The tips apply to all cases where you’re dealing with an insurance adjuster. I’ve used and use these tips in my personal injury cases, when appropriate.

These tips can be used in a personal injury claim with Uber, GEICO, Progressive and many other companies.

Here is a video with some of the best negotiation tips on dealing with insurance claim adjusters:

1. Don’t be Intimidated

Adjusters have different personalities. Some adjusters are more assertive than others. If you are dealing with an aggressive adjuster, remain calm and have some faith.

Let me give you an example.

Ryan was driving in Clearwater, Florida when an oncoming car made a left hand turn and hit him. Ryan hired me to represent him in his personal injury claims. Allstate, the at fault driver’s insurance company, paid its $100,000 bodily injury liability limits.

Fortunately, Ryan had uninsured motorist coverage with Travelers Insurance Company. Travelers assigned a sweet adjuster, Darlene, to the claim. However, Darlene didn’t make an offer.

I expressed my frustration that Darlene didn’t make an offer. She then offered $150,000 to settle.

Ryan’s uninsured motorist insurance policy from another state (Georgia) required him to sue the at fault driver. Thus, I could not settle his case with Allstate.

I sued both the at fault driver and the uninsured motorist insurance company. I then got a call from the new Travelers claims adjuster. She told me:

I’m a new adjuster. You know what this means. I am going to reevaluate the case.

She said it in a condescending tone. I assume that she was implying that she was going to review the case and possibly reduce the settlement offer.

She didn’t say it as if she was going to increase her offer.

Now:

That’s not something that an attorney (or injured client) wants to hear. My response to her was that when she revaluates the case she should make a higher offer.

We eventually settled for $200,000. Ultimately, her comment was a negotiation tactic where she was trying to instill fear in me. It did not work.

2. Accept that the Adjuster May Have Limited Decision Making Authority

You never know what goes on behind the scenes at the responsible party’s insurance company. For example, let’s say that you slip and fall at a supermarket in Florida.

You claim that water on the floor that caused you to slip and fall.

As a result of the fall, you have surgery to repair a pre-existing wound that re-opened from the fall. You hire a lawyer who tries to settle your personal injury claim with the supermarket’s claims company.

However, the claims adjuster sends you a letter denying liability and offering nothing. This requires your lawyer to either sue or drop the case.

There is a chance that the adjuster asked their supervisor (or client) to give them authority (money) to settle your case, but it was rejected. In other words, sometimes the adjuster has limited settlement authority.

I settled a case for $300,000 like the one I just described. But only after I sued and took multiple depositions (testimony under oath).

3. Don’t Be Insulted by the First Offer

In personal injury cases, insurance companies often make a low first offer. Whether you like it or not, it’s part of the process.

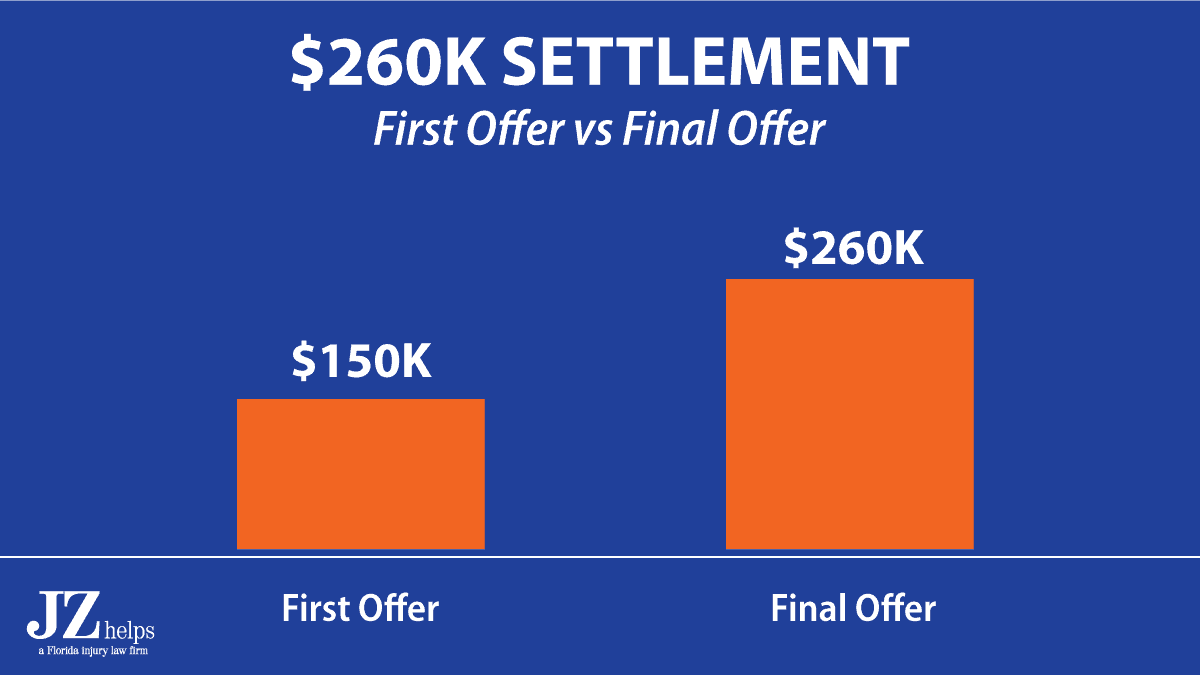

For example, I represented an Uber driver who was involved in a car accident. An oncoming van made a left turn and the Uber driver crashed into him.

The van’s insurance company (CNA) offered $150,000 to settle. Rather than getting offended at CNA’s first offer, we negotiated and eventually settled for $260,000.

Here is a comparison between the first offer and the settlement:

Instead of getting bothered by a low first offer, ask yourself:

Have I given the adjuster all the evidence that helps my case?

It’s a better use of your time to spend work on building your claim instead of being mad at the adjuster for their low offer.

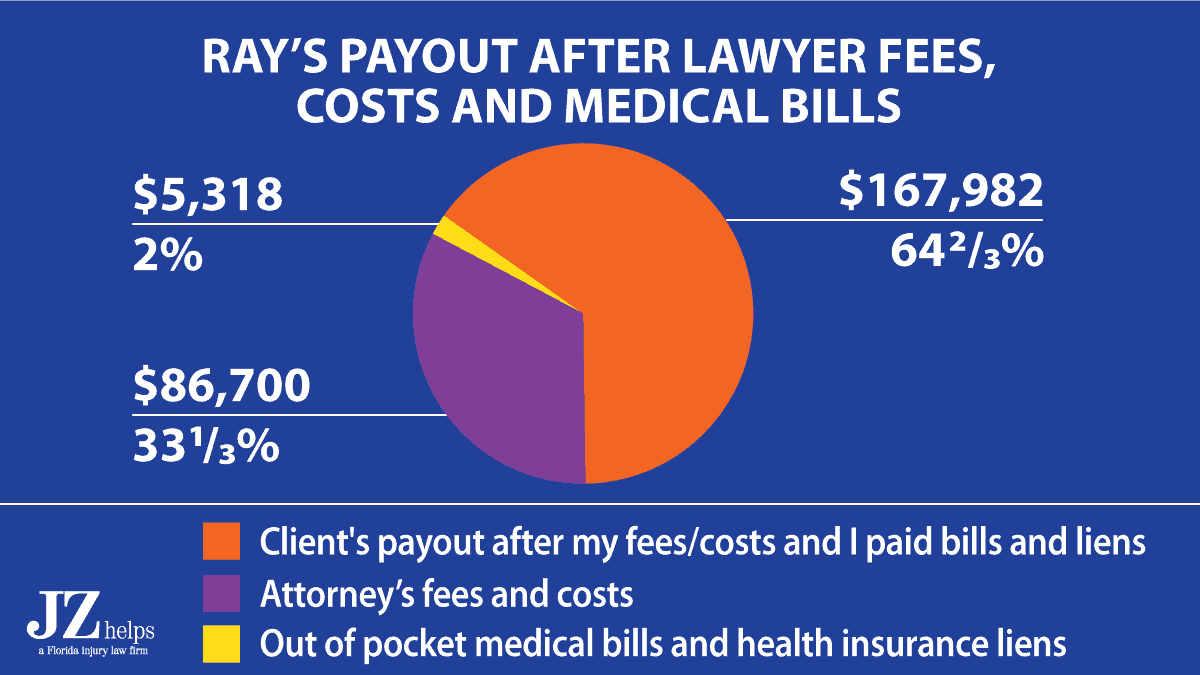

You can see how much the Uber driver got in his pocket after my lawyer fees, costs and paying back his medical bills and Medicaid.

His payout above does not include the interest on a loan that he took.

4. Don’t Believe What The Adjuster Says

No matter how much you like the adjuster who is handling your claim, do not believe him or her. You and him/her have opposite interests.

The less money the insurance company pays you, the less money you get.

Let me give you an example of why you should not believe the insurance adjuster.

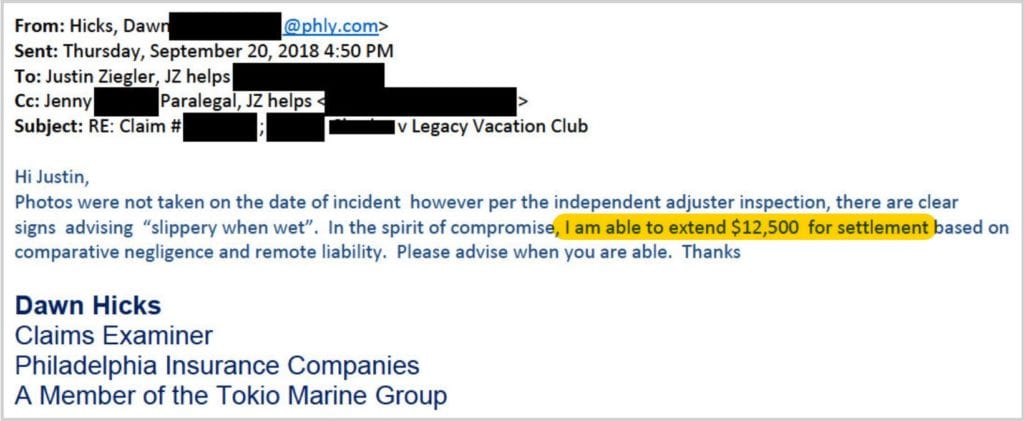

Angela slipped and fell in a bathtub at a hotel near Orlando, Florida. As a result of her fall, she broke her arm.

Philadelphia Insurance Company insured the hotel. The adjuster’s first offer was for $12,500. In her email to me, she said that she was making this offer based on comparative negligence (my client’s fault) and remote liability.

Basically, she said that the hotel wasn’t at fault and my client was at fault.

After representing people injured in accidents for 17 years, I knew not to believe her. Even though she was not rude to me.

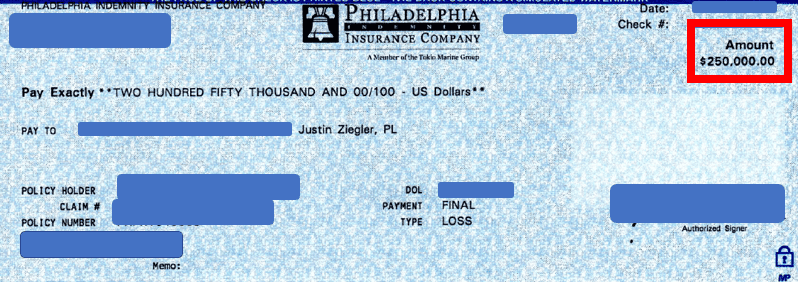

Can you guess what happened several months later?

I settled Angela’s personal injury claim for $250,000. Here is the settlement check:

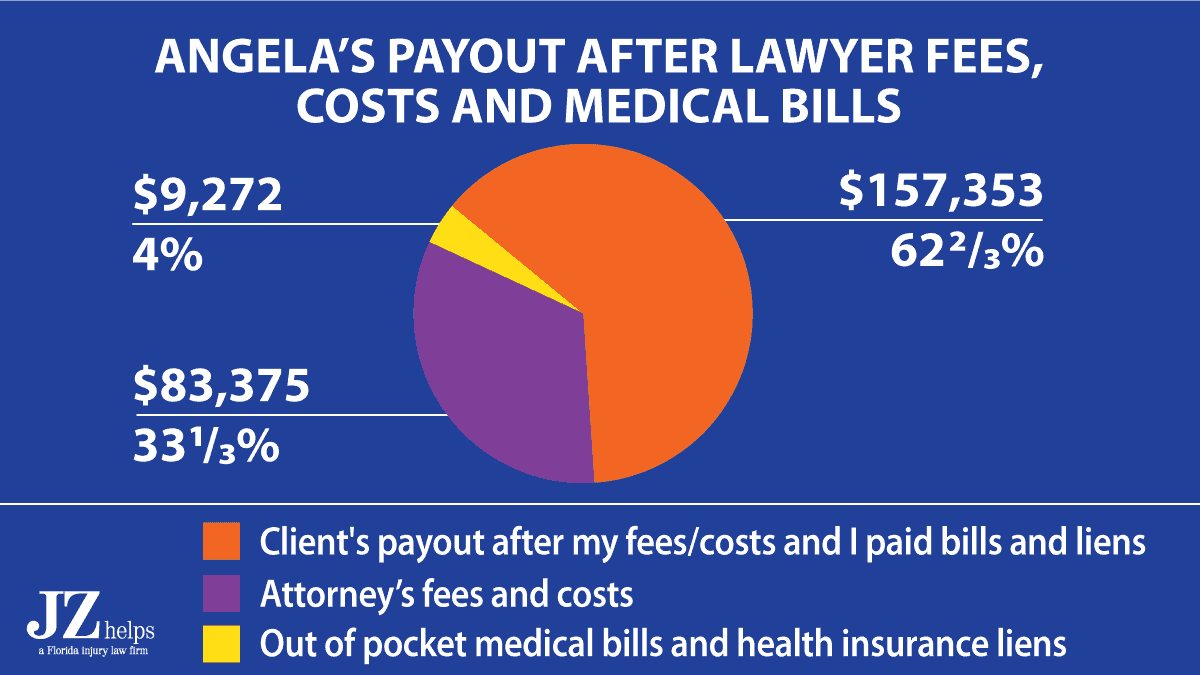

You can see how much Angela got in her pocket:

Insurance adjusters have a duty to act in good faith toward their insureds. However, personal injury claims involve negotiation.

The fair settlement value of every personal injury case is a range. It’s not one exact number.

The adjuster wants to have a good career with their employer. Ultimately, their loyalty to their employer is number one.

If they can save their company money, they will. Saving their company money means paying you less.

Adjuster Says Case Worth $100K (Pays $445K Months Later)

I had a case where the adjuster told me that he had reserved (set aside) $100,000 to pay my client’s claim. We settled months later for $445,000. Don’t believe what they tell you.

5. Don’t Expect the Adjuster to Help You Find More Insurance

It is your job to locate all the available insurance that may pay for your personal injury claim. Don’t expect the insurance adjuster to help you find additional insurance money. Often times, they won’t.

Let me give you an example.

Mary (not real name) was driving her car through an intersection. Another driver ran ran a red light. Mary t-boned her.

An ambulance took Mary to the hospital. As a result of the accident, Mary broke her wrist. A doctor put a plate and screws into her wrist.

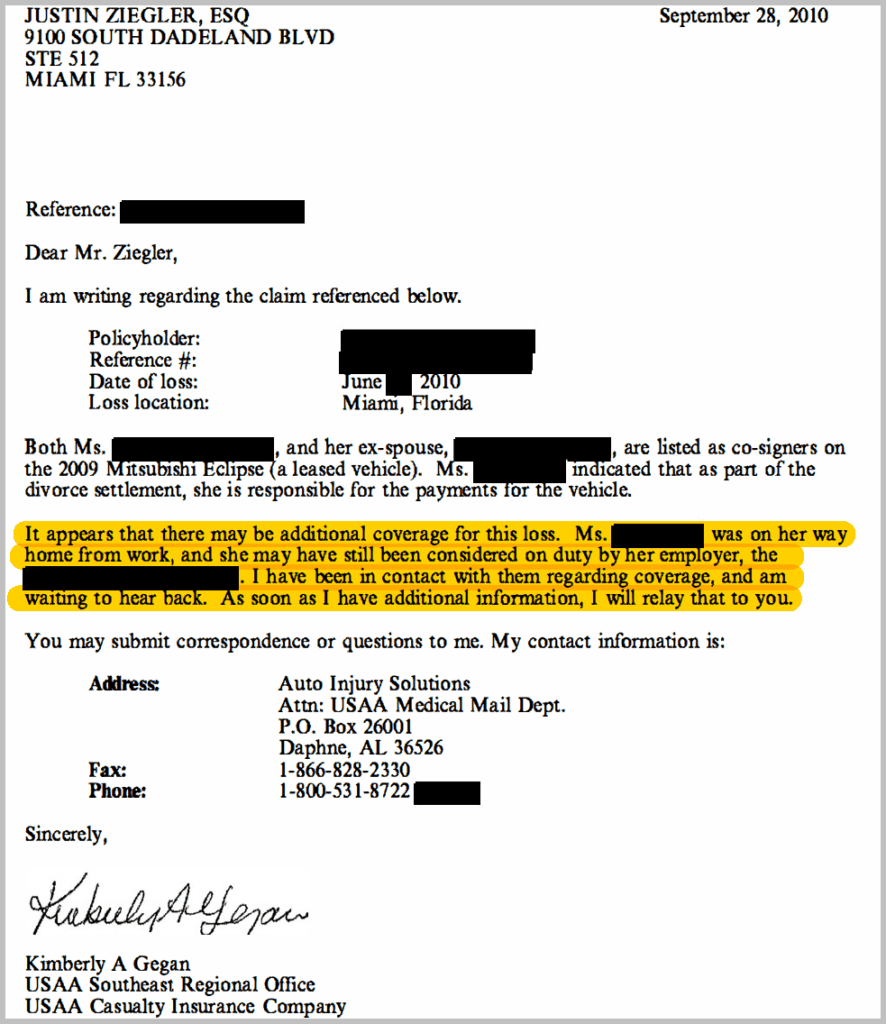

Mary got a free consultation with me and hired me. USAA insured the at fault driver with $100,000 in bodily injury coverage.

USAA told us that it was only aware of its $100,000 bodily injury (BI) insurance policy.

Now:

I did not just rely on what USAA told me.

I asked the at fault driver to complete a financial affidavit that also asked them if she was working at the time of the accident.

It was only then that USAA told me that the at fault driver was working at the time of the accident.

Fortunately, her employer insured her with a $1 million insurance policy.

Within four months of the accident, USAA offered me the $100,000 to settle.

In addition, Old Dominion paid $100K to settle. The total settlement was for $200,000.

If I would have a never pressed the driver to complete an form under oath stating whether she was working, my client would have missed out on an extra $100,000 in insurance money.

That’s a whole lot of money!

6. Ask the Adjuster to Preserve Evidence

Evidence can make or break a personal injury case. Whether it is the vehicle’s event data recorder (black box), or a raised surface that caused your trip and fall, you want to preserve the evidence.

As soon as possible, you should send the responsible party a letter asking them to preserve all evidence. In addition, send a copy of that letter to the adjuster. It shows them that you mean business and that you are serious about your case.

Be sure to get written confirmation that the letter was received. Certified mail is one example of written confirmation.

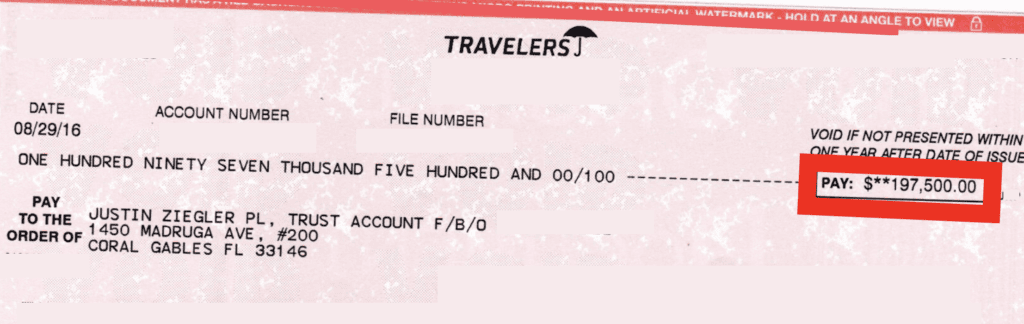

In one case, my client slipped and fell in a hotel bathtub. After my client hired me, I quickly sent a letter to the hotel asking it to preserve the entire bathtub. I sent a copy of that letter to the adjuster.

Later, I sent an expert to take measurements of the tub.

Ultimately, we settled the case for $197,500.

7. Ask the Adjuster to Explain Anything that You Don’t Understand

If the adjuster uses a phrase that you understand, ask him or her to clarify. For example, I’m going to use the facts from one of my settlements.

Tiffany claimed that she tripped and fell on some caution tape that you was hanging from one barricade to something else. After several demands and counter offers, the insurance adjuster makes you an offer of $100,000.

We’ll assume that your last demand was for a lot more than that amount. The adjuster tells you that he has:

a “couple more bucks to offer if that would settle the case.

You ask yourself, “What does “a couple of bucks” mean?”

Does it mean two dollars, two thousand dollars, or more.

I don’t know. And you probably don’t know either. Only the adjuster knows.

The solution?

Just ask the adjuster what he means when he says a couple of bucks. I took the above facts from one of my trip and fall cases except it was the defense lawyer who told me he had “a couple of more bucks”.

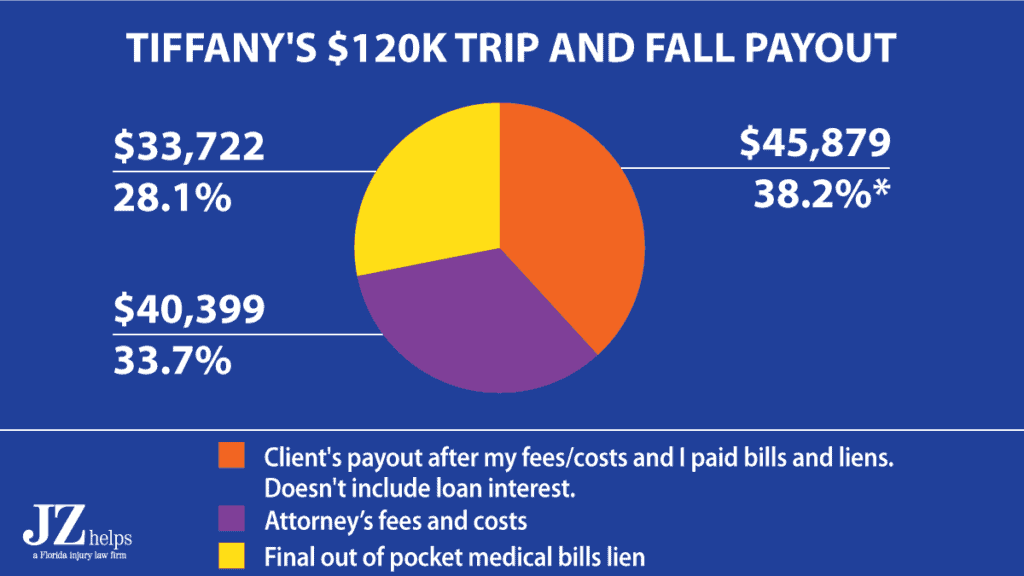

It turned out that a couple of more bucks was an extra $20,000. So we settled my client’s case for $120,000.

In this case, my client (Tiffany) got about $45,879 in her pocket after my lawyer fees, costs and paying back her medical bills.

This figure doesn’t include the interest on a loan that she took and was used to pay for her foot surgery.

The same is true if the adjuster says that he values the case to be in the “low five figures”. Ask him or her what that means. Get the adjuster to commit to an exact amount or range.

7a. Accept Pre-Suit Mediation if Offered

If the adjuster accepts pre-suit mediation, you should accept the offer. This assumes that you have completed (or will soon complete) your medical treatment.

You don’t have to say a word at mediation. You can just let the adjuster make their offer. It’s always a nice feeling to get an offer on the table.

That said, I know there are some attorneys who won’t agree to pre-suit mediation against particular defendants (like certain supermarkets and stores). These plaintiff’s attorneys think that pre-suit mediation is a waste of time. They prefer just suing.

7b. Give Them Time Deadlines To Respond

When you give an insurance adjuster a deadline to respond to you, they usually put it in their calendar. This gives them a reminder when the deadline approaches.

This is particularly true for your settlement demand. If you don’t give them a deadline, your file may just sit on their desk.

8. Answer Their Calls and Respond to Them Quickly

If you answer an adjusters calls, you may have a better chance of getting what you need done quicker.

If you don’t answer their call, you may wind up playing phone tag which may delay your settlement.

9. Speak With a Supervisor if Necessary

Sometimes you need to speak with an adjuster’s supervisor to get more money in the case. I’ve spoken to supervisors many times in my career.

Many times, speaking with a supervisor has helped me get thousands of more dollars in a case. On the other hand, I remember speaking with a supervisor and it only got me an extra $250 in a car accident injury case.

10. File a Consumer Complaint or Civil Remedy Notice if You Need To

11. Listen to What the Adjuster Says

When a claims adjuster is talking to you, actively listen. Don’t interrupt them.

Awkward silence is OK. It’s OK if there is silence on the phone for up to a minute. Sometimes this silence will get them to talk and give you a nugget that will lead to you getting a higher settlement.

You generally want to let the adjuster do more of the talking than you on any phone call.

12. Be Nice…But Be Tough

Tip #1 when dealing with insurance claim adjusters is to be nice. Now, don’t mistake being nice for not being tough and assertive.

However, at the end of the case, the insurance claims adjuster is going to be the one who is “writing” you a settlement check. Thus, you want to be nice and have a good relationship with the adjuster.

After all, insurance adjusters are people just like you. They have families. They are just trying to pay their bills.

That said, you want to be nice to them so that when they think about reaching out to you and giving you a phone call, they are in a good mood. You don’t want them to be thinking, “Ugh…I have to deal with this claimant again.”

I’ve heard insurance adjusters say that sometimes they pay a little bit more money to someone who’s nice to them. Likewise, I’ve heard insurance defense attorneys say the same.

13. Organize Your File…and Take Notes

You should organize all documents in your case. You need to be sure that you have every document that can help prove your case.

Use a computerized spreadsheet – such as MS Excel – so that any bills that you have can be edited quickly.

You want to show the adjuster that you’re organized, and that you’re not sloppy.

Every time that the adjuster calls you, he/she is taking notes that will permanently be in the insurance company’s file.

14. Review Your File Before You Call the Adjuster

Before you call an insurance adjuster, you should know the facts of your claim perfectly. Before an insurance adjuster calls you, they’ve reviewed their file and are prepared.

Do the same so that you’re on equal footing.

15. Give the Adjuster Documentation to Help Him