State/County: Florida/Miami-Dade/near Midtown Miami

Settlement Date: March 2014

Claimant’s Attorney: Justin Ziegler

Insurer for At-Fault Car /Liability Claims Adjuster:

GEICO Insurance/Adjuster Denise Araiza

Claimant’s Expert:

Dr. Maury A. Jayson, M.D. (Urologist in Pembroke Pines)

Parties:

Claimant was single 23 year old male, employed as a chef at the time of accident. The adverse car owner had auto insurance with Geico.

Summary:

On May 26, 2013, at 12:40 a.m., our client, a 23 year old, was riding a motorcycle going straight on NE 2nd Ave.

He was in Wynwood, Miami-Dade County, Florida. Wynwood is North of Overtown and Downtown Miami, and South of Little Haiti.

A driver of a car violated our client’s right of way. The car made a left hand turn in front of our client. GEICO insured the driver.

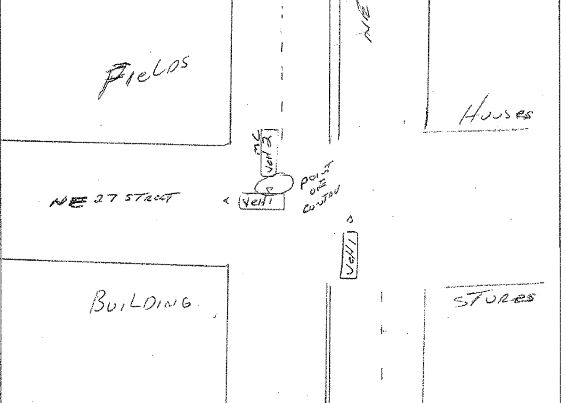

The crash report stated that it the accident occurred at a four-way intersection that was dark-lighted and without any traffic controls.

The car’s turn was so unexpected that the motorcyclist could not stop the motorcycle and struck the car. The car driver received a ticket for careless driving. The crash occurred in Miami-Dade County.

The impact was so hard that the motorcycle was removed by a towing company. The crash report lists $3,000 of damage to the car. Our client took pictures of the damage to the motorcycle.

As you can see from the picture at the top of this page the front tire on the motorcycle partially came off of the rim. Metal was significantly bent on the front rotor.

There were dents to the motorcycle frame on the front seat. There were other dents on motorcycle.

Geico accepted liability and paid the property damage claim for the motorcycle. The crash report diagram is below.

Claimant’s Injuries (Damages):

Six days following the crash, my client received medical treatment at Citimed in Downtown Miami. Citimed is one of the medical providers that I have listed on my map of Plaintiff friendly orthopedic doctors and neurologists.

I recommend if you are injured in an accident caused by someone else.

Our client’s medical bills were about $19,000. He complained of neck, back, knee, flank (area to the side of your “stomach”) and testicle pain. He had an MRI of the lower back which revealed a broad-based lumbar disc herniation at L5-S1 which can be seen below.

Our client did not have health insurance. He treated with a Florida orthopedic doctor that we recommend in Miami.

An MRI of his knee did not find any injury.

Geico submitted the MRI of the knee to an “independent” doctor (radiologist Avinash Balkissoon, M.D.).

The good news for the motorcycle rider’s injury case?

Suprisingly, Dr. Balkissoon said that the MRI of his knee showed a meniscus tear. Specifically, it was a small partial peripheral undersurface posterior horn medial meniscus tear.

Sadly, our client was also diagnosed with erectile dysfunction.

Policy Limits for Bodily Injury Liability Coverage of the car:

$100,000

Settlement Details:

I offered to settle the personal injury case with GEICO for the policy limits of $100,000. The settlement formula that I used is listed below. At this time, I did not know that our client would soon be diagnosed with erectile dysfunction or that he had a possible tear in his meniscus.

In order to calculate the full value of this claim for settlement purposes, we use a formula that applies to all Florida injury cases.

Settlement = Pain and Suffering + Medical Bills + Lost Wages

In Florida, if a driver’s negligence caused your injuries while you’re riding a motorcycle, then you may be entitled to get non-economic damages (damages for pain and suffering), and hopefully money. The same is true for getting damages, and hopefully money, for your medical bills and lost wages.

So to bring this formula to life we are going to substitute a possible settlement value for the pain and suffering component of an unoperated herniated disc.

We will use $50,000, which is the upper end of the range that I use as a starting point when assigning a settlement value for the pain and suffering component of an unoperated herniated disc in a Florida accident. Since our client owed $19,000 in medical bills, we substitute these numbers into the formula.

Possible Settlement value = $50,000 + $19,000 + Lost Wages

Now, we add the pain and suffering and medical bill amounts together.

Possible Settlement value = $69,000 + Lost Wages

Part of the reason that I chose the $50,000 figure for pain and suffering was that our client is a chef and he needs to be able to be standing on his feet for long periods of time. Back pain can make it difficult to stand for long periods of time.

Our client was unable to get his employer to complete a wage and salary verification form that stated his lost wages and time missed from work.

Geico’s First Offer is Only $4,500

GEICO claims adjuster Larry Frederick made an opening offer of $4,500. This is why I say that Geico is just an average insurer when it comes to paying personal injury claims. I think Geico did not make this offer in good faith. In fact, Mr. Frederick described our client’s issues as soft tissue.

I asked him for his top offer, which he told me it was $10,000. He said that I would need to file suit if I thought that my case was worth more than that.

The car owner had “split limit” liability coverage of $100,000/$300,000. This means that one person – in this case my client – can get a maximum amount of $100,000 for his personal injury claim.

So that I could get a better understand of this particular disc herniation, I called to speak with an independent orthopedic doctor – who is often hired by the insurance companies. I gave the brief facts to this orthopedic doctor including the fact that MRI report stated that he has a broad-based disc herniation.

The independent orthopedic doctor told me that most MRI reports – in accident related claims – from the claimant’s radiologist that state that the injury claimant has a broad-based disc herniation usually overstate the disc injury, and it is not true herniation. But he said that he was willing to look at the actual MRI CD to make certain that the finding was incorrect.

So we reviewed the MRI CD and medical records for about 1 hour and a half, in person, and the doctor said that this was definitely a disc herniation.

He said that this was the 1-2 out of 10 situations where the MRI report from the treating radiologist – in an accident case – was correct when stating that the claimant had a broad-based disc herniation.

The independent orthopedic felt that the most important 3 things, in no particular order, in this case were:

1. The MRI – when he read (saw) it – revealed an actual disc herniation.

2. The gentleman with the herniation is young, specifically 23 years old. The doctor said that absent a past medical history of treatment for lower back pain – a 23 year old should not have a herniated disc in his lower back.

This is true even if he played football in high school or engaged in a rough contact sport prior to the accident. He did not play football in high school. I told the doctor that my client does not have a prior history of lower back pain.

3. My client had complaints of lower back pain beginning on the first date of treatment – 6 days after the crash – and continuing through the date of the MRI.

Since this was such an obvious disc herniation, I demanded the policy limits of $100,000 and sent the MRI CD to Geico and asked them to re-read the MRI. They hired a radiologist (Kevin Abrams, MD), who is the medical director of Neuroradiology and MRI at Baptist Hospital.

That is an impressive title, given that Baptist Hospital is the largest hospital network in South Florida. I would assume that Dr. Abrams is pricey. This shows that an insurer, such as Geico, will spend significant money to investigate and defend a claim.

Dr. Abrams confirmed that at L5-S1, there was a moderate– size central /right paramedian disc herniation indenting the thecal sac. This helped my client’s case.

More often than not, a liability insurer will hire a radiologist in a herniated disc case. He or she reviews the MRI of the injured person’s spine.

The defense radiologist will use one of several arguments to deny or minimize the existence, cause or severity of a herniated disc.

GEICO switched adjusters and I spoke with the covering adjuster Peggy Thaggard. Peggy told me that I needed to reduce my demand below $100,000 in order for her to make an offer above $10,000. reduced my demand from $100,000, then she would not offer any amount above $10,000, in part because it was not her file.

She did tell me that Geico had more money to offer. There are many things that may affect the value of an injury case. Peggy’s arguments as to why the claim is worth less than $100,000 were because:

1. My client waited 6 days to get medical treatment.

One typical defense used by a claims adjuster in a personal injury case is that the claimant has gaps in medical treatment. However, in this claim 911 was called so the crash was reported. Police arrived at the scene and issued a citation to the driver of the car. I do not believe that fire rescue arrived at the scene. Adjuster may attempt to minimize your injuries if you were not transported by ambulance to the hospital, or if you did not emergency room treatment.

2. She said that the medical bills of $19,000 were inflated and I would be able to negotiate them down.

3. I think Penny argued that the herniated disc was not impinging on a nerve root or spinal cord.

I told Peggy that she was not acting in good faith by not offering the fair value of the case. She told me that she would not bid against herself.

In Florida, a third-party bad faith claim arises when an insurer fails in good faith to settle a third party’s claim against the insured within policy limits, thus exposing the insured to liability in excess of his or her insurance coverage. Opperman v. Nationwide Mut. Fire Ins. Co., 515 So. 2d 265 (Fla. 5th DCA 1987).

Learn more about Florida injury claims with Nationwide Insurance Company.

After I got off the phone with Peggy, I emailed and faxed a request for insurance assistance letter to the Florida Department of Financial Responsibility. I also copied Geico on that letter via fax and email. In Florida, the insurer – in this case GEICO – is required to respond to this request for insurance assistance.

Upon receipt of that letter, a Florida insurer will have to explain its actions to the Florida Department of Insurance.

That complaint should have and may have triggered a review and a large amount of scrutiny to this claim by Geico upper claims management. My client’s claim was legitimate, so GEICO should have settle the claim rather than get involved with the Department.

If GEICO had made a fair offer, then I would not have sent that letter to the Department. I sent it because my position was correct in that GEICO made a “lowball” offer and refused to increase its offer unless our client decreased his demand.

The goal was to get a more experienced upper level manager who will perform his own evaluation of this claim and tell the current adjuster to settle the claim for the policy limits or offer an amount that GEICO feels is reasonable. Geico then quickly increased its offer to $17,976. I told my client not to accept this amount and he gave me permission to reject it.

Most clear liability claims or claims where liability can be shown even if it is not clear, should be settled before a lawsuit. I believe this was a clear liability claim for several reasons:

- The driver of a car had a stop sign; therefore my client had the right of way.

- My client was in the inner lane heading north and did not have a chance to avoid the impact.

Our client could not afford to see an urologist so we found one who would perform a one time independent medical evaluation on our client for his testicle pain. In his medical record he diagnosed our client with a penile fracture, testicular pain and erectile dysfunction.

I spoke with the urologist on the phone and discussed what he would be willing to state in an affidavit, and he agreed to state the following in an affidavit:

“1. Within a reasonable degree of medical probability, the motorcyclist sustained a penile fracture, with deformity of his penis, scar tissue and erectile dysfunction as a result of the injuries he received in this incident. This will require him to take the medication – Cialis or Viagra – in order to achieve and/or maintain an erection. The duration of taking the Cialis or Viagra is reasonably certain likely be for the remainder of his life.

2. The motorcyclist will have to incur medical expenses in the future for these medications. The best estimate of these future costs is $35 per pill to be taken on demand; or $130-$150 per month if he takes a daily regimen of said medication.

3. Our client will have to incur medical expenses in the future for physician treatment in order to be written a prescription for said medications. He will need to see a physician two to three times a year for a prescription for a refill, and my best estimate of cost per visit is $100.00.

4. Our client does not have any other risk factors that caused his erectile dysfunction. His erectile dysfunction is organic, resulting from his accident and is not psychological.”

We quickly sent this affidavit to GEICO, who then asked me whether we would be interested in pre-suit mediation. We agreed to mediate it. This gave me a chance to finally meet my client in person as we previously only communicated via email and phone. After hard-fought mediation, GEICO finally offered its limits of $100,000.

After the settlement with Geico, I was able to negotiate our client’s medical bills from approximately $19,000 to $9,000, which gave our client a net settlement of more than $56,750 after we were paid our attorney’s fees, expenses and medical bills were paid.

My thoughts:

1. GEICO is an average personal auto insurer when it comes to paying personal injury claims. You may be able to get a better deal with another insurer who has a better reputation for paying claims. If you have an auto insurance company that is worse than Geico, you may want to see if Geico has a better rate.

2. Request the MRI CD from the MRI facility as soon as you learn that there is a positive finding – something abnormal – on the MRI. Then send the MRI CD to a claims adjuster as soon as you get it.

3. Understand that just because a claims adjuster tells you that he or she is making their top offer, do not assume that you will not be able to get more money. Perhaps you have not given the insurer enough information to set the proper reserves, or they have not had enough time to evaluate your claim. Also, insurers often bluff when negotiating.

4. It may be wise to get your client’s doctor to sign an affidavit or write a report that relates the injury to the accident.

5. There are certain situations when underinsured motorist (UM) coverage in an auto insurance policy may pay for your damages if you are injured while on a motorcycle in Florida. Unfortunately, our client was not covered under any such policy, so we could not make a UM claim.

All things equal, most motorcycle cases in Florida having a higher full value than cases where the injured person was in a car, in a truck, walking as a pedestrian or riding a bicycle when the crash happened. This is because in Florida, in order to make a claim for non-economic damages (pain, suffering, etc.) if you’re in a Florida motorcycle accident, you do not need to have a permanent injury.

The trade-off is that you are not entitled to Personal Injury Protection (PIP) coverage when on a motorcycle. So in this claim our client was not covered by PIP.

This claim is one of the many settlements that we have had for someone who was riding a motorcycle and struck by a vehicle. It is also one of my many settlements for back injury or knee pain. A few years ago, we settled a claim for $445,000 for a motorcycle rider who was hit by a truck.

Did someone’s carelessness cause your injury in an accident in Florida, or on a cruise or boat?

See Our Settlements

Check out some of the many Florida injury cases that we have settled, including but not limited to car accidents, truck accidents, slip or trip and falls, motorcycle accidents, drunk driving (DUI) accidents, pedestrian accidents, taxi accidents, bicycle accidents, store or supermarket accidents, cruise ship accidents, dog bites, wrongful death and much more.

We want to represent you!

Our Miami law firm represents people anywhere in Florida if someone’s carelessness caused their injuries in car accidents, truck accidents, slip, trip and falls, motorcycle accidents, bike accidents, drunk driving crashes, pedestrian accidents, cruise ship or boat accidents, store or supermarket accidents, wrongful death, accidents at an apartment complex, condo building or home, accidents involving a Uber or Lyft Driver, and many other types of accidents.

We want to represent you if you were hurt in an accident in Florida, on a cruise ship or boat. If you live in Florida but were injured in another state we may also be able to represent you.

Call Us Now!

Call us now at (888) 594-3577 to find out for FREE if we can represent you. We answer calls 24 hours a day, 7 days a week, 365 days a year.

No Fees or Costs if We Do Not Get You Money

We speak Spanish. We invite you to learn more about us.