Medical Payments is a coverage that is listed in a Commercial General Liability (CGL) Insurance Policy. Most businesses have a CGL insurance policy.

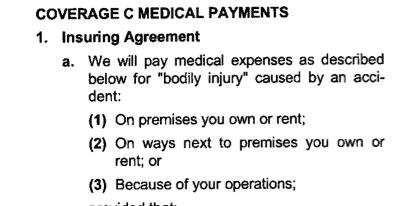

Medical Payments coverage pays emergency medical expenses for bodily injury to you if you were hurt on someone else’s property. Medical Payments coverage is also called Medpay. As you can see from the image above, Medpay is coverage “C” on a CGL insurance policy.

If you are an insured or are an employee of the company, it may or will not cover you and you should look into the workers compensation coverage.

Medical Payments coverage pays for your medical expenses regardless of who is at fault.

You do not have to prove that someone’s negligence (carelessness) caused your accident in order to get your medical bills paid from the Medical Payments portion of a CGL policy.

Looking for Medical Payments coverage is one of the things that you should do if you slip and fall at a store or business. Medical payments coverage will not pay for your lost wages or pain and suffering. (On the other hand, Bodily Injury Liability coverage pays for pain and suffering. Bodily Injury Liability is Coverage A in a CGL insurance policy.)

If you want to get your lost wages paid, read these 4 tips for getting paid for missing work after an accident. You can get money for pain and suffering in a slip, trip or fall or other injury on the premises of another if you can prove that they caused your accident.

Some companies do not have Medical Payments coverage – or the amount is limited. Therefore, you must know what to do after you receive a medical bill from your accident at a store, mall, hotel or other premises.

When Won’t Medpay Pay for Your Medical Bills?

There are times when “Medical Payments” will not pay for your medical expenses such as:

- If you are an “insured” or for anyone hired to do work for the insured

- To anyone entitled to benefits under a workers compensation or disability benefits law

- To any athletic participants

- For anything excluded under the Bodily Injury Liability portion of the CGL insurance policy.

Companies with locations in Florida that most likely do not have Medical Payments coverage:

- Apple Stores

- Carnival Cruise Lines

- Chevron gas stations (corporate owned)

- Costco Wholesale

- CVS pharmacy stores

- Epcot

- Publix Supermarkets

- Royal Caribbean Cruises

- Sedanos Supermarket

- See’s Candies Chocolate Shops

- Target Stores

- Texaco gas stations (corporate owned)

- Walgreens

- Walmart Stores

- Walt Disney World

- Winn Dixie

You should note that the insurance policies for the above companies may changed since the last time that I dealt with the above companies.

Which Businesses Might Have Medpay Insurance?

I have seen the following type of companies, all which were franchisees or small privately owned non-franchised businesses, provide Medical Payments coverage:

- Chevron gas stations (franchisee owned)

- Denny’s restaurant

- Exxon and Mobil gas stations (All stations are franchisees)

- Hyatt hotel

- Property Owners who lease space to a restaurant

- Restaurants

- Day Spas, salons and barber shops

- Taverna Opa restaurant

- Texaco gas stations (franchisee owned)

- W hotel in Fort Lauderdale, Florida

Generally small businesses are more likely to have Medical Payments coverage than large “big box” stores. Let me give an example of how Medical Payments coverage may apply.

How Medpay Works if You Get Injured (at a Restaurant)

Assume you are injured when you fall from a booth that was loose at a restaurant. You fracture your wrist and go to the hospital.

An ambulance arrived at the scene but you decided that you did not want to be transported. Later that night you went to the hospital because the pain in your wrist is bad.

You receive hospital bills that are over $1,200. The restaurant is aware of your incident because the paramedics came into the restaurant to examine you.

Assume Denny’s is insured with Travelers Insurance Company and has a $1,000 medical expense limit under its Medical Payments coverage portion of its CGL insurance policy.

If you set up a claim with Travelers Insurance Company and send them the hospital bill, they will pay the hospital up to $1,000. This is true even if Travelers does not believe that you will be able to prove that the restaurant’s negligence caused your injuries.

If you have already paid the hospital bill, Travelers Insurance Company will reimburse (pay) you $1,000.

If your health insurance has already paid the hospital bill, and you settle your personal injury case against the restaurant, you may be legally required to pay the health insurance company back for bills that they paid which were related to the accident.

If you had health insurance, you may be able to use the medical payments coverage to pay your health insurance company’s lien if they have a lien, but you should wait to the end of your personal injury case before paying this lien off.

Is There a Time Limit for Making a Medpay Claim?

Yes. As an example, let’s use a CGL insurance policy for a Marriott Hotel in Pensacola, Florida. My client slipped and fell while using the bathtub. She broke her arm. Days later, she had surgery to fix her arm.

The Travelers Property and Casualty Company of America insured the hotel. In short, the name of the company is Travelers. I requested that Travelers send me the insurance policy. They did so.

The Medical Payments section of the policy said that Travelers will pay for medical expenses for “bodily injury” caused by an accident provided that:

the expenses are incurred and reported to us within one year of the date of the accident.

Therefore, in that case, the expenses must be incurred within one year. Additionally, the injured person (or her attorney) needed to report the expenses to Travelers within one year of the accident.

If the injured person waits too long to send the expenses to the CGL insurer, they might not pay the expenses.

That Travelers policy gave the injured person 1 year to submit the expenses. However, perhaps the time period could be shorter. I would think that “cheaper” insurance companies are more likely to have a shorter time frame.

That’s one reason that it’s important to quickly get the insurance company’s policy. Don’t just settle for the insurance company’s disclosure of its insureds’ policy limits.

Can the Medpay Time limit Be extended?

In Florida, the time limit to make a Medpay claim with the CGL insurer may be extended in certain circumstances. But don’t rely on an extension! That’s a huge mistake.

Like most things in life, the best practice is not to delay. The best practice is to get your medical records and bills to the Medpay insurer fast.

When can the Medpay time limit to be extended?

This may occur if you send a written request, pursuant to Florida Statute 627.4137, for insurance disclosure information from the insured or the CGL insurer and they fail to produce a certified copy of the policy.

Coverage defense rejected for failure to provide copy of the insurance policy

Below is an example of when a Florida you may get an extension to the time limitation to submit bills/records to the Medpay insurer. Although the example deals with uninsured motorist (UM) benefits and not Medpay, the reasoning is the same.

Jeanne Rousseau was injured while riding as a passenger in a motor vehicle involved in an automobile accident. Her Gainesville attorney filed a lawsuit for uninsured motorist (UM) benefits against United Automobile Insurance Company (UAIC), who was the insurer for the owner of the motor vehicle in which she was a passenger.

UAIC argued that she was not entitled to UM benefits because she failed to prove compliance with conditions precedent in the UAIC insurance policy. She, as an omnibus insured, did not have a copy of the UAIC insurance policy.

She through her attorney, repeatedly requested a copy of the policy and that UAIC failed to provide a copy of the policy. The insurer failed to comply with subsection 627.4137(1)(e), Florida Statutes, which requires that an insurer “shall provide” a copy of the policy “within 30 days of the written request of the claimant.” Cf. Allstate Ins. Co. v. Singletary, 540 So.2d 938 (Fla. 2d DCA 1989).

The trial court refused to dismiss the case for the passenger’s failure to comply with conditions precedent. The passenger was awarded attorney’s fees pursuant to Florida Statute 627.428 because the insurer’s sole argument relates to a coverage issue.

The coverage issue is that the insurer’s sole argument that the passenger was not entitled to UM coverage as a result of her alleged failure to comply with conditions precedent in the insurance policy. See State Farm Mut. Auto. Ins. Co. v. Lynch, 661 So.2d 1227, 1230 (Fla. 3d DCA 1995).

Tip: Attorneys normally should not charge an attorney’s fee on recovering Medpay benefits. However, if the attorney has to sue to get Medpay, he is allowed to charge attorney’s fees.

Coverage defense rejected for failure to give copy of policy

In the case of Figueroa v. U.S. Sec. Ins. Co., 664 So.2d 1130 (Fla. 3d DCA 1995), the trial court granted judgment based on insurer’s, U.S. Security Insurance Company, defense that insureds failed to provide timely a sworn statement.

U.S. Security is now known as Mendota Insurance. This is a Miami-Dade County case.

The appeals court said that although the failure to submit a sworn statement constitutes a material breach of the policy, Stringer v. Fireman’s Fund Ins. Co.,622 So.2d 145 (Fla. 3d DCA), review denied, 630 So.2d 1101 (Fla. 1993), under the facts and circumstances of this case.

They reversed the summary judgment.

Here, the insurer, who admitted coverage, failed to comply with insureds’ requests for a copy of the policy, and insureds agreed to give sworn statements after receiving a copy of the policy which set forth the obligation to give a sworn statement. See Crown Life Ins. Co. v. McBride, 517 So.2d 660, 661 (Fla. 1987);Allstate Ins. Co. v. Singletary, 540 So.2d 938 (Fla. 2d DCA 1989); § 627.4137, Fla. Stat. (1993). Cf. Goldman v. State Farm Fire Gen. Ins. Co., 660 So.2d 300, 305 (Fla. 4th DCA 1995) (compliance two years after loss “satisfies neither the spirit nor intent of the policy conditions at issue.”).

The insurer lost its coverage defense for failing to give the insured a copy of the policy.

Tip: The claimant should agree in writing to comply with any legal requirements in the policy after receiving a copy of the sworn policy which sets for the obligation. The injured person will look good in front of the judge for offering to be reasonable.

Did someone’s carelessness cause your injury in Florida?

We want to represent you!

Our Miami law firm represents people anywhere in Florida if someone’s carelessness caused their injuries in slip, trip and falls, drunk driving crashes, cruise ship or boat accidents, accidents at an apartment complex, condo building or home, wrongful death and many other types of accidents.

We want to represent you if you were hurt in an accident in Florida, on a cruise ship or boat. If you live in Florida but were injured in another state we may also be able to represent you.

Call Us Now!

Call us now at (888) 594-3577 to find out for FREE if we can represent you. We answer calls 24 hours a day, 7 days a week, 365 days a year.

No Fees or Costs if We Do Not Get You Money

We speak Spanish. We invite you to learn more about us.

Editor’s Note: This post was originally published in 2013 and has been completely revamped and updated.