,000. That’s a $45,000 loss! We’re talking about a huge drop in settlement value.

I don’t know what Lyft has done for other states for this time period. However, Lyft’s certificate of insurance is on its website.

Note: If I mention making a claim against Lyft’s uninsured/underinsured motorist (UM) coverage below, assume that the accident happened at a time when Lyft used to have UM coverage.

Lyft Accident Claim and Settlement FAQs

I’ve collected a bunch of frequently asked questions. Please review them carefully before handling a Lyft claim.

Who handles Lyft’s accident claims?

The last time that I checked, Lyft vehicles were insured by the following insurance companies: Latitude, Travelers (Constitution State Services), Progressive (United Financial Casualty Company), State Farm (State Farm Mutual Automobile Insurance Company), and Sedgwick.

Here are some states and the insurance company that insures Lyft:

– California (Indian Harbor Insurance Co.) – Florida, Georgia and New York (excluding NYC) – United Financial Casualty Company (Progressive) – Texas (Liberty Mutual Fire Insurance Company)

However, in regard to Lyft claims, Travelers only acts as a third party administrator. Travelers does not actually insure Lyft vehicles. Greenwich Insurance Company (AXA XL) insures Lyft. Basically, Travelers decides how much to offer to settle for. Then, they pay the claim with Greenwich’s money.

The image below shows the many 5 companies that recently handled Lyft’s claims:

Should I hire a law firm who doesn’t have the attorney’s name on their website?

No. This because you have no way of knowing if the firm actually has a licensed attorney. Without knowing the attorney’s name, you won’t be able to look him or her up to see if they are licensed with the state bar.

Do you really want to pay someone to represent you who is not even an attorney? I doubt it.

Only attorneys can represent you in a Lyft rideshare accident case. Don’t hire someone who is not licensed.

Even if the website shows a law firm name, this is not enough. You need to be able to see the lawyer’s name.

For example, let’s say the a law firm says that they are the Domingoeez Law Firm. (I made that name up). You should still be able to look at their website and see the attorney’s name.

There is no excuse for a law firm not to list the name of at least one attorney on its website. In fact, states (like Florida) require it.

The Lyft rideshare accident attorney’s name is usually found under the law firm’s “About Us” section. You can find out more about me in the “About Us” section of my website. I also list my name in every article that I write on my blog.

In addition, I put my name on the bottom of every page on my website. Look at the image below. I have nothing to hide.

Are Lyft drivers covered with collision insurance?

Yes, if the Lyft driver had collision coverage on his or her auto policy. Lyft calls it “contingent” collision coverage. Also, Lyft’s collision coverage only applies from when the ride is accepted through the ride end.

Collision insurance is a coverage that pays the cost of repairing or replacing your vehicle. You won’t find any mention of collision or comprehensive coverage on Lyft’s certificate of liability insurance.

Thus, Lyft’s collision coverage won’t apply if the Lyft driver has not accepted a ride.

It gets worse:

There is a $2,500 deductible. Interestingly, this deductible is much higher than Uber’s collision coverage deductible. Uber’s collision insurance deductible is only $1,000. Uber beats Lyft in this aspect.

Collision coverage applies regardless of whether the Lyft driver was at fault or not. The coverage amount is up to the actual cash value of the vehicle or the cost of repair, whichever is less.

If you are a Lyft driver, just download the declarations page from your personal auto insurance company website. Then, send it to the Lyft collision coverage adjuster. The Lyft adjuster will need your declarations page in order to pay for the damage to the Lyft driver’s vehicle.

This image shows the Period 2 and 3 contingent collision coverage deductible:

Who pays your medical bills after a Lyft accident?

If a Lyft passenger owns a car, then his or her Personal Injury Protection (PIP) auto coverage will pay up to $10,000 in medical bills. However, PIP only applies in No-Fault states like Florida (and a few others). In Florida, the claimant must get medical treatment within 14 days of the crash. Otherwise, PIP does not apply.

If the Lyft passenger does not own a car, then his or her resident relative’s PIP would pay up to $10,000 in medical bills.

If the Lyft passenger does not live with a relative, then Lyft will pay up to $10,000 of the passenger’s medical bills. Before Lyft will pay any PIP benefits, the claims adjuster will run a search to confirm that the passenger did not own a car. The passenger will need to complete an affidavit stating that he or she did not own a car. If the passenger has a Lyft accident attorney, he or she can complete the statement for the passenger.

The passenger can also make a claim against the at fault party for any medical bills that are not paid by PIP. Of course, the passenger can also make a claim for lost wages, pain and suffering.

Likewise, Lyft’s PIP will pay the Lyft driver’s medical bills up to $10,000. If another driver caused the accident, that driver is liable for any medical bills not paid by the Lyft’s PIP.

How long will Lyft take to settle your injury case?

If the Lyft is engaged in a ride, then Lyft’s insurance company usually does not face any pressure to quickly settle. I’d estimate that about 80% (or so) of the time, Lyft’s insurance company does not face pressure to settle.

Why does Lyft’s insurance company not face pressure to quickly settle?

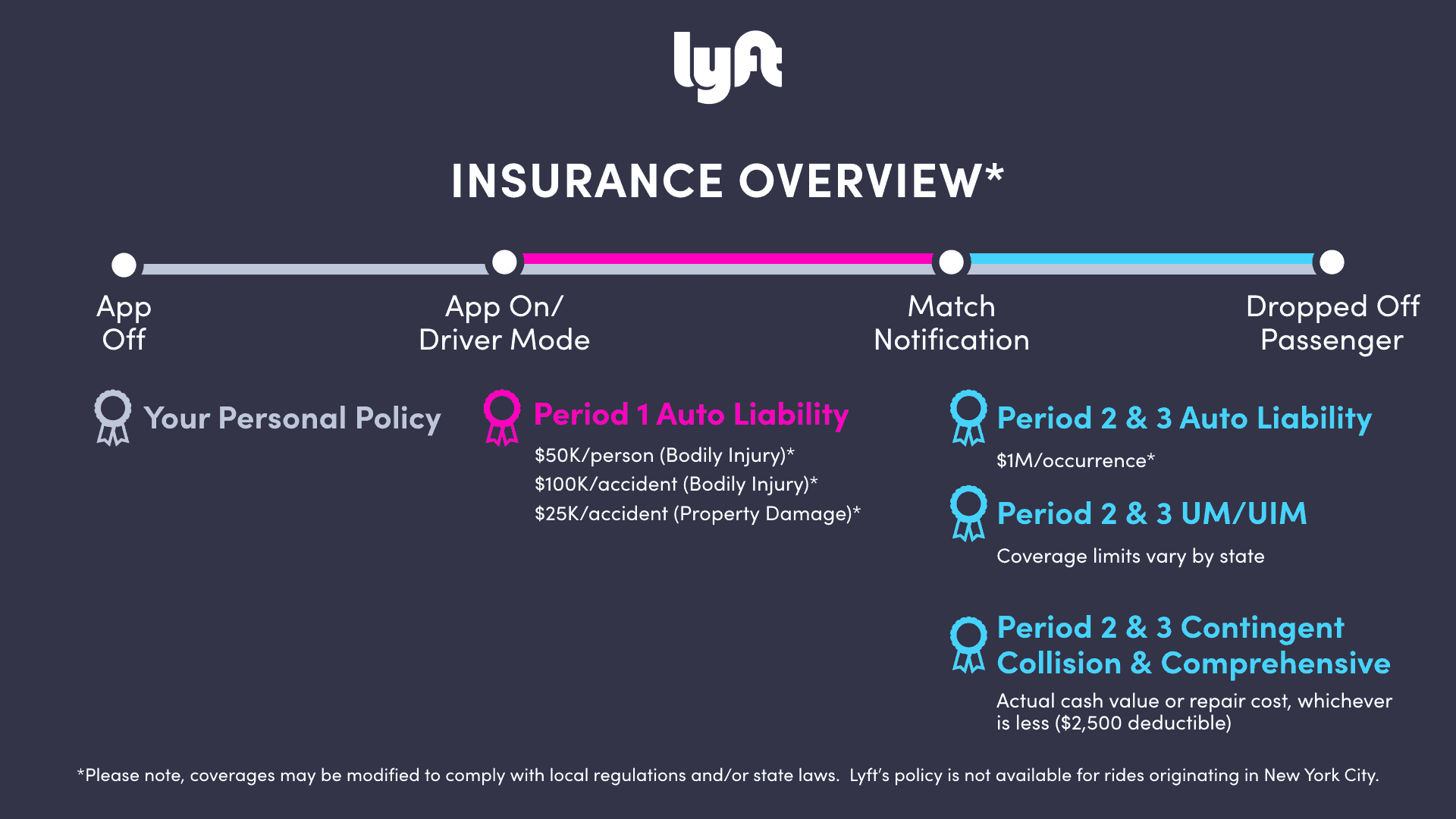

Because the Lyft vehicle will often have high liability insurance limits ($1 Million). Combine this with the fact that most injury cases are worthmuch less than the $1 Million and you have a recipe for no pressure.

Thus, in almost all cases where the Lyft driver was engaged in a ride, Lyft’s insurance company doesn’t have to worry about getting hit with a verdict for above the policy limits.

Again, the $1 million limit is pretty big. At least compared to most personal car insurance policies.

However, if the Lyft driver had the app on, but wasn’t engaged in a ride, then things are different. This is because the Lyft’s bodily injury liability (BIL) insurance limits are much lower.

The limits are $50,000 for death or bodily injuryper person/$100,000 for death or bodily injury per accident. In this instance, if the Lyft driver’s negligence caused someone else to get badly injured, Lyft’s insurance company may quickly settle. They would only have to pay the $50K per person/$100K per accident limits.

This diagram shows the different Lyft insurance coverages depending on if the Lyft is engaged in a ride:

How does LYFT insurance work?

Lyft’s car insurance works similar to other car insurance. The biggest difference is that Lyft cars usually have much more insurance than your average car.

If the Lyft is picking up passengers or during trips, Lyft’s insurance policy provides up to $1 million in BIL coverage. For insurance purposes, you’re usually better off being in an accident with a LYFT than with a random car.

What happens if your LYFT gets in an accident?

The first step is to get medical care if you need it. If you wind up making an injury claim, your payout will be smaller if you waited to get medical care.

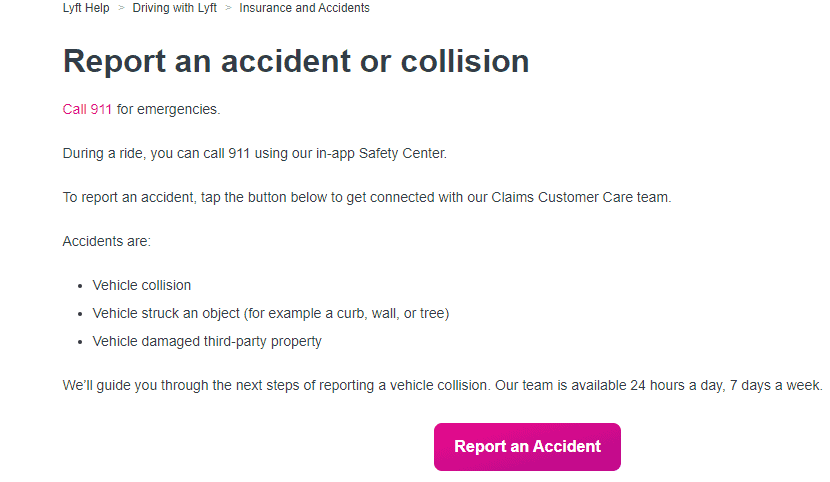

In order to get a claim setup, the accident needs to get reported to Lyft. A claim will get set up fastest if either the Lyft driver or passenger reports the accident using the Lyft app. Be careful with what you write in the Lyft app. What you write can later be used against you in your claim.

You can also report the accident by clicking the “Report an Accident” button on Lyft’s website. Once you click the button, it will ask you for your phone number. Within seconds after giving your phone number to Lyft, you will get a call from Lyft.

After the accident is reported, a claim will get set up with Lyft’s insurance company. Once a claim is setup, you will get a claim number. This is your reference number for the case. From that point forward, all of your contact will be through Lyft’s insurance company. You won’t be dealing with Lyft’s safety team.

Lyft uses different car insurance companies in different states. For example, in Florida Lyft uses Progressive American Insurance Company.

Below, was a screenshot of the “Report an accident” page from Lyft’s website:

What can you do if Lyft’s insurance company isn’t acting fairly or contacting you?

Look at Lyft’s certificate insurance certificate for the state where the accident happened. Currently, Lyft currently lists the certificate of insurance on its website for each state. Let’s use Florida (where I practice) as an example.

In Florida, Lyft’s certificate of insurance lists its insurance company as Progressive American Insurance Company. Assume that you set up a up a claim with Lyft or Progressive .

If you don’t get a response within a reasonable amount of time, you can file a consumer complaint with Florida’s Department of Financial Services. They regulate Lyft’s insurance company.

The department will quickly contact Progressive . Soon thereafter, Progressive will respond to you. If they don’t, the department may fine them. Progressive will then give you the claim number and adjuster’s contact information.

Likewise, let’s say that Lyft’s insurance company makes you a lowball offer. You can file a complaint with the department of financial services. However, if you’re badly injured, I recommend hiring a Lyft accident attorney. They’ll fight to get you fair compensation.

Does Lyft pay more for pain and suffering if the car was badly damaged?

As a general rule, insurance companies pay more money for your pain and suffering if your car was badly damaged in the accident. There is no reason why Lyft’s insurance company would be any different.

The (insurance company) thinking is that a jury is more likely to believe that you were injured in the accident if the car was heavily damaged. After an accident, take photos of the damage to all the vehicles that were involved in the Lyft accident.

If you hire a Lyft accident lawyer, he or she can take high resolution photos of the damage to your car for you. I am happy to do so for any of my clients.

Does Lyft pay more for pain and suffering if you take an ambulance to the hospital?

Insurance companies usually give you a bigger pain and suffering payout if you take an ambulance to the hospital from the accident scene. There is no reason why Lyft’s insurance company would be any different.

The (insurance company) thinking is that your injury is more serious if an ambulance took you to the hospital from the accident scene. In fact, Lyft’s representative may ask you if your airbag deployed. The reason that they do this is to determine the seriousness of the accident.

If possible, get someone to take a photo of you while you are on the stretcher. This is one of the most powerful photos in any car accident case. If you spend a night at the hospital, get someone to take a photo of your in the bed. This is a very helpful photo in an accident case. Make sure that the photo is high quality.

I am happy to take high quality photos of my clients at any hospital in Florida. I took the photo (below) of my client at Coral Gables Hospital. He was an Uber driver. I settled his case for $260,000.

Here is my video on Lyft accident settlement amounts and claims.

GEICO issued a $25,000 settlement check within just one month after the accident!

You might be wondering:

Why did GEICO send us a $25,000 check so fast?

They quickly issued a check because the GEICO insurance policy had low limits relative to my client’s injuries. Additionally, the driver (who GEICO insured) receiving a ticket for driving too fast for the conditions.

The At Fault Driver Was Underinsured (with GEICO)

However, GEICO’s $25K check wasn’t enough to compensate my client for his injuries.

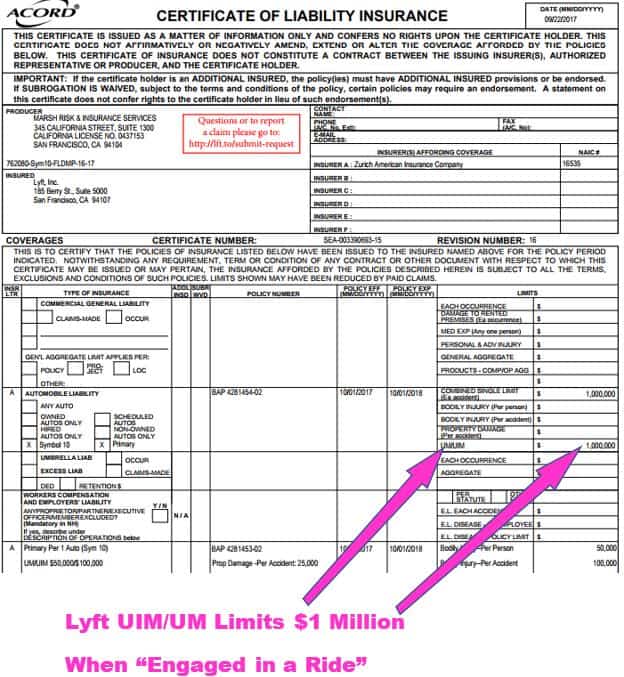

Thus, we also made a underinsured motorist insurance claim with Lyft. Fortunately, Lyft had $1 million dollars of underinsured (UIM) motorist insurance that covered its passengers.

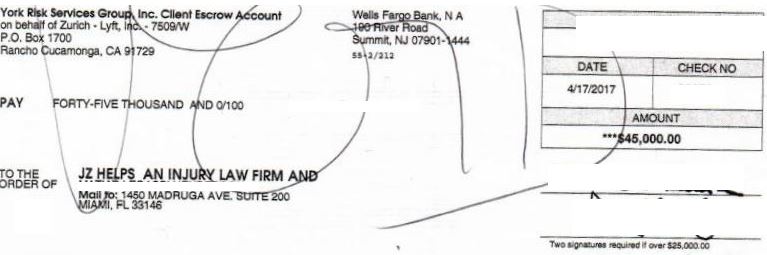

At the time of this accident, Zurich American Insurance Company insured Lyft. York Risk Services Group handled the claim for Zurich. Zurich paid us $45,000 to settle the passenger’s UIM insurance claim.

Lyft’s (York Insurance) $45,000 check is below.

$45K Settlement check from Lyft’s insurer (some info redacted)

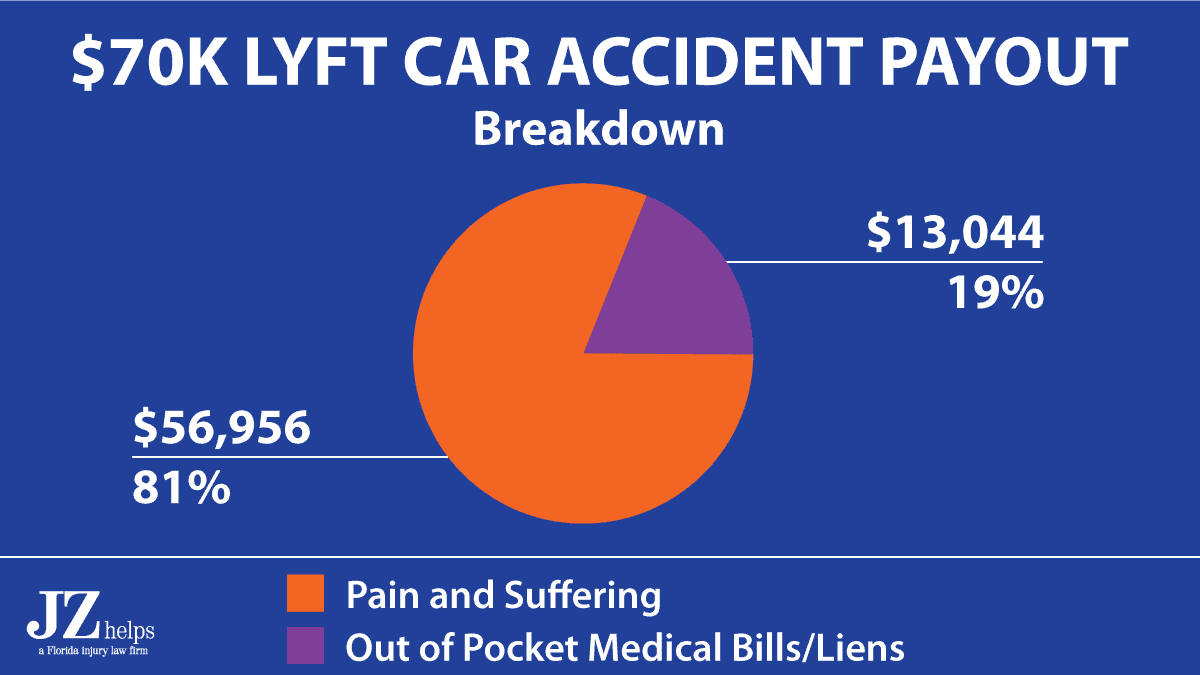

I estimate that about 81% of the settlement was for pain and suffering:

In other words, about $56,956 of the $70,000 payout was for pain and suffering. The rest was for medical bills.

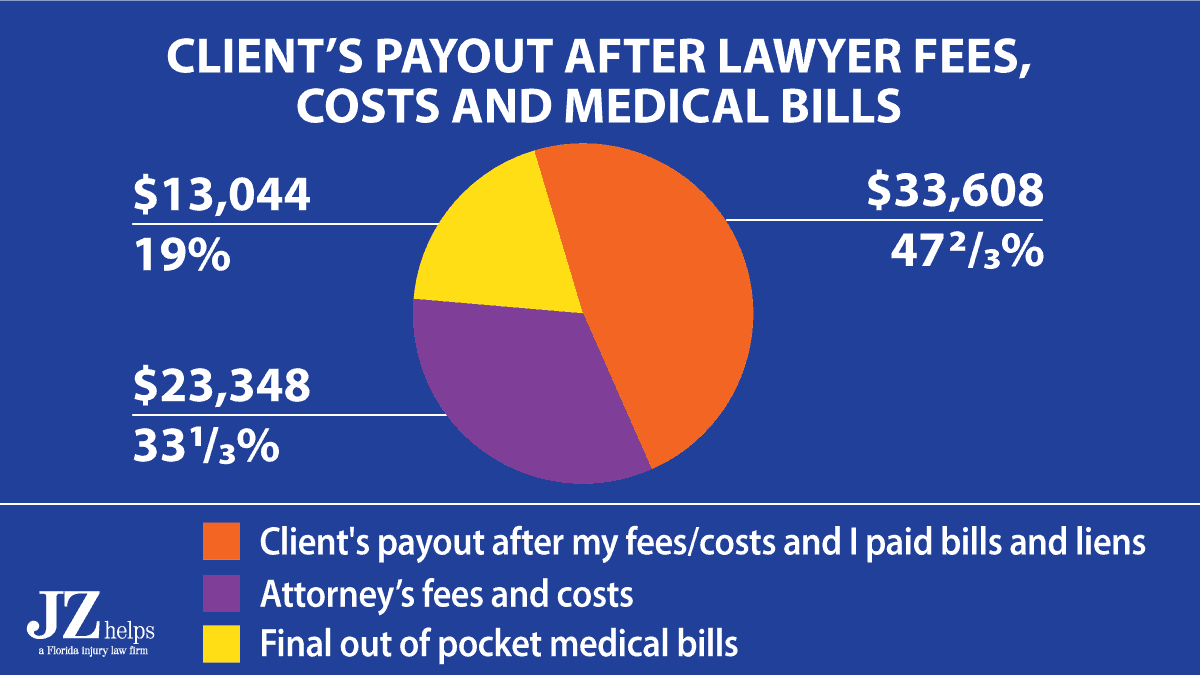

After my attorney’s fees, costs and paying his final medical bills, I gave my client a check for $33,608.

Check out the breakdown:

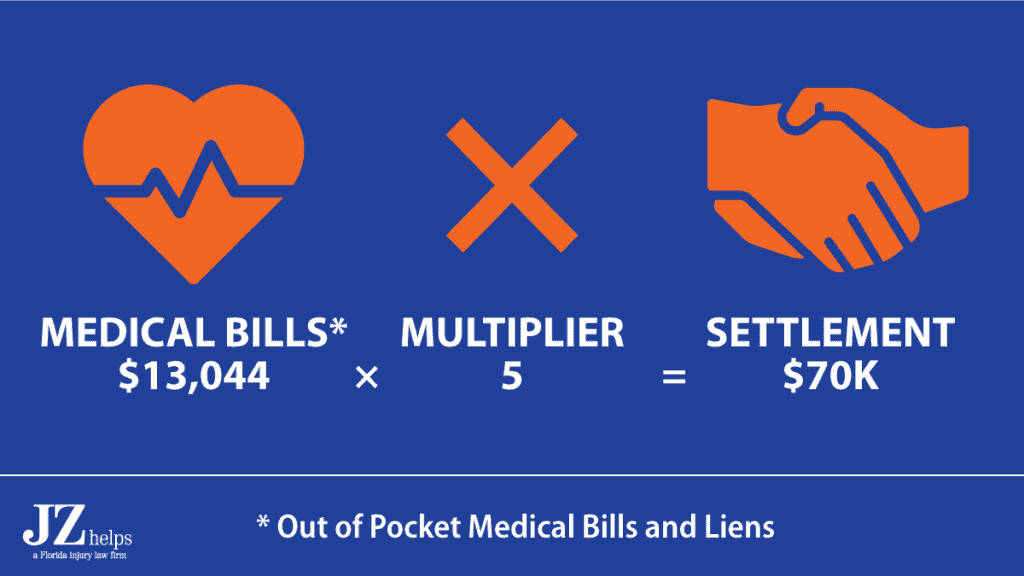

The $70,000 Lyft accident payout was about 5 times the final out of pocket medical bills. (This was after I got the medical provider to reduce the bills.)

Watch my short video about this $70,000 Lyft accident settlement:

In his 5 star review, here is what my client said about me as his Lyft accident attorney.

⭐⭐⭐⭐⭐

Rating: 5 out of 5.

Justin is fast and effective by being ALL THE TIME one step ahead of potential issues with your case. I was impressed with his accurate and rapid responsiveness even for a single phone call or email.. He’s an EXTRAORDINARY professional and human being…two qualities hard to find in a lawyer. I’m positive about referring Justin to everyone.

My actual client (Lyft passenger) review on Google Maps

What is the average Lyft accident settlement amount?

I estimate that it is under $20,000 for a personal injury claim. I’ve seen attorneys say (on the internet) that typical Lyft personal injury settlements are between $300,000 and $1 million.

I completely disagree.

Most Lyft accident claims are not worth $300,000 (or anywhere close to it). This is because most Lyft accidents do not result in serious injuries. And it’s serious injuries that lead to settlements of $300,000 or more.

Lyft Doesn’t Have Uninsured Motorist Insurance

Currently, Lyft’s certificate of liability insurance does not show uninsured motorist coverage.

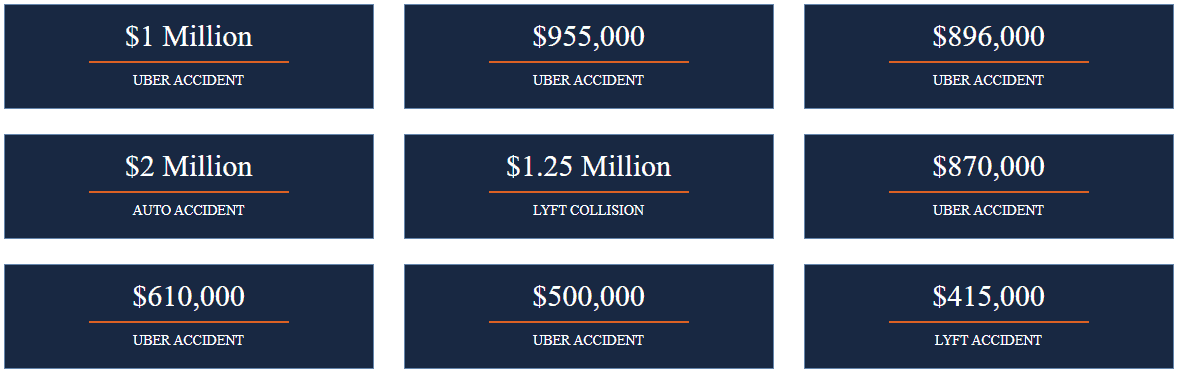

Which law firm has the best Lyft accident settlements online?

On its website, Kenmore Law Group (in California) lists two Lyft accident settlements. One was for $1.25 million, and another was for $415,000.

This was a screenshot of their rideshare accident page:

Those are some big settlements! Unfortunately, the facts of those cases are not listed. So I don’t know who was at fault, or how badly the victims were hurt.

I will say this:

To get that kind of compensation, you need really serious injuries. At least that’s the case in Florida (where I practice).

Even if you have the best Lyft accident attorney, you will likely need a broken bone and three (3) surgeries to get an insurance company to pay you $500,000 in a Lyft accident. Or you will need to have a brain bleed or a diffuse axonal injury, which is the shearing (tearing) of the brain’s nerve fibers (axons) that happens when the brain is injured as it shifts and rotates inside the bony skull.

You may also be able to get a payout of $500,000 (or more) if your family member was killed in an Lyft car accident.

Basically, do not set your expectations too high after looking at those payouts. If you have minor injuries, even the top Lyft accident lawyer won’t be able to get you a mid six figure settlement. At least this is the case for Lyft accidents in Florida.

I do not know anyone at the Kenmore Law Group.

What Questions Will Lyft Ask You If You Call to Report an Accident or Collision?

The Lyft representative will likely ask you many questions. Their goal is to setup the claim and forward it to their claims handler for the state where the accident happened.

Will Lyft’s First Settlement Offer Be Close to Their Final Offer for Your Injury Claim?

Not from my experience. In the above case that I settled, Lyft’s insurer paid $45,000 of the $70,000 settlement. Their opening offer was $16,000.

Their initial offer was for 36% of their final offer. If we would’ve accepted the initial offer, we would’ve missed out on $29,000.

In most injury cases, it isn’t smart to take their first settlement offer!

How Collision Coverage Works in an Lyft Car Accident (Example)

Let me give you an example of how collision coverage works in an Lyft accident case. Assume that Matt is driving for Lyft with a passenger. Matt is the front car that is rear ended by another car. We’ll call Matt’s car #2. GEICO insures Matt’s car with collision coverage. However, when Matt got insurance, he never told GEICO that he drove for Lyft. (That was a poor decision.)

Car #1 hits Matt’s car. State Farm insures car #1. Matt’s car is damaged badly. After the crash, a tow truck tows the car to the tow yard.

First, Matt should get his car out of the tow yard.

Why?

Because the tow yard will charge a daily fee to store his car. Not everyone has money lying around to pay for this.

If Matt has a car towing service like AAA, he should use them to tow the car out of the tow yard.

Let’s assume that State Farm only insures car #1 with $10,000 in property damage (PD) liability coverage. (Remember, car #1 is at fault for this accident.) Unfortunately, having $10,000 in PD liability complies with Florida’s auto insurance requirements. I’m referring to the PD liability insurance requirement for private passenger cars.

The most that State Farm will pay to Matt for his car damage is $10,000. If Matt’s car damage is over $10,000, then it is in Matt’s best interest to make a collision damage claim with his own collision coverage with GEICO. Shortly after receiving the claim, GEICO will deny the claim because Matt never told them that he was driving for Lyft. This is considered a material misrepresentation. It is grounds for GEICO to deny coverage.

However, Matt can then show Lyft’s claims adjuster (Constitution State Services/Travelers) a copy of the GEICO’s written denial of collision coverage. Matt will also need to show Lyft’s insurer his GEICO declarations page. Lyft’s insurance company will only pay for Matt’s collision damage if he was engaged in a ride. Fortunately for him, he was.

Earlier, I said that GEICO insured Matt with collision coverage. Since Matt was engaged in ride and had collision coverage, Lyft’s insurer will pay for Matt’s car damage up to its actual cash value. However, Matt will have to pay a $2,500 deductible.

The good news?

Lyft’s insurance company should pay Matt’s car damage rather fast.

What happens if you were in a Lyft and another driver hit you but the crash report does not list any insurance for the other driver?

If the Lyft car was damaged, Lyft’s insurance company will assign a collision adjuster to the claim. That collision adjuster has access to see if the other car had insurance at the time of the accident. Insurance companies have access to this information. You don’t.

You (or your lawyer) can ask the collision adjuster to give you the name of the other driver’s insurance company. If a claim has been set up, they can also give you (or your attorney) the claim number and adjuster’s contact information.

Remember:

If Lyft’s insurance company pays for the damage to the Lyft car, they want to get this money back if another car caused the crash. If you are injured because the other driver was careless, you also want to know if that other car has bodily injury liability (BIL) coverage.

Why?

Because Lyft’s uninsured motorist (UM) coverage does not kick until your claim is worth more than the other driver’s BIL coverage. This assumes that Lyft has uninsured motorist coverage. Currently, they do not.

In a moment, I will talk about this in detail.

Who Pays for a Lyft Driver‘s Rental Car if His Car Was Damaged in the Accident?

Either the Lyft driver’s personal auto insurer or the at fault party’s insurance company will pay to get the Lyft driver a rental car.

Let me explain using an example.

Assume that Matt is driving for Lyft. Maybe he has a passenger or maybe he does not. Another driver (Bob) runs a red light and hits Matt’s car. Matt’s car is damaged. USAA insures Bob.

As a result of the impact, Matt’s car is badly damaged. And he needs a car so that he can continue to drive for Lyft and support himself.

Matt sets up a claim with USAA. Or maybe Bob reported the accident to USAA. Either way, Matt is hopeful that USAA will quickly get him a rental car and fix his car.

The bad news?

Anyone who has been through the claims process knows that it takes time for an insurance company to clear (approve) coverage. For starters, USAA will call Bob and make sure that he was not driving for Uber, Lyft, Uber Eats, Grubhub or any delivery service at the time of the accident. Sometimes, USAA (or any insurance company) will have a tough time getting into contact with its insured. People are busy and delays happen.

Why does USAA need to confirm that Bob was not driving for a rideshare or delivery service?

Because if Bob was working for a rideshare company or delivering for a food service at the time of the accident, USAA (or any insurance company) will deny coverage. This means that they will also deny property damage liability coverage. Basically, USAA will not pay for Matt’s car damage. However, the rideshare or delivery service’s coverage would pay for the damage to Matt’s car. But if Bob was driving for a rideshare or delivery service it will likely cause an additional delay if Matt wants to get his rental car paid for “through Bob”.

As stated above, Matt was driving for Lyft at the time of the accident.

Lyft Does Not Provide Rental Car Reimbursement Coverage

However, Lyft’s auto insurance policy does not provide rental car reimbursement coverage. Thus, Matt has to hope for one of two things. One, he purchased rental car coverage on his personal auto policy (with a rideshare endorsement). Or two, USAA (or whoever ultimately insures Bob) quickly clears coverage.

If Matt has rental car reimbursement coverage on his personal auto policy (with a rideshare endorsement), his personal auto insurance company will pay for his rental car. They will pay for Matt’s rental car for a reasonable time until his car gets fixed. However, some auto insurers will not start paying for the rental car until the car is at the body shop and repairs have begun.

In sum, because delays often happen, Matt should set up a rental car reimbursement claim through his personal auto insurer (if he has a rideshsare endorsement). Additionally, Matt should ask Bob’s insurance company to get him a rental car. Matt should use rental car reimbursement coverage through whichever insurance company gets the rental car setup the quickest.

Also, after the accident, Matt should rent a car with his own money. This is the quickest way to get back on the rode. Later, he can get reimbursed for it. However, if Matt wants to continue driving for Lyft, he needs to make sure that Lyft knows about the rental car.

I also want to make something clear. Earlier, I said that Lyft does not have rental car reimbursement coverage on its insurance policy. This is true.

However, if someone is driving for Lyft and damages your car, Lyft always has property damage liability coverage. Property damage (PD) liability coverage pays for damage to the other driver’s car. It does not pay for damage to the Lyft driver’s car. Property damage liability coverage also pays for the other driver’s rental car.

Why You Should Hire a Lyft Accident Attorney

If you are injured, you should hire a Lyft accident lawyer. In rideshare accident cases, you will often have to deal with more adjusters than in a typical car accident.

Often times, you’ll deal with a minimum of 6 different claims adjusters (usually from different insurance companies). Sometimes you may wind up dealing with 7 to 9 (or more) insurance claim adjusters in one Lyft accident claim!

That means you’ll have to call and email a whole lot of people for one claim.

You’ll often have to leave voice messages with different adjusters requesting a call back. Sometimes adjusters are handling another claim when you call them. Other times, they are out of the office.

Don’t expect handling a Lyft accident claim on your own to be fun. It won’t be. Count on it being stressful.

Thus, you may get overwhelmed and frustrated. This is especially true because you won’t have a case management program that sorts the claim information in the right areas. This makes taking notes simple when an adjuster calls you or if you call them.

Here is another reason to hire a Lyft accident attorney:

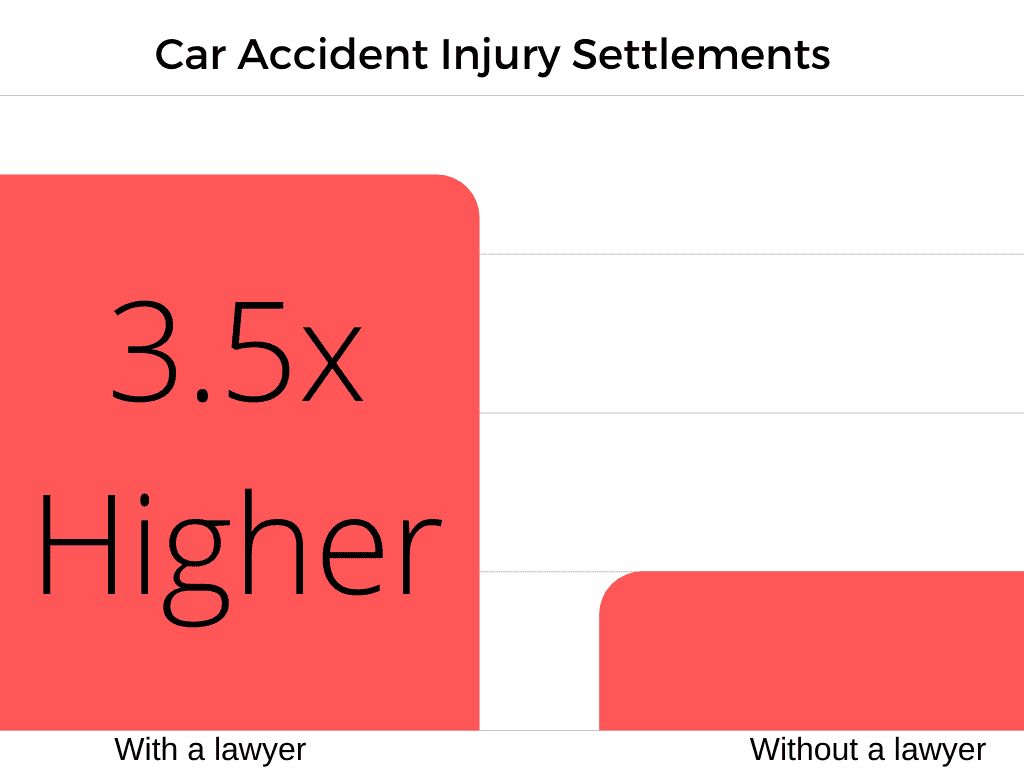

A 1999 Insurance Council Study revealed that people with an attorney got a 3.5 times bigger settlement then those without a lawyer.

Insurance research council (1999)

I will also help with you your property damage claim free of charge. We only charge on fee on any property damage recovery if I (as your Lyft accident lawyer) have to sue.

But don’t worry:

The odds are high that I will not have to sue to get your property damage claim paid.

How Long Does Lyft Take To Send You a Settlement Check in an Injury Case?

Once you reach a settlement with Lyft’s insurance, they should send the check fast. You should likely get it within 2 weeks.

However, the tougher part of the claim is to get a settlement. In my Lyft accident settlement, Lyft’s insurer quickly sent me the $45,000 check after we agreed upon settlement release language. It took about a week or so to receive the check.

This was in a personal injury case. Some states have laws that give a car insurance company a certain time to give you your check. For example, in Florida, Lyft’s insurer must send you the check within 20 days of you signing a settlement release.

Passenger Got PIP Benefits Through Lyft’s Insurance (York Handled the Claim)

The passenger got PIP medical benefits through York because he didn’t own a car in Florida, or live with a relative who owned a motor vehicle. As a Lyft accident attorney, I knew this. Thus, I quickly sent my client an affidavit (sworn form) that said that the Lyft passenger did not own a car (or live with a relative who did).

York paid $10,000 of PIP benefits to the passenger’s medical providers for medical treatment.

This crash happened in late 2016.

Let’s assume that this accident would have happened today in Florida. Currently, Lyft is not required to give PIP benefits to passengers. Florida Statute 627.748(7)(c)1.b. This law doesn’t require Lyft to give any PIP benefits when the car is en route to pickup passengers or during trips.

PIP is limited to $2,500 if you are not diagnosed with an “emergency medical condition“.

There is another reason to quickly get medical treatment (if you need it). The value of your pain and suffering drops each day that you wait to get medical treatment. At least according to car insurance companies. And there is no reason why Lyft’s insurance company would treat your case any differently.

Does a Lyft Passenger’s PIP Pay Medical Bills and Lost Wages if They Owned a Car?

If a Lyft passenger owned a car on the day of the crash, the passenger’sPIP insurance may pay some of the passenger’s medical bills and lost wages. If the passenger has a Lyft accident attorney, he or she can complete the PIP form for the passenger.

Does a Lyft Passenger Relative’s PIP Pay Medical Bills and Lost Wages if the Lyft Passenger Did Not Own a Car?

If a Lyft passenger didn’t own a car on the day of the crash, the passenger’s resident relative’s PIP insurance may pay some medical bills and lost wages. If the passenger has a Lyft accident attorney, he or she can help the passenger complete the forms to get PIP coverage from the relative.

Lyft Driver’s Personal Policy Will Likely Deny Coverage

If you didn’t own a car or live with a resident relative who owned a car on the date of the accident, then most Lyft driver’s personal auto insurance policies won’t pay PIP benefits.

This is since, in Florida, most Lyft driver’s personalauto policies will likely deny coverage because the Lyft driver was being paid a fee while driving. Most Florida personal auto policies have an exclusion when the insured is driving for a fee. And most Lyft drivers do not purchase rideshare coverage on their auto insurance policy.

A Lyft driver may make a PIP claim with his/her personal auto insurer. If this insurer doesn’t know that the driver was working for Lyft when the accident happened, they may (possibly incorrectly) approve the Lyft driver for PIP.

Warning! Drivers should never lie to any insurer.

If the Lyft driver’s personal insurer approves the Lyft driver for PIP, then they may cover the passenger for PIP even if they learn that the car was being operated as a Lyft. Once they provide PIP coverage for the driver, they may also cover the passenger.

Can a Lyft driver get PIP benefits through Lyft for a Florida car accident?

Yes, if the Lyft driver’s personal car insurance company denies Personal Injury protection (PIP) coverage. If this happens, you (the Lyft driver) should quickly send Lyft’s insurance company a copy of the denial letter.

Why would the driver’s personal car insurer deny PIP coverage?

The driver’s personal auto insurer may deny coverage if the Lyft driver never told them that they drove for Lyft. GEICO and all insurance companies will deny PIP coverage if you don’t tell them that you drive for Lyft.

Can a Lyft passenger get PIP through Lyft for a Florida car accident?

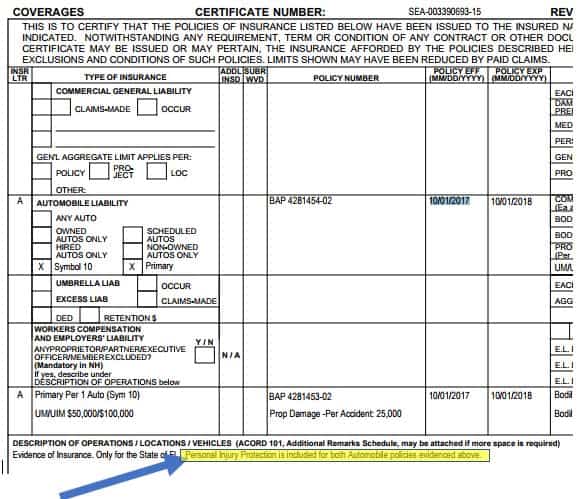

As stated earlier, Lyft’s certificate of liability insurance includes PIP for passengers. PIP is included on all Lyft automobiles in Florida.

What happens if a Lyft passenger didn’t own a motor vehicle or live with a resident relative who owned a motor vehicle in Florida?

In this scenario, the passenger qualifies for PIP with Lyft’ insurance company. Thus, Greenwich Insurance (or Lyft’s current insurer) would pay the PIP benefits.

York Risk Services Group Claims (“York”) was handling Lyft claims. Now, Lyft uses different insurance companies for different states. For example, Travelers (Constitution State Services) handles Greenwich Insurance Company’s claims in Florida.

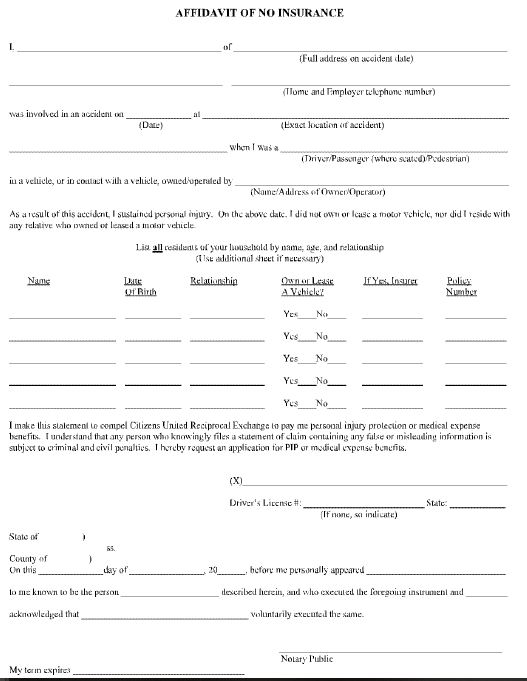

In this scenario, a passenger will need to complete a Lyft Claim for PIP – Affidavit of No Insurance. If you have a Lyft accident attorney, he or she can complete this form for you. You’ll then need to get it notarized. This will get Lyft’s insurance company to begin paying your medical bills and lost wages.

Sometime after the Lyft accident occurred that resulted in my $70,000 settlement, York started using a different Affidavit of No Insurance.

Here is Lyft’s Affidavit of No Insurance, as of July 27, 2018:

Lyft’s Affidavit of No Insurance – PIP

You may need to edit the form so that it fits your set of facts.

Lyft’s insurance company will also ask you to complete a PIP Application.

Is Lyft’s insurer entitled to take a passenger’s statement if he makes a PIP claim with them?

Actress.

Yes. In Florida, an insured seeking PIP benefits, including a passenger, must comply with the terms of the policy. This includes, but is not limited to, submitted to an examination under oath. Florida Statute 627.736.

What can a Lyft’s claims adjuster ask a Lyft passenger during a PIP statement?

The area of questioning during the examination under oath is limited to relevant information or information that could reasonably be expected to lead to relevant information. This is a pretty liberal standard. That said, I recommend hiring a Lyft accident lawyer so that your rights are protected. Your lawyer can keep the insurance adjuster in check.

Compliance with this is a condition precedent to receiving benefits. An insurer that, as a general business practice as determined by the office, requests an examination of a passenger without a reasonable basis is subject to s. 626.9541.

Does Lyft Have Medical Payments (“Medpay”) Coverage?

If you look at Lyft’s insurance policy with Zurich, you won’t see Medpay insurance.

However, I represented an injured passenger. Lyft’s PIP insurance paid 100% of his medical bills up to $10,000. Basically, Lyft’s PIP also paid the 20% of the passenger’s medical bills that Medpay would’ve paid.

Thus, in essence, Lyft’s PIP was also acting like Medpay.

It may pay for the medical bills the 20% that Lyft’s PIP doesn’t pay, up to $10,000.

Bills Should Be Submitted to Health Insurance (After PIP Pays)

In Florida, your health insurance coverage should pay medical expenses that PIP and Medpay do not pay. In Florida, health insurance is secondary to PIP and Medpay.

This means that PIP needs to be billed first. After PIP and medical payments coverage are billed, your health insurance may pay the bills.

Can You Sue a Lyft Driver if the Lyft Driver Didn’t Cause the Crash?

No. However, you can hire a Lyft accident lawyer to sue for uninsured motorist (UM) coverage if you are entitled to UM coverage. Maybe you own a car that has UM coverage. Likewise, if you lived with a relative who had UM coverage on a vehicle, you may be entitled to their UM coverage.

While you technically could sue without a lawyer, this would a terrible decision. Why?

Because court laws in an uninsured motorist lawsuit arising from a Lyft car accident are very complex. For the past 16 years, I have handled car accident cases. And I still learn something new every week! That shows you how complex the law (in my case Florida law) is.

Bottom Line:

Hire a Lyft accident attorney for your claim. It’s the easier, softer way.

In order for a passenger to be entitled to Lyft’s UM insurance, another vehicle must have negligently caused the crash. Also, the other vehicle must have been uninsured or underinsured.

Above, I used the word “sue”. However, the reality is that most in most UM claims do not result in lawsuits. This is in large part because most car accidents do not result in serious injuries.

However, the passenger (or his or her Lyft accident lawyer) can try to settle the case without a lawsuit. The passenger will have the greatest chance of settlement if the claim is properly documented. This is where an attorney comes into play. One of the benefits of hiring a personal injury lawyer is that he or she knows how to properly document the case.

On the other hand, you may need to hire a Lyft accident attorney to sue in some situations. Sometimes lawsuits are not avoidable. Sadly, most insurance companies try to save money (on claims) at the expense of injured car accident victims.

What happens if you have your Own Non-Stacking Uninsured Motorist (UM) Insurance?

If you have uninsured motorist coverage on your car, you need to look to see whether the UM coverage is stacking or non-stacking. Your car insurance declarations page will say whether your coverage is stacking or not.

If your UM coverage is non-stacking, then Lyft’s uninsured motorist insurance pays before your own car insurance has to pay any money. Let me give you an example.

Mike accepts a ride on the Lyft platform as Lyft driver in Miami Beach, Florida. Sara is a passenger in the Lyft car. Another car crashes into the back of the Lyft car. Nationwide Insurance Company insures Sara’s car with $10,000 in non-stacking uninsured motorist coverage.

As a result of the accident, Sara breaks her arm and has surgery. The at fault car only has $10,000 in bodily injury liability insurance coverage.

Since Sara was a passenger in a Lyft, she is entitled to up to $250,000 in UM coverage. Since her UM coverage on her personal car is nonstacking, her uninsured motorist injury insurance case must be worth more than $260,000 before her personal UM coverage has to pay. The $260,000 amount is the total available UM coverage on the Lyft car in addition to the at fault car’s $10,000 BIL limit.

If You Have Stacking Uninsured Motorist (UM) Insurance, Will Lyft’s UM Coverage Pay?

If your personal UM coverage on your car insurance policy is stacking, then both your personal and Lyft’s UM coverage pay on a pro-rata basis. Fidelity & Casualty Co. of New York v. Chacon, 408 So.2d 812 (Fla. 3d DCA 1982); State Farm Mutual Automobile Insurance Co. v. Colonial Penn Insurance Co., 379 So.2d 1036 (Fla. 3d DCA 1980).

Let’s take the above example above except assume that Sara’s UM car insurance coverage is stacking UM. To keep it simple, let’s assume that the car that hit her is uninsured.

If Sara has $10,000 in UM coverage with Nationwide and $250,000 UM coverage with Lyft’s insurance company, her total UM coverage is $260,000. Assume that she sustains damages (pain, suffering, medical bills, lost wages, etc.) of $200,000.

Nationwide would pay $8,000 (4%) and Lyft’s insurance company pays $192,000 (96%). Nationwide pays 4% because it’s policy has $10,000 of UM coverage. The total UM coverage is $260,000. $10,000 divided by $260,000 is 4 percent.

Likewise, Lyft’s UM limit ($250,000) divided by the total available UM coverage ($260,000) is 96%.

In the two examples above, I have kept it very simple. However, you should hire a Lyft accident attorney because these cases are complicated.

When is Lyft’s Insurance Company Most Likely to Pay You the Policy Limits for Your Injury?

This is most likely to happen if you are a Lyft driver on your way to pickup a passenger and an uninsured car causes the accident.

In this scenario, Lyft’s insurance company is more likely to pay you the limits because this is when Lyft’s insurance limit is the lowest. Specifically, Lyft has a $20,000 uninsured motorist insurance limit in this instance. This is the lowest insurance limit that Lyft ever has. And Lyft’s insurance company is much more likely to pay out the policy limits when they are low.

I recommend hiring a Lyft accident lawyer who will fight to get you fair value for your case.

Example When Lyft’s Insurance Company Most Likely to Pay You the Policy Limits for Your Injury

I just told you when Lyft’s insurance company is most likely to pay you the policy limits for your injury. Now, let me you give an example.

Bob is a Lyft driver who accepted a ride request. He is on his way to pickup a passenger. When doing so, an uninsured driver rear ends Bob. Bob’s car is badly damaged.

Bob takes an ambulance to the hospital. Bob has pain in his neck, back and knee. Over the next few months, Bob receives treatment for his neck and back pain. He does not get an MRI of his neck or back.

Here, Lyft’s insurance company is more likely to pay Bob the policy limits than in other situations. This is because the uninsured motorist injury limit is only $20,000 in this instance. Bob should hire a Lyft accident lawyer to look for all available coverage so that he does not leave any money on the table.

On the other hand, if Bob had a passenger in the car, Lyft’s UM limit would be $250,000 per accident. And Lyft’s insurance company would not pay Bob $250,000 (or close to it) for pain in his back, neck and knee.

When is the 2nd Most Likely Scenario Where Lyft’s Insurance Company May Pay You the Policy Limits for Your Injury?

If you are hit by a Lyft car (who is at fault) that is logged in to the platform but has not accepted a ride and you are not inside the Lyft vehicle. You could be in another car, a pedestrian, or on a motorcycle or bike.

In this scenario, Lyft’s insurance company is more likely to pay you the limits because – here – Lyft’s insurance limit is the 2nd lowest. In this instance, Lyft has a $50,000 bodily injury liability limit per person. Again, Lyft’s insurance company is much more likely to pay out the policy limits when they are low.

However, you will still need a decent injury in order for Lyft to pay you the $50,000 per person BIL limits. If two or more other people (who are not in the Lyft car) were also hurt, this puts more pressure on Lyft’s insurance company to pay the $50,000 per person limits. This is because more than one person is competing for the same $50,000 (per person) pot of money.

You should hire a Lyft accident attorney to put pressure on the insurance company to pay the limits.

Example Of The 2nd Most Likely Scenario When Lyft’s Insurance Company May Pay You the Policy Limits for Your Injury

Bob is a Lyft driver who is logged onto the Lyft platform but has not accepted a ride request. Bob rear ends another car.

There are two occupants in the other car. As a result of the accident, one of the passengers breaks her wrist (and gets surgery). The other occupant (of the other car) has a rotator cuff tear. He gets shoulder surgery.

Here, Lyft’s insurance company should quickly pay each occupant the $50,000 BIL insurance limits.

Why?

Because each of the other car occupants’ injuries is clearly worth over $50,000. In a moment, I will list many injuries that have a pain and suffering value that is over $50,000. Keep in mind that pain and suffering is just one component of damages. Lyft (or another driver) may also be liable for medical bills, lost wages and other damages.

However, each occupant should hire a Lyft accident lawyer to maximize their case value.

Which Injuries Are Worth Over $50K in a Lyft Claim?

If you look at past jury verdicts, you’ll see that some injuries consistently have a full value of pain and suffering of over $50,000.

Some of these are injuries are if you have surgery to fix a:

Even without surgery, Travelers should pay the $50,000 per person limits for upper leg bone (femur) fracture. They may even pay the $50,000 per person limits for a lower leg bone (tibia or fibula) fracture without surgery. I settled a case with GEICO for over $64,000 for a leg (fibula) fracture.

Therefore, if the Lyft driver had the app on, but wasn’t engaged in a ride, Travelers may quickly pay the $50,000 per person limits for the above injuries. This assumes the Lyft driver’s negligence caused the injury.

When will you get the settlement check after you settle your case?

Most insurance companies send the settlement check within a few days after the settlement. I have no reason to believe that Lyft’s insurance company would be any different.

Here’s a tip that I use when I’m close to settling a car accident case. Whether you are an injured victim or a Lyft accident lawyer, you can use this tip in your car accident claim.

Right before you are about to settle for an agreed upon amount, tell Lyft’s insurance adjuster that you will accept their offer if they send you the check overnight. If the adjuster really wants to settle the case, they may agree to do so.

If they can’t send it to you overnight, ask if they can send it to you via two day mail.

The main point is that the time to ask is immediately before you are about to accept Lyft’s settlement offer. Not after.

Why?

Because once you settle your case with Lyft’s insurance company, they don’t have any reason to send you the check overnight. This is true for all insurance companies.

And don’t ask them too early on in your case to overnight your settlement check. They’ll think that you are desperate to settle and may offer you less money.

What if there are several claims against the Lyft driver for the accident?

If there are many claims against the Lyft driver for injuries and property damage, Lyft’s insurance company may pay out the liability policy limits quicker. This is not unique to Lyft’s insurance company. Any insurance company would do this.

However, this will only happen if the Lyft driver is at fault for causing the accident.

If Lyft’s insurance company agrees to pay out the liability policy limits to several injured people, they will likely hire a lawyer to do this. (Uber’s insurance company (or any insurer) would also do this.)

The following is the procedure that most (if not all) insurance companies follow when paying out the limits to several people.

Lyft’s insurance company (or its attorney) may send you (or your attorney) a letter stating that they have agreed to tender (payout) the policy limits for all claims. Lyft’s insurance company may schedule a global settlement conference, or they may let you (or your lawyer) try to reach an agreement splitting up the money with the other injured claimants (or their attorneys).

If everyone (and their Lyft accident lawyers) can agree on how to split of the policy limits, then you don’t need to go to a global settlement conference. This saves you time, stress and potentially mediation fees.

If you (or your attorneys) can’t agree on how to split up the money, then you can give Lyft’s insurance company the names of mediators that you like. A mediator is someone (usually an attorney) who tries to get all sides to settle the case.

Before this mediation, ask Lyft’s insurance company’s attorney if they will agree to pay for the mediator’s cost. A good mediator can cost up to $4,000 for half a day. That amount is split up between the parties. For example, if there are 4 people making claims, each may have to pay $1,000 to the mediator.

Some mediators charge much less than $3,000 for half a day.

How does it affect you if Lyft’s insurance company agrees to pay out the limits and there is more than one claim?

Sometimes there is more than one person who is making a claim against the Lyft driver for the accident. In this case, you may get a great payout, or you may get a bad payout. Let me explain.

The worst case scenario for you is that you and someone else (other than the Lyft driver) is very badly injured. This is because there likely won’t be enough money to fairly compensate you.

Here is an example:

Assume that you are passenger in a Lyft car. The Lyft driver runs a red light and crashes into another car. You are unconscious at the scene. The paramedics take you to the hospital. You are in a coma for several days or weeks. Doctors perform emergency surgery on a burst fracture in your spine (back or neck).

Assume that the passenger in the other car was paralyzed or had a serious brain injury.

A serious brain injury (and spine surgery), or paralysis, is alone worth Lyft’s $1 million liability insurance limit.

But there’s a problem:

You’ll have to split the $1 million limit with another person making a claim. Since your injuries are worth the amount of the policy ($1 million), this is bad for you. Your case would be much better if you were the only one hurt in the accident. Then, you’d get the $1 million to yourself.

That was the worst case scenario.

On the other hand, your best case situation is that your case and the other peoples’ cases are worth a little less than the $1 million liability limit. In that instance, Lyft’s insurance company may pay faster and more money than you would get if you were the only one injured. Lyft’s insurance company may be less likely to delay your settlement by asking for your past medical records or other documents.

If You Weren’t Wearing a Seat Belt, Does This Affect Your Injury Claim?

Possibly. The first question to ask is, “Was the occupant wearing a seat belt?”

If the answer is No, then you must ask, “Was there an operational and available seat belt in the car?”

If there was an operational and available seat belt, but the occupant wasn’t using it, the insurance company may argue the “seat belt defense”.

The injured person’s compensation should be reduced accordingly. The person who wasn’t wearing a seat belt should expect the responsible insurance company to make this argument. They may make this argument even if the injured person was a back seat passenger.

Maybe Lyft’s insurance adjuster will be a little more understanding for back seat passengers who were not wearing a seat belt. However, do not count on it.

I settled a case (not involving Lyft) for $170,000 where my client was not wearing a seat belt. However, in that case, the bodily injury liability adjuster mentioned my client’s failure to wear a seat belt on almost every phone call. In that case, my client was a back seat passenger.

What if a Lyft driver hit you while you were on a bike?

To get compensation, the Lyft driver must be at fault for causing the accident. The Lyft driver is likely at fault if he or she hit you while you were riding a bike in a crosswalk. Your case is better if the front of the Lyft car hit you instead of you hitting the side of Lyft car.

If you are badly injured, your best case scenario is that the Lyft driver had already accepted a ride request, or had a passenger. This is because Lyft’s $1 million liability limit will apply.

For example, let’s say that you were lawfully riding a bike in the crosswalk. A Lyft driver hits you. You get thrown to the street and land on your ankle. You have pain in your ankle.

Paramedics take you to the hospital. There, doctors diagnose you with a trimalleolar ankle fracture. They perform surgery on it, which includes putting in a plate and screws.

Your best case is if the Lyft driver had accepted a ride request or had a passenger. This is because trimalleolar ankle fractures have a pain and suffering value of over $250,000 in South Florida. The Lyft driver is also responsible for your medical bills and lost wages. If you stay a few days at the hospital and have ankle surgery, the hospital bill can easily be over $100,000.

In Florida, in certain situations, Lyft’s PIP insurance coverage will pay up to $10,000 towards the bicyclist’s medial bills and lost wages. PIP coverage is in addition to the Lyft driver’s liability insurance coverage.

This chart shows when Lyft’s PIP coverage will pay a bike rider if a Lyft driver hits him/her in Florida:

Bike Rider’s residence

Will Lyft’s PIP cover the bike rider?

International visitors to Florida

No

Visitors to Florida who live in another state

No

Florida residents who own a car

No

Florida residents who live with a relative who owns a car.

No, if the relative’s auto policy has PIP (and coverage isn’t denied).

Florida residents who don’t own a car and don’t live with a relative who owns a car.

Yes, if the Lyft driver had the Lyft app on but had not accepted a ride request.

Is Lyft’s Insurance Company Good?

Currently, Lyft has several insurance companies. Companies like State Farm and Progressive have a reputation for being cheap. Travelers has a better reputation than State Farm and Progressive.

The good news?

Travelers has a reputation for paying above average for personal injury claims. However, don’t get to excited. They are still an the insurance business. Their goal is to pay you as little as possible.

However, keep in mind that Travelers does not insure Lyft. It merely acts as a claims administrator. In Florida, Greenwich is currently the insurance company.

Travelers’ reputation is similar to USAA in regard to paying above average for injury settlements. Hire a Lyft accident lawyer who has settled several injury cases with Travelers (even if they insured someone other than Lyft.)

Can You File a Lawsuit Against Lyft?

No. However, you can hire a Lyft accident lawyer to sue the Lyft driver if he was careless and your are injured. Likewise, if you have a UM insurance claim with Lyft’s insurance company, and they aren’t making a fair offer, you can hire a Lyft accident lawyer to sue.

Can One Attorney Represent You and Another Lyft Passenger for Your Injuries from an Accident?

To answer this question, we first must look at what your relationship is with the other Lyft passenger. If the other passenger is your family member, then the same attorney will most likely be able to represent both of you.

However, if the other Lyft passenger is a boyfriend, girlfriend or friend, then the answer becomes more difficult. Let me explain.

In a state like Florida, an attorney cannot represent two individuals (who are not family members) who are competing for a limited amount of liability of bodily injury liability (BIL) insurance. Florida Bar rules prevent this. See Ethics opinion 02-03. It should be a big warning flag for you if you are speaking with an attorney who is willing to break this rule.

A boyfriend, girlfriend or fiance is not considered a family member.

A Lyft accident attorney who is willing to represent two or more passengers who are not family members (when 3 or more people are making claims) against a limited amount of BIL coverage should be a warning sign to you for three reasons.

First, perhaps the attorney does not know the Florida bar ethics rules. What’s the big deal about hiring a lawyer who does not know the Florida bar’s ethics rules?

The second problem is that the lawyer may know the ethics rule but his or her greed is causing them to disregard the rule. Either one of the above reasons is cause for major concern.

Do you want a greedy lawyer?

I doubt it.

Third, if you are competing against a limited amount of BIL coverage, then the more money that you get, the less money than one of the other passengers gets. This is a conflict of interest if you are not related to the other Lyft passenger.

Example of when a Lyft accident lawyer attorney can’t represent two people

Let’s assume that while Miguel is driving for Lyft, he runs a red light and hits another car. At the time of the crash, Peter and Joana are passengers in the Lyft car. They are good friends.

As a result of the impact, Peter fractures his pelvis. (The pelvis is the complex of bones that connects the trunk and the legs.) At the hospital, Peter undergoes 3 surgeries to his pelvis over a period of 9 days. A pelvis fracture with surgery is worth a lot of money.

An ambulance takes Joana to the hospital where an MRI of her head reveals that she has a diffuse axonal brain injury. She has some dizziness, headaches and memory loss. Joana misses a month of work, but then goes back to work as a janitor.

Can one Lyft accident attorney represent both Peter and Joana in their personal injury claims against the Lyft driver?

No, unless Peter or Joana has plenty of uninsured motorist (UM) coverage under a personal auto insurance policy. But that is not common. Many people have low limits of UM coverage on their car insurance. In Florida, most drivers do not have UM coverage.

Assuming that Peter or Joana does not have a huge amount of UM on a personal car insurance policy, an attorney cannot represent both Peter and Joana because their combined injury claims are worth more than Lyft’s $1 million liability insurance limit. Basically, as the attorney gets more money for Peter, Joana will get a smaller settlement.

For example, if Peter gets a $600,000 settlement, Joana will get $400,000. (Lyft’s combined liability limit is $1 million.) How can one attorney fight to get Lyft’s insurance company to offer Peter more money?

He or she can’t because this will result in Joana getting less money. This is a conflict of interest because Peter and Joana are not family members. Peter and Joana cannot agree to waive this conflict of interest. See Ethics opinion 02-03

This is true even if a Lyft accident attorney says that they can waive it. The lawyer is wrong.

The vice versa is true as well.

Peter and Joana need to hire separate Lyft accident lawyers so that their rights are fully protected.

Is the Coronavirus affecting Lyft accident claims and settlements?

Greenwich Insurance Company insures Lyft. AXA XL owns Greenwich. Just look at AXA’s stock price below:

As you can see, it has takena huge financial beating by COVID-19. The Coronavirus has hit AXA much harder than Uber’s insurance company (Progressive in most states).

In Florida, Travelers handles claims for AXA XL (Lyft). Therefore, Travelers may be making smaller offers until AXA XL has recovered financially from the Coronavirus. And that may take a long time.

Can Lyft’s Insurer Require You to Go to a Doctor That it Selects?

Maybe. In Florida, uninsured motorist policies typically have wording that require you to show up at a medical examination (CME) conducted by a doctor of their choosing.

Lyft’s insurance company likely has this language in its insurance policy. A passenger is considered an omnibus insured under an auto insurance policy.

If you have a Lyft accident attorney, he or she may be able to attend this exam with you. If you are badly injured, I am happy to attend this exam with you. In big injury cases, I may bring a videographer to make sure that Lyft’s doctor accurately reports your complaints and his exam in his medical report.

What If You’re Visiting Florida, and You’re Injured in a Lyft Accident?

If you’re injured in a Lyft accident in Florida, while visiting from another state, the claim gets more complex. The out of state visitor is usually in Florida for one of two reasons. They are either here for:

A vacation (or pleasure)

Business (work related)

In either instance, the injured person is even more likely to need a Lyft personal injury lawyer to protect their rights. This is because multiple state laws may apply.

Let’s first look at the slightly more complicated of the two above situations. That is, someone who is injured in an Lyft accident while in Florida for work purposes.

What Happens if You’re Hurt in an Lyft Accident in Florida While on a Business Trip from Another State?

Let’s assume that you’re visiting Florida for work purposes. You live in another state. Maybe you’re a consultant, or perhaps you deal with cyber security. Or maybe you have some other type of job. Regardless, you’re in Florida on a business trip.

If you’re injured while you are a passenger in an Lyft, you should report the accident to your employer.

Why?

Because you don’t want to lose potential valuable workers’ compensation coverage by not reporting an Lyft accident to your employer.

Once your employer’s workers compensation insurer gets notice of the Lyft accident, it will do one of two things. Workers comp will either accept the claim as compensable, or deny the workers compensation claim.

If the workers compensation insurer accepts the claim, it will pay for all necessary medical treatment and hospitalization services. Workers compensation will also pay around 66 2/3% of your lost wages caused by the Lyft accident.

If workers’ compensation denies the claim, it will likely say that you were not in the course and scope of your employment at the time of the Lyft accident. This may (or may not) happen if you get hurt while you were in an Lyft on the way to somewhere that was not specifically business related. An example is a meal that was not a “business lunch or dinner” with a client.

Even if the workers’ compensation insurer denies benefits, it may be dead wrong. This is because, even if you’re out of state law doesn’t cover you, Florida workers’ compensation law will likely cover you if you were injured in an Lyft accident while in Florida for business travel. Florida’s workers compensation laws are very (broad) generous in this regard.

Again, the key is to report the Lyft accident to your employer. Report the accident even if you think you will be at the company for the rest of your career.

I’ve represented people who were injured in an accident. They thought that they would be a lifelong employee at their company. Yet, at some point during their claim their company fires them. Additionally, the economy can tank at any time. As we have seen with the Coronavirus, we never know what may happen.

In addition to a workers’ compensation claim, you should make a PIP claim with Lyft. Lyft’s insurance policy has PIP.

Further, the Lyft passenger can make a personal injury claim against the at fault party for causing his or her injury. If the Lyft driver was careless and caused the crash, Lyft’s insurance company is on the hook. If a driver of another car caused the accident, then the other driver’s insurance company is owes you compensation.

This can result in a big savings to you! Your ability to reduce the workers’ compensation lien will depend on the out of state workers compensation law.

Lyft’s Express Drive program helps you rent a car so you can start driving in select cities through Lyft’s rental partners, Avis Budget Group, Flexdrive, and Hertz. In Florida, Express drive through Hertz is offered in Miami, Orlando and Tampa Bay.

Express drive with Avis is offered in Jacksonville and Orlando.

Express Drive renter’s insurance coverage depends on which of the following three periods you’re in when an incident occurs:

Personal driving: You’re offline (i.e. not in driver mode)

Waiting for a request: When the app is in driver mode and you have not received a ride request.

Ride in progress: This includes any time from accepting a ride request until the time the ride has ended in the app.

Lyft works with different partners, including Allstate, Atlas, MetLife, Paragon, Travelers, and Zurich, to help with auto insurance claims.

What are the differences between Lyft Express drive claims and other claims?

The biggest difference is that Hertz or Avis provides auto physical damage to the vehicle. In other words, Lyft does not provide auto physical damage coverage. However, Hertz or Avis only provide vehicle coverage while you are personal driving or waiting for a ride request. If a ride is in progress, Lyft provides auto physical damage coverage.

Also, for auto physical damage to the rental, there is a $1,000 deductible. The Lyft driver must pay this deductible. As a comparison, in claims that don’t involve Express drive, Lyft’s auto physical damage deductible is $2,500.

Another difference is that Avis and Hertz has a $50,000 limit on auto physical damage. Lyft does not have a limit.

The other coverage bodily injury and uninsured motorist liability limits are basically the same. I want to be your Lyft accident lawyer if you are injured while driving a Hertz express car.

What happens if a Lyft driver hits a motorcyclist?

If a Lyft driver hits a motorcyclist, the motorcycle rider may have a case. However, the motorcyclist is entitled to compensation for pain and suffering only if the Lyft driver was at fault.

If the Lyft driver did nothing wrong to cause the accident, the motorcycle rider does not have a case. This is true even if he or she hires the best Lyft accident lawyer. In this instance, at best, the motorcyclist can make a claim with his or her insurance company to fix the motorcycle.

If the motorcycle was insured with Medpay coverage, it will pay the rider’s bills. Medpay pays up to the limit as stated on the insurance policy.

Let’s assume that the Lyft driver was at fault in an accident. In this instance, if the Lyft driver was en route to pick up a passenger or during a trip, Lyft has $1 million of bodily injury liability (BIL) coverage. In most cases, this should be enough to pay for the fair settlement value of the motorcycle rider’s personal injury claim.

However, there are times where $1 million may not be enough to cover the motorcycle rider’s injury claim. For example, if the motorcycle rider died, the Lyft driver’s $1 million BIL may not be enough to pay for the value of the claim.

In any serious injury case, you should hire a Lyft accident attorney.

Lyft’s Minnie Van Mode at Walt Disney World

Walt Disney World’s Minnie Van allows users to use their smartphone to request a ride. Disney calls it a relaxing way to get back to your room after a busy day at one of the Walt Disney World theme parks or the Disney Springs area. Walt Disney World says that the Minnie Van Service is a great way to get around Walt Disney World Resort quickly and in comfort—all while in a Disney-owned, Disney-operated vehicle.

Walt Disney World explains How It Works as follows:

Our Minnie Van service works with the Lyft app. Simply open the Lyft app from anywhere within Walt Disney World Resort to access Minnie Van service, request a ride and pay for it through the app—or call (407) 828-3500 to request an accessible vehicle. Cars are usually minutes away.

Open the app and select your Walt Disney World destination

Confirm your pick-up location and tap “Select Minnie Van”; if Minnie Van service is not the default vehicle type displayed, you will need to swipe through your vehicle options until Minnie Van service is displayed

The app will display a map tracking the vehicle en route—along with an identifying vehicle number to help you spot your car

Here is what Lyft says about Minnie Van Mode at Walt Disney World:

The Minnie Van Mode is provided by Walt Disney Parks and Resorts and Resort employees at the Walt Disney World Resort in Orlando, Florida. All Minnie Van ride vehicles are provided and operated exclusively by Walt Disney Parks and Resorts. If you choose to take a ride in the Minnie Van mode you agree that the Minnie Van mode is subject to Walt Disney World Resort policies.

Motorcyclist’s Wife Sues (and Settles) with Lyft Driver for Her Husband’s Death

I created this diagram of an actual Lyft accident. (Not to scale.)

Let’s look at an actual lawsuit where the wife of a Lyft motorcycle rider sued the driver that hit him and Lyft.

But before I tell you what happened, I want to give you a tip:

You need an attorney to sue Lyft in court.

Otherwise, you are asking for major problems. I highly recommend hiring a Lyft accident attorney who has settled at least one case for over $40,000 with Lyft’s insurance company. I have.

OK. Let’s get back to this case. This is not my case. However, to better learn how Lyft handles accident lawsuits, I read the court file. And I created a crash diagram (above). The diagram is not to scale. That said, it gives a general illustration of the accident.

The Lyft accident attorney (for the motorcycle rider’s family) sued in Miami-Dade County state court.

The lawsuit alleged that on October 31, 2015 at 5:43 p.m., a Lyft driver was trying to make a left hand turn from NE 1st Avenue onto NE 36th Street. A motorcyclist was traveling west on NE 36 Street. The lawsuit alleged that the Lyft car and the motorcycle rider crashed.

Sadly, the motorcyclist died at Jackson Memorial Hospital. As is common in most motorcycle accidents, the Lyft driver denied liability.

The motorcyclist was survived by his pregnant wife. About a year and a half after the accident, she settled with Lyft. Like all Lyft lawsuit settlements, court records do not say the settlement amount. The court records say that the settlement paid for the motorcycle rider’s son four year Florida pre-paid college plan. That plan costs about $19,000. Thus, we can assume that the settlement was for at least $19,000.

However, the court order also said that remaining portion of the minor’s settlement shall be used to purchase a structured settlement. Thus, Lyft’s insurance company paid more than $19,000.

In Florida, if a minor gets $15,000 “in his or her pocket” after attorney’s fees, costs and medical bills, the money must be placed in a structured settlement. The minor can’t touch the money until age 18. A structured settlement is an annuity.

Each state has a different law regarding minor child’s settlements. I am a Lyft accident lawyer in Florida. Thus, I only know Florida’s laws.

Articles for Visitors From Another State Who are Injured in Florida Car Accidents

Here are some other articles for out of state victims injured in Florida Lyft accidents.

How Long Do You Have to Sue After a Lyft Accident?

It will depend in the state where the Lyft accident happened. Since I’m a Florida lyft accident lawyer, I’ll talk about Lyft cases in Florida.

In Florida, you have generally have four (4) years to sue a Lyft driver for negligence. This same 4 year time limit applies if a Lyft passenger is suing the the driver of another car.

If you’re making an uninsured motorist (UM) claim with Lyft’s insurance company in Florida, then you have 5 years to sue for UM benefits.

If your family member is killed to a Lyft driver’s (or the other driver’s negligence) negligence, there are essentially two time limits that affect Florida wrongful death cases. The general statute of limitations (time limit) that applies to the majority of wrongful death cases says that a lawsuit for wrongful death must be filed within two years after the cause of action starts. Fla. Stat 95.11(4)(d).

Thus, in most cases, a family member will have 2 years (after the death) to sue a Lyft driver for wrongful death. The same time limit applies for suing a driver of the car for wrongful death.

However, if the decedent dies after expiration of the 4 year time period applicable to negligence and a lawsuit has not been filed before the death, then a wrongful death lawsuit based on negligence is not allowed. Ash v. Stella, 457 So. 2d 1377 (Fla. 1984).

If the decedent dies within the 4 year deadline for negligence, the wrongful death lawsuit against a Lyft driver will be allowed so long as the Lyft accident lawyer files it within the two year deadline that apply to wrongful death lawsuits. Pait v. Ford Motor Co., 515 So. 2d 1278 (Fla. 1987).

Thus, you (or your attorney) need to look at the 4 year deadline that applies to the negligence to see if the death occurred during that applicable time period. If the death happened within that time limit, then the deadline applicable to the wrongful death lawsuit will have to be complied with.

The loss of a loved one is tragic. This is especially true when the death is due to a Lyft accident. However, you don’t want to miss the wrongful death deadline and forever lose your claim. You should also hire a Lyft accident attorney because the settlement value of wrongful death cases is often large. Trying to handle your Lyft wrongful death claim without a lawyer is a poor choice.

You need to hire a Lyft accident lawyer who can properly determine who is at fault. In a big injury case, do not rely on the crash report. That report cannot be used in a Lyft personal injury lawsuit. Florida laws do not allow it.

That said, if the only vehicle involved in the crash was the Lyft car, the passenger can only make a injury liability claim. He or she can’t also make a Lyft uninsured motorist insurance claim.

Let’s assume that there were two vehicles involved in the Lyft wreck. In this scenario, the Lyft passenger often won’t need to pursue both a liability and a UM claim with Lyft. This is because most passenger injury claims are worth under $1 million. Thankfully, most car accident injuries aren’t life altering.

When is a Lyft passenger is most likely to need to make a claim under the Lyft driver’s liability and UM coverage?

In cases of death, or a moderate to severe brain injury, loss of eyesight, paralysis. These are big injury cases. You need an experienced Lyft accident attorney for these claims.

Additionally, if a Lyft passenger suffers a hand or above the knee amputation he or she will likely need to make a claim against the Lyft driver’s liability and UM coverage.

Likewise, if a passenger has a fracture that requires several surgeries (and infection), it may be worth over $1 million. Although not a Lyft case, a woman broke her kneecap (patella) from an accident. Things went downhill from there, fast.

She had a whopping, six surgeries. During the course of these surgeries she had complication and an infection. A judge awarded her $3 million.

Does Lyft’s Insurance Company Pay Better Than Uber’s Insurance Company?

The answer is likely to be Yes in states where Progressive insures Uber, and where Progressive does not insure Lyft.

For example, Progressive insures Uber in Florida. However, Progressive does not insure Lyft in Florida. All things equal, I would prefer a Lyft accident claim than an Uber claim.

I am not making a comment as to how Progressive is as Uber’s insurer. I don’t have an opinion on that. My comment is that Progressive in general is very cheap.

And you won’t find any information on Lyft’s insurance company (Greenwich Insurance Company). If you do, please let me know in the comments below. I would love to hear it.

I would prefer a personal injury claim against almost any major insurer other than Progressive. (And I say this even though as recent as November 2019, I settled a $90,000 injury case with Progressive).

I settled an Uber driver’s accident case for $260,000. However, the at fault driver had big insurance limits. Thus, CNA insurance paid the claim. I didn’t even make an uninsured motorist claim with Progressive.

You can see my video on that $260K settlement here:

How do you make a claim with Lyft’s former insurer, Zurich?

York was (but no longer is) the third party claims administrator (TPA) for Lyft’s insurer, Zurich. York’s info is:

Zurich American Insurance Company C/O York Risk Services Group, Inc. Attn: PIP, BI and/or UM Claims PO BOX 183188 COLUMBUS OH 43218

Claim No.: LYFTXXXXXX

Lyft driver: xxxxxx Claimant: xxxxx

Zurich’s info is below. However, even though Zurich insured Lyft, York handled Zurich’s claims. So don’t use this Zurich info unless York is not responding to you.

Zurich American Insurance Company Attn: Lyft Claims 1400 American Lane Schaumburg, IL 60196-1056

By writing “Attn: Lyft Claims”, this may get your letter to the proper adjuster faster.

York Risk Services Uses Different Digits (in Claim Numbers) to Mark the Type of Coverage

Like many third party claim administrators, York Risk Services assigns a claim number for each accident. York puts a digit at the end of the claim number. I’ve seen York use the last digit of the claim number as a 1 or 3.

Because York will send the injured person letters. The letters may have the York adjusters name. However, the letter or email may not say what type of adjuster he or she is.

By knowing the last digit of the claim number, the injured person will know the type of injury claim. Then, the injured person will know the type of adjuster he or she is dealing with.

There is more:

The injured person may be required to give a statement to a PIP or uninsured motorist adjuster. However, the injured person doesn’t have to give a statement to a Lyft bodily injury liability adjuster.

Bottom Line:

The injured person needs to know the type of York adjuster that he or she is dealing with.

More Info about Lyft’s Old Insurer (Zurich)

Zurich is subject to Florida Insurance Guaranty Association (FIGA). This means that if Zurich becomes insolvent (runs out of money), you still may make a personal injury claim for up to $300,000 with the Florida Insurance Guarantee Association.

Can Lyft’s insurance company use everything that a Lyft passenger says against him/her in a UM insurance claim?

Yes. So use caution with everything that you say or put in writing. Lyft’s insurance company wants to save money. They do so by paying you less. The adjuster is not your friend.

GEICO Rideshare Insurance for Lyft Drivers

GEICO’s Rideshare Policy covers Lyft drivers whether the app is on or off . Lyft driver’s earn $0.25 extra on each eligible Lyft ride that they give. Here is a chart that shows how the GEICO rideshare policy works for Lyft drivers:

Progressive Rideshare Endorsement (Insurance) for Lyft Drivers

Progressive offers a rideshare endorsement for Lyft and Uber drivers. However, if you are transporting a passenger or driver during a rideshare trip, your Progressive rideshare auto policy will not pay for collision damage to your car. This is different than GEICO’s rideshare endorsement.

The good news is that Lyft’s contingent collision coverage will pay for damages to your car. The bad news is that the deductible is a whopping $2,500! Lyft will require a denial of coverage letter from Progressive in order to pay for the damage to your car.

Many Companies Sell Rideshare Insurance in Florida

Several auto insurers are selling rideshare insurance. These include USAA, Foremost Insurance (part of Farmers Insurance), Infinity Insurance, and Great Florida. Those are just a few auto insurers that sell insurance to Lyft drivers in Florida. So, if one of those companies insures the Lyft driver, then they may pay you PIP Benefits.

However, in the Lyft case that I settled, Lyft’s PIP insurance was the primary PIP insurer.

More and more auto insurers will likely start to sell Rideshare insurance to Lyft drivers.

Lyft Accidents that Occurred from May 1, 2019 through March 29, 2020

For car accidents that occurred from May 1, 2019 through March 29, 2020, Lyft made a huge change on its Florida insurance policy. If there are no passengers in the Lyft car, Lyft only has a $20,000 combined single limit (CSL) in uninsured motorist insurance coverage.

The CSL is the most uninsured motorist (UM) coverage that all the passengers and the Lyft driver can recover under Lyft’s insurance policy for one accident.

This is big news. And it’s bad for Lyft drivers (when they don’t have a passenger in the car).