If you were injured in a car accident while performing job duties in Florida, your case likely involves two separate insurance systems:

- Florida Workers’ Compensation

- The at-fault driver’s auto insurance

These systems operate under different laws, rules, and financial incentives.

Insurance companies often try to shift responsibility to each other. When this happens, injured workers can find themselves stuck between insurers arguing about who pays first and who reimburses whom later.

Handled properly, an injured worker may recover compensation from multiple sources. Handled incorrectly, important claims or benefits can be lost.

At JZ Helps, we focus on cases involving the intersection of workers’ compensation and third-party injury claims after Florida work-related car accidents.

Below are several examples of settlements we obtained in these types of cases.

Work-Related Car Accident Settlements

Below are several examples of settlements we obtained in these types of cases.

- $300,000 Settlement: T-bone crash while driving on a work trip in Clearwater.

- $260,000 Settlement: Uber driver was T-boned by a van while transporting a passenger.

- $210,000 Settlement: Truck driver rear ended by another 18 wheeler.

- $125,000 Car Accident Injury Settlement: Police officer T-boned a car that ran a stop sign

- $100,000 Settlement: Driver Rear-Ended While Transporting a Vehicle for Work

- $57,000 Settlement: Police officer was rear ended while on duty.

- $35,000 Settlement: Driver injured when another vehicle ran a stop sign during work hours.

While every case is different, these examples show how compensation may come from both workers’ compensation benefits and claims against negligent drivers.

Table of contents

Who Pays First: Workers’ Comp or Auto Insurance?

In Florida, if you are injured in a car accident while working, Workers’ Compensation is usually the primary payer.

Under Florida Statute §440, workers’ compensation typically pays for:

- medical treatment

- a portion of lost wages (usually 66⅔%)

Your Personal Injury Protection (PIP) and the other driver’s insurance may become relevant later depending on the circumstances of the crash.

Because multiple insurance policies may apply, determining which coverage applies and in what order can become complicated.

Can I Sue the Other Driver if I’m Receiving Workers’ Comp?

Yes. This is known as a “Third-Party Claim.” While Workers’ Comp covers your immediate medical bills and lost wages regardless of fault, it does not pay for pain and suffering.

To get money for pain, suffering, and the full value of your damages, you must file a claim against the negligent driver who caused the crash. This is exactly how we secured the $35,000 settlement mentioned above—by pursuing the driver who ran the stop sign while our client was on the clock.

The “Coming and Going” Rule: Is Your Commute Covered?

Generally, Florida law says that commuting to and from work is not “in the course of employment.” However, there are major exceptions:

- Travel as part of your job: Like our client in the $300,000 Clearwater settlement who was on a work trip.

- Special Errands: If your boss asked you to pick up coffee or supplies on your way in.

- Mobile Offices: If your vehicle is required for your work (like a delivery van or police cruiser).

What is a “Third-Party” Claim in a Work Accident?

A “third-party” claim is a lawsuit against someone other than your employer or co-worker. In many of our settlements, like the $125,000 case where a police officer was T-boned, we pursued the negligent driver who ran the stop sign.

This is vital because while Workers’ Comp pays for doctors, it doesn’t pay for your “pain and suffering.” By filing a third-party claim against the at-fault driver’s insurance, we can seek the additional compensation you deserve for the physical and emotional toll of the accident.

Detailed Case Studies: How We Won These 6 Settlements

Reading about the law is one thing, but seeing how it is applied to real Florida families is another. Below, we have detailed six specific cases where we navigated the ‘priority of pay’ between Workers’ Comp and auto insurance to secure maximum compensation for our clients.

These stories illustrate the strategies we use to overcome insurance company denials and complex liability disputes.

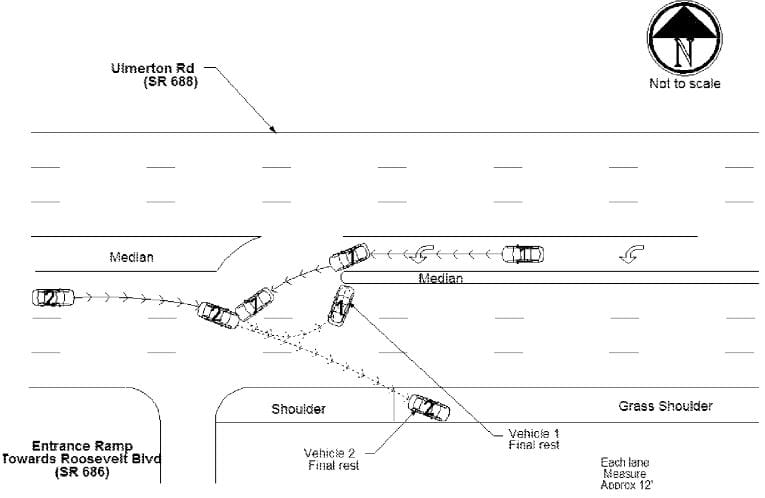

$300,000 Settlement for Businessman T-Boned While Working in Clearwater

Ryan, a Georgia businessman, was in Clearwater for a work trip when the crash occurred.

While driving a rental car between meetings, another driver made a left turn directly in front of him. The driver failed to yield the right of way and was ticketed.

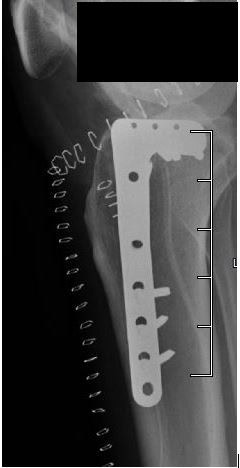

Ryan suffered a tibial plateau fracture in his knee and required surgery with a plate and screws to repair the injury.

While still in the hospital recovering from surgery, Ryan hired me to represent him.

Because Ryan was injured while traveling for work, his claim involved both workers’ compensation and a third-party injury claim.

Workers’ compensation covered his medical treatment and part of his lost wages. However, workers’ comp does not compensate for pain and suffering.

To recover those damages, we pursued a claim against the driver who caused the crash.

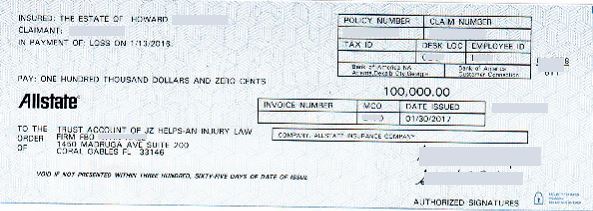

The at-fault driver had $100,000 in liability insurance with Allstate, which paid the full policy limits.

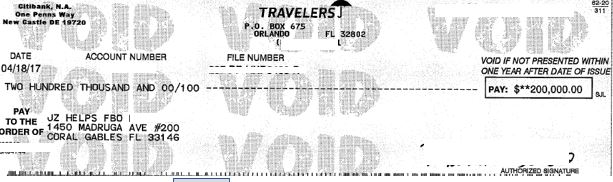

Because Ryan’s injuries were serious, we also pursued a claim under his underinsured motorist (UM) policy with Travelers.

This required filing a lawsuit against both the driver’s estate and the UM insurer.

After presenting medical evidence and negotiating with both insurers, the case settled for $300,000:

- $100,000 from Allstate

- $200,000 from Travelers UM coverage

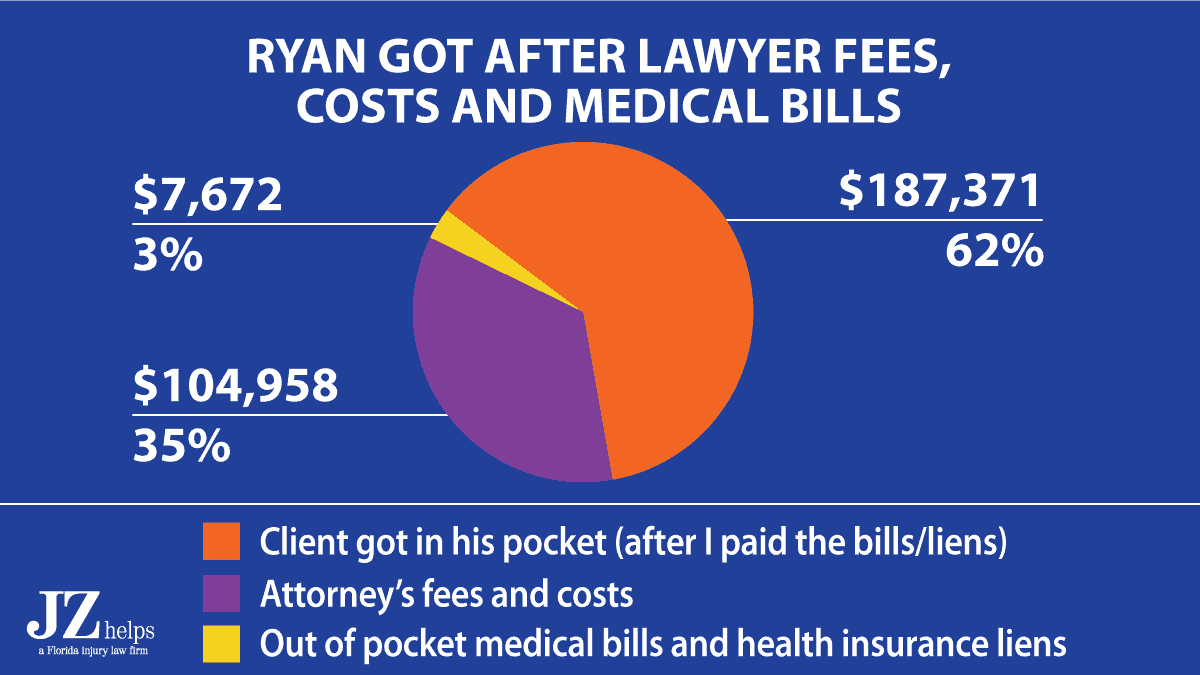

After fees, costs, medical bills, and the workers’ compensation lien were resolved, Ryan received $187,371.

This case shows how an injured worker can recover compensation beyond workers’ compensation benefits by pursuing a third-party claim against the negligent driver and underinsured motorist coverage.

$260,000 Settlement for Uber Driver T-Boned While Transporting Passenger in Miami

Ray was driving for Uber in Miami when the crash occurred.

While traveling straight on the road with a passenger in his vehicle, a van suddenly made a left turn directly in front of him. The vehicles collided.

Because Ray was transporting an Uber passenger at the time of the crash, he was working when the accident happened.

Shortly after the crash, Ray went to the hospital for evaluation.

While there, he contacted my office and hired me to represent him.

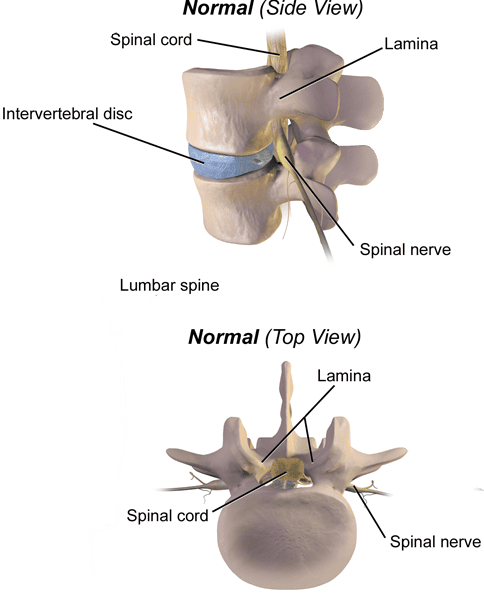

Ray claimed that the accident caused a fracture of the lamina in his spine, as well as disc injuries in his lower back.

Because Ray was working at the time of the crash, the case involved issues common in work-related car accident claims, including a third-party claim against the driver who caused the crash.

The driver of the van was insured by CNA Insurance.

CNA initially offered $150,000 to settle the claim.

After presenting medical evidence and negotiating with the insurer, the case settled for $260,000.

Most of the settlement compensated Ray for pain and suffering related to his spinal injuries.

$100,000 Settlement for Driver Rear-Ended While Transporting a Vehicle for Work

David was behind the wheel of an SUV in Orlando, transporting it for his company, when another driver slammed into him from behind. The force snapped his head back, and for a few seconds everything went black.

By the time paramedics reached him, he was awake and told them the crash had knocked him out briefly.

That kind of damage may look like just another repair bill, but the real story was David’s injury. And the SUV wasn’t the only one torn up that day.

Doctors didn’t find any broken bones, but his pain was real — and soft tissue cases are exactly the kind GEICO loves to minimize.

While he lay in the hospital, he worried: Would GEICO even take his case seriously? Would he be able to keep working to pay his bills?

Adding to the challenge, David already had pre-existing neck and back injuries. With the impact not being huge, GEICO could argue the crash didn’t cause or worsen those injuries.

After the crash, David completed our form for a free consult to see if hiring me made sense. We spoke, and he decided to move forward. (Like David, many people aren’t sure if hiring a lawyer is worth it. That’s why I offer a free consult — so you can find out before making a decision.)

Workers Comp Pays the Hospital Bill

One of the first things I did was connect David with a workers compensation lawyer. Workers comp covered his enormous hospital bill — more than $233,000 — and his lost wages while he recovered. But workers comp has the right to get paid back out of any settlement.

Here’s where having a personal injury lawyer mattered: under Florida law, workers comp had to cut down what they collected to account for my legal fees and costs. And if David’s injury case was worth more than GEICO’s $100,000 policy limit, workers comp would have to reduce their payback even further.

Without a lawyer, David might have owed most workers comp nearly every dollar of his settlement — leaving him with little in his pocket.

Before GEICO even saw that hospital bill, their adjuster tossed out an early offer of just $10,350. That might cover an ER visit in some crashes, but it was nowhere near enough for the injuries and hospital stay David faced. Offers like this are common —GEICO hopes injured people will take quick money before the full extent of their case is clear.

Most injured people, under stress and staring at bills, take that kind of offer. If David had done that, legal fees and medical paybacks would have eaten up most of it — leaving him with almost nothing in his pocket.”

David continued treatment for his neck, back, and head, and wrists. But when it came time to value his case, GEICO’s adjuster brushed off his $233,000 hospital bill as outrageous, insisting the charges were way too high.

On his own, David would have had no leverage to fight back when GEICO dismissed his medical bills. That’s where strategy mattered.

Still, we pushed forward. Just 67 days after the crash, GEICO changed course and offered their full $100,000 policy limits.

Before the check could be finalized, though, we had to confirm whether David had access to additional coverage and whether the other driver had assets or was acting in the course and scope of their job. Only after clearing those issues could the settlement move forward.

Relief at Last

After my fees, costs, and workers comp’s reduced payback, David took home about $54,000. The settlement funds were wired straight into his account 117 days after the crash — no delays, no waiting for checks to clear.

For David, that payment meant more than just numbers on paper. It meant his hospital bills didn’t crush him, his workers comp worries were lifted, and he could finally move forward with relief instead of fear. Cases like David’s show how even when the odds feel stacked against you, the right strategy can turn a difficult claim into a real recovery.

If he’d faced GEICO and workers comp alone, the result could have been a $10,000 lowball — or worse, a settlement eaten up entirely by liens.

Instead, he walked away with $54,000 in his pocket.

Injured in a Car Accident While Working in Florida?

When a crash happens while you are working, the legal situation is often more complicated than a typical car accident claim.

You may be dealing with:

- your employer’s Workers’ Compensation insurance

- the at-fault driver’s auto insurance

- possible uninsured or underinsured motorist coverage

- reimbursement claims from workers’ compensation

Each of these systems operates under different rules, and insurance companies often try to shift responsibility to one another.

Handled properly, an injured worker may be able to recover compensation from multiple sources, including damages for pain and suffering that workers’ compensation does not cover.

The case studies above show how work-related car accident claims can involve both workers’ compensation benefits and third-party injury claims against negligent drivers.

If you were injured in a car accident while performing job duties in Florida, it is important to understand all of the potential claims that may apply to your case.

You can call my office for a free consultation to discuss your situation.