Notification of PIP Benefits Doesn’t Explain Limited Right to Sue

That article does not explain the limited exception from liability for injuries caused to others in an automobile accident.

It doesn’t explain how a careless party can sometimes be exempt from liability for injuries caused to others. Here, I discuss a huge amount of info that you need to know about getting your medical bills paid after a Florida auto accident.

Personal Injury Protection (PIP) or No-Fault Coverage

Personal Injury Protection (PIP) is also known as No-Fault Coverage. It is found in Section 2 of many Florida family automobile insurance policies.

PIP Applies Regardless of Fault

If you are covered by PIP, it pays benefits regardless of whether you are at fault. Even if you were at fault (or received a ticket for a moving violation) for causing the auto accident, PIP will still pay your medical bills.

What Are The Minimum Limits for PIP?

If you were hurt in a motor vehicle accident and you’re covered by Florida PIP, then the minimum limits for no-fault personal injury protection benefits are:

$10,000 for Medical Bills

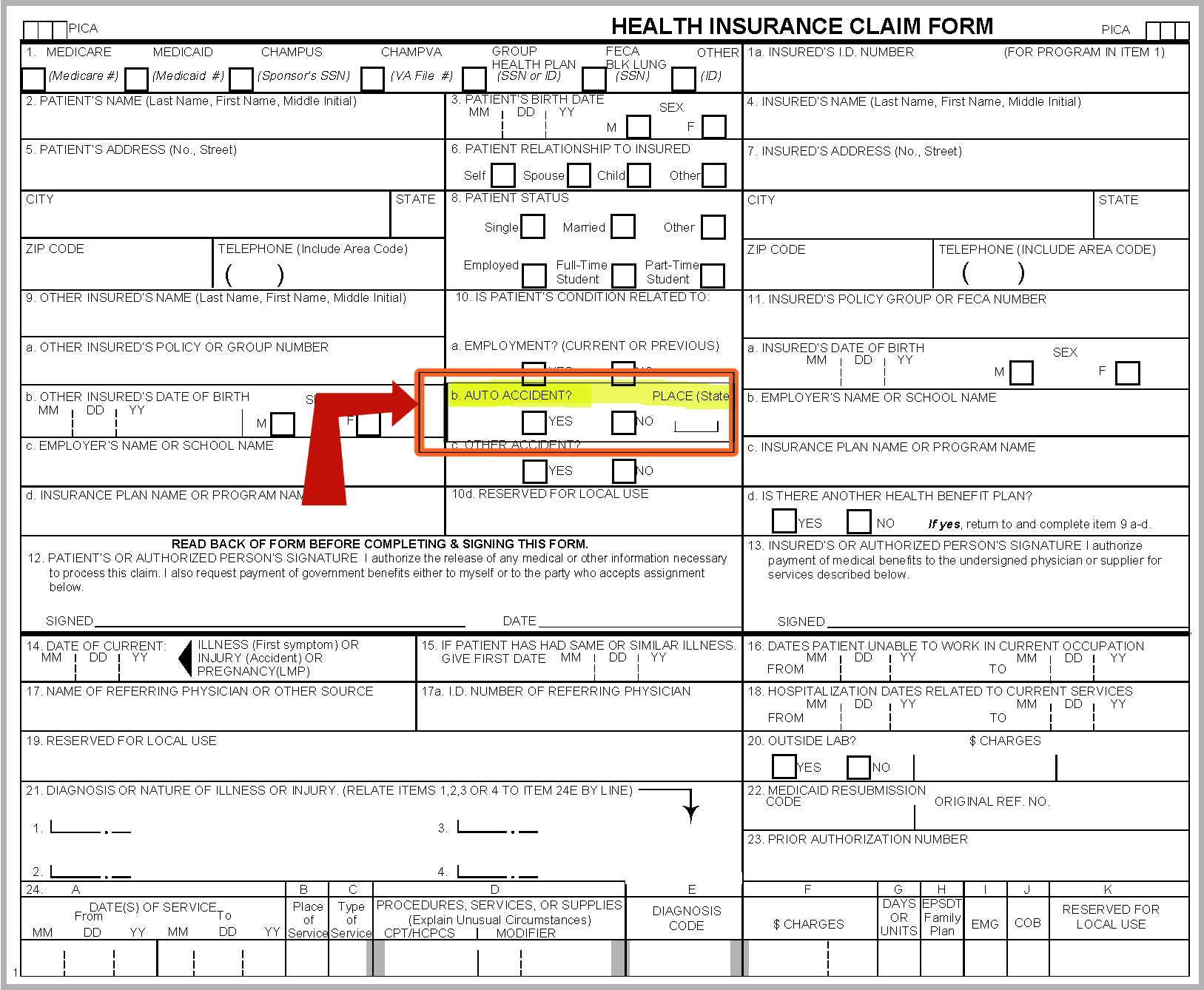

a. $10,000 per person for loss resulting from bodily injury, sickness, or disease arising out of the ownership, maintenance, or use of a motor vehicle if a physician, dentist, physician assistant, or advanced registered nurse practitioner has determined that the injured person had an emergency medical condition,

$2,500 for Medical Bills if You Don’t Have an “Emergency Medical Condition”

b. $2,500 per person for loss resulting from bodily injury, sickness, or disease arising out of the ownership, maintenance, or use of a motor vehicle if a physician, dentist, chiropractic physician, physician assistant, advanced registered nurse practitioner, physical therapist or person licensed to provide emergency transportation and treatment has determined that the injured person did not have an emergency medical condition,

PIP Pays for Lost Wages (Up to $10K)

ACTOR.

c. Disability benefits, which combined with medical benefits cannot exceed $10,000; and

One group of people who often don’t own a car that will provide PIP is foreigners. However, tourists from other countries who are injured in Florida are in luck.

80 percent of all reasonable expenses for medically necessary medical, surgical, X-ray, dental, and rehabilitative services, including prosthetic devices and medically necessary ambulance, hospital and nursing services.

PIP Only Pays Bills if You Get Care Within 14 Days of Car Accident

Medical benefits do not include massage or acupuncture, regardless of the person, entity, or licensee providing massage or acupuncture and a licensed massage therapist or licensed acupuncturist may not be reimbursed for medical benefits.

If No Emergency Medical Condition, PIP Only Pays $2,500

If you are not diagnosed with an emergency medical condition, your PIP insurance will pay up to $2,500 of your medical bills.

What is the Formula to Determine How Much PIP Pays?

The formula to determine how much PIP pays is:

PIP Pays = 80% x total bill

Here is a basic example.

Example – $5K bill (And You Have an Emergency Medical Condition)

You’re driving a car and a careless driver hits you. Your hospital bill is $5,000.00. State Farm insures your car.

If the hospital states that you have an emergency medical condition, State Farm will pay the hospital $4,000. You would then owe the hospital $1,000.

I got this amount by using the formula that I just mentioned.

You also have a claim for bodily injury, any resulting pain and suffering, disability and physical impairment, disfigurement, mental anguish, inconvenience or loss of capacity for the enjoyment of life experienced in the past or to be experienced in the future.

This is subject to certain exceptions and which is outside the scope of this article.

Same Example Except No Emergency Medical Condition; PIP Only Pays $2,500

If the hospital does not state that you have an “emergency medical condition”, your car insurance will only pay the hospital $2,500. You would owe the hospital $2,500.

Example #2: $15,000 hospital or doctor bill

You were driving a car or were a passenger in a car involved in a car accident, and the other driver received a ticket for careless driving.

Your hospital bill is in the amount of $15,000.00. Let’s say that the hospital states that you have an emergency medical condition. In this case, your car insurance will pay the hospital $10,000.

PIP Pays = 80% x total bill

= 80% x 15,000

= $12,000

Here, PIP will pay $12,000.

But PIP Only Pays Up to $10K

You would then owe the hospital $5,000. If you want to make a claim for lost wages from your car insurance policy, your auto insurance company will not pay you anything because your PIP insurance is exhausted.

You can make a claim against the at fault driver’s bodily injury (BI) liability insurance for the outstanding medical bills of $5,000 in addition to lost wages and pain and suffering.

If the hospital does not state that you have an emergency medical condition”, your car insurance will only pay the hospital $2,500. You would then owe the hospital $10,000.

You can make a claim against the at fault driver’s BI liability insurance for the outstanding medical bills $10,000 in addition to lost wages and pain and suffering.

Parent, Not the Child, Has the Claim for Medical Bills

The minor’s parents are entitled to get compensation for the reasonable value of hospitalization and medical care for the child from the date of the crash until the child reaches the age of (legal age). The current legal age is 18.

In Wilkie v. Roberts, 91 Fla. 1064, 109 So. 225, 227 (1926), the court said the father could recover medical expenses for the child’s medical treatment. The father’s right of to bring a lawsuit is separate from the child’s right.

Once the child turns 18, all medical bills incurred from that date forward are the child’s responsibility.

How a PIP Deductible Works in a Florida Auto Accident Case

When Won’t PIP Pay Your Medical Bills? (Issues with Application, Etc.)

The most common reasons for a PIP insurer refusing to pay your medical bills are:

The name insured made a material misrepresentation in the auto insurance policy application.

The name insured and/or you failed to cooperate with the PIP insurers investigation. (This may include failing to attend an examination under oath or attend an independent medical examination (IME).

You did not receive medical treatment within the fourteen (14) days following the accident.

A doctor does not state, in writing, that you had an emergency medical condition.

The PIP policyholder failed to tell the PIP insurer about additional people who reside in the household after the policy was purchased.

The medical bills are not related to your injuries from the accident. (The PIP insurer may argue this in a minor impact collision.)

The medical treatment is not necessary.

The medical provider did not submit your medical bills to the PIP insurer within the applicable time frame.

Tip: The medical provider may be able to sue the PIP insurer. A jury will then decide if a PIP insurer should’ve paid the medical bills.

Medical Payments Coverage (“Medpay”)

If you’re an insured under an auto insurance policy with Medical Payments (“Medpay”) coverage, it may pay any bills that PIP doesn’t pay up. It pays up to the Medpay limit on the policy.

Will Workers’ Compensation Pay Your Medical Bills from a Florida Car Accident?

Other First Party Coverage (e.g. Health insurance, Medicare, Medicaid, etc.)

You should use any available first party coverage to pay your medical bills. Health insurance, Medicare and Medicaid are secondary to any PIP coverage to which you are an insured and which PIP should pay.

This means that PIP should be billed and pay your medical providers before the health insurance, Medicaid or Medicare is billed and pays.

After PIP pays the maximum policy limits, you are responsible for paying the medical provider’s full reasonable charges. Florida Statute 627.736(5)(a)4.

(This assumes that you don’t have health insurance.) You don’t get the benefit of any discounted rate that your doctor must accept from PIP.

Health Insurance Pays Medical Bills After PIP Pays

Once PIP pays a medical bill from a Florida car or truck crash, the medical provider (e.g. hospital, ambulance, ER physicians, etc.) should submit the medical bill to the health insurer.

PIP may pay more than the health insurer’s allowable rate. You can find the health insurer’s allowable rate by looking at the explanation of benefits (EOB) that they are required to send you.

If PIP pays more than the health insurer’s allowable rate, the medical provider should waive the balance.

Why must the medical provider waive the balance?

Because the injured person should not penalized (financially) because he/she was an insured under a PIP policy that paid benefits.

Medical Provider Should Bill Health Insurer After PIP is exhausted

Once PIP is exhausted (used up), the medical provider should immediately bill the health insurer. You should be sure to immediately send your health insurer a letter from the PIP insurer stating that PIP is exhausted.

I’ve had many clients who did not give the hospital and/or doctor both their auto and their first party coverage at the time of their medical visit.

Sometimes, by the time the first party coverage provider receives the medical bill, they deny the bill due to it being submitted too late. If that happens, the patient may be stuck owing the bill. The patient can send an appeal to his or her health insurer.

If Rob got medical treatment at the hospital, the hospital may have billed Rob’s health insurer. However, Rob’s health insurer may deny paying the hospital.

They may deny paying because the hospital likely checked the Auto Accident box when they billed your health insurance company.

Your health insurance company may then require that the hospital resubmit its bill with a primary explanation of benefits (EOB) from your car insurance company.

In this case, an explanation of benefits (commonly referred to as an EOB form) is a statement sent by a car insurance company to covered individuals explaining what medical treatments were paid for on their behalf.

However, here, there is no primary car insurance company to bill. To get his health insurance to pay the hospital bill, Rob can file a grievance against his health insurance company.

However, some “health insurers” like some Medicaid plans may take up to 90 days to respond to a grievance. That is a long time to get the hospital bill paid.

Thus, it can delay Rob’s personal injury settlement. And that’s not an option because Rob wants to get his money. Pronto.

This will get another set up eyes, at the health insurance company, to look at his claim. Hopefully, it will quickly get the health insurer to quickly pay the hospital bill.

Then Rob will know how much he has to reimburse (pay back) his health insurer. Likewise, he will know how much his case is worth. Then, he can settle his injury case with the careless driver’s insurer.

What Happens if You Own a Car in Florida That Wasn’t Insured, and Your Hurt in an Accident in Florida?

I Owned a Car But Didn’t Have Auto Insurance. I Was Driving My Employer’s Vehicle. Does My Employer’s PIP Have to Pay My Bills?

No. If you let your car insurance expire, or simply didn’t have your car insured, you cannot get PIP benefits from your employer’s vehicle that you were driving at the time of the crash. You can still make a workers’ compensation claim.

In some counties in Florida, if you owned an uninsured car and were in a crash, the at fault driver owes you 100% of your medical bills. These counties include Pasco, Pinellas, Hardee, Highlands, Polk, DeSoto, Manatee, Sarasota, Hendry, Hillsborough, Charlotte, Glades, Collier, Lee, Hernando, Lake, Marion, Citrus, Sumter, Flagler, Putnam, St. Johns and Volusia Counties, Orange, Osceola Counties, Brevard and Seminole.

In other counties, if you owned an uninsured car and were in an accident, the at fault driver gets a PIP credit on the first $10,000 of your medical bills. This is true even if you weren’t in your own car at the time of the accident. These counties include Miami-Dade, Monroe County, Palm Beach, Broward, St. Lucie, Martin, Indian River, and Okeechobee Counties.

In these counties, since the at fault driver gets a PIP credit, the at fault driver will owe you much less for your medical bills (and lost wages). Expect GEICO or any other car insurer to use this defense. This argument decreases settlement value of your personal injury case.

Will Medicare Pay Medical Bills from a Car Accident?

You may face criminal penalties, the loss of your Medicare benefits and/or Social Security if you do not satisfy Medicare’s lien after a car or truck crash after you reach a personal injury settlement.

Do medical providers have to bill Medicaid in car accident cases?

Repaying Medicaid After a Florida Car or Truck Accident

If settle your personal injury case and you try to stiff Florida Medicaid on the bills that they paid, you could face criminal penalties, and lose your Supplemental Security Income (SSI) and Medicaid benefits.

If someone else’s carelessness caused your injury, you can sue them for any bills that PIP doesn’t pay.

Florida law allows you to recover “the reasonable value or expense of hospitalization and medical and nursing care and treatment necessarily or reasonably obtained by the injured person in the past or to be so obtained in the future.” Fla. Std. Jury Instructions (Civil) 6.2b.

Ticketed Driver Doesn’t Always Have to Pay Your Bills

In Florida, the driver who was received a ticket for causing the crash is not automatically responsible for all of your medical bills.

The potential defendants are liable for the 20% of your medical bills that PIP doesn’t pay up to $10,000 if their negligence caused your injuries. If you want the potential defendants to pay 20% of your medical bills up to $10,000, you have to set up a claim with them.

The potential defendants may be liable for 100% of your damages – above the $10,000 – if their negligence caused your injury.

Do Hospitals Have a Lien on a Personal Injury Settlement?

In many counties in Florida, the hospital will be entitled to a lien on your personal injury settlement against the party whose negligence caused your injury. This may determine how easy or tough it will be to negotiate your outstanding balance with the hospital.

For example, in Miami-Dade County, the hospital is entitled to the reasonable value of its bill from your personal injury settlement.

On the other hand, if you treated at Health Care District of Palm Beach County, it’s Charter caps its lien at 2/3 of the net settlement remaining after your injury attorney’s fees. Other hospitals may have different lien rights.

Uninsured Motorist (UM) Insurance May Pay Your Medical Bills

If another driver’s carelessness caused your injury, then any policies of UM coverage to which you are an insured should pay for medical bills that aren’t paid under workers compensation, PIP, Medpay, or BI coverage.

What Other Personal Injury Compensation Can You Get?

We want to represent you if you were injured in an accident in Florida, on a cruise ship or boat. If you live in Florida but were injured in another state we may also be able to represent you.

Editor’s Note: This post was originally published on March 2013 and I update it from time to time.

Related

I will not become your attorney by you leaving a comment. There is a time limit to file a lawsuit. All comments will be public. This includes the name that you enter. I only represent people who were hurt in Florida or on a cruise ship; or if the injured person lives in Florida or a family member (in the case of a death) lives in Florida. This is because I am only licensed in Florida.

Comments

flowsays

i was wondering who would be in charge of paying my bill if i have back pain after a car accident?

i was recently in a car accident i was going straight and the other car that was coming had a stop sign he said he did not notice it and his car hit the car i was driving and my body went forward and came back to hitting the chair i did not hit the steering wheel ever since that time i been having back problem

Thanks for asking your question. I assume that your accident happened in Florida, which is where I am licensed to practice law. My answer only applies to an accident in Florida. I am not your attorney. This is not legal advice. There is a time limit to file a lawsuit. Before I give my response, I want to say that there are many, many exceptions to my answer. Florida car accident cases can be very complex.

My answer assumes that you were not driving a taxi at the time of the accident.

My answer also assumes that you were a resident of Florida at the time of the crash.

If you owned a car at the time of the accident, then you should give your auto and health insurance to any medical providers that you treat with. Your PIP coverage in your auto insurance policy may pay your medical providers up to $10,000, and possibly more if you have extended PIP, for medical bills. If you have medical payments coverage on your auto policy, that may cover the percentage that PIP does not pay.

If you did not own a car, then the PIP & Medpay coverage of a resident relative’s auto insurance policy may cover your medical bills. If you did not own a car or live with a resident relative at the time of the crash, then the PIP coverage of the vehicle that you were driving may pay for your medical bills.

It sounds to me like that other driver was at fault for causing the accident. Did he receive a ticket for causing the accident? You should also make a claim against the bodily injury coverage, if he has any, of his auto insurance for your medical bills as well as other damages. His bodily injury coverage, if he has any, may pay for some of your medical bills as well if he was at fault.

If the other driver was driving someone else’s car, was driving with a learner’s permit, working or performing an errand at the time of the accident, then the owner, employer, person who directed the errand, volunteering agency, person who signed for a learner’s permit, etc. may be responsible for paying your medical bills that PIP adoesn’t cover. There are also additional parties that could be responsible for your medical bills.

I will not get into making a claim for pain and suffering and other damages that you may be entitled to because you have not asked about that.

Have you received medical treatment? If so, what are your injuries?

Call me now at (888) 594-3577 to Get a Free Consultation. There are No Fees or Costs Unless We Recover Money. We accept calls 365 days a year, 7 days a week, 24 hours a day. We also speak Spanish.

Person in car accident who has pain and sorenesssays

I was recently involved in a car accident (in Florida) it was the other drivers fault and they received the tickets. However this person had no insurance I was released from the hospital and now want to follow up with a doctor for I am badly bruised and very sore all over. I am concerned over my chest still hurting ….. This is now day 4…… My question. Is the person who caused the accident still responsible even though they don’t have insurance ….. I have a $500 collision deductible also I will be owing 20% on my car rental bill Have not returned to work yet too much pain and soreness How does this work?

Dear Person who was in a car accident and has pain and soreness:

Thank you for telling me about your accident. I am sorry to hear that you were injured. I hope you feel better.

Unfortunately, I cannot answer your question here. If you want to hire a lawyer, you are more than welcome to call us at 888-594-3577 and we will tell you – for free – whether we can represent you. I suggest that you speak with an attorney immediately. There are at least 11 reasons and benefits to hiring an injury lawyer.

There is a time limit to file a lawsuit. I am not your attorney. This is not legal advice.

I was recently involved in an accident where the driver of another vehicle rear ended my car. He admitted fault, the officer issue him a ticket, the police report cites him at fault, and his insurance company that can be mistaken as gecko has admitted on a recorded statement that they have accepted fault for their driver. My lower and mid back, as well as my neck, sustained injury and I have been sore for a week. I have not seen a doctor or chiropractor because my insurance company told me that I would be liable for the $1000 PIP deductible before insurance pays 80% of the remaining $9,000. I understand that Florida is a “No-Fault” state, but that’s a bunch of bologna. How is it just or fair that this other driver wasn’t paying attention and hit my vehicle, yet I am the one who has to pay for it even though he has insurance too? If he hadn’t hit me, I would not have the injury. I do not feel I should have to pay a dime under the circumstances. What can I do? I can not afford the deductible, much less 20% of the remaining $9000, not do I feel I should have to. However, I need to get checked out because I am sore and it is really effecting my ability to perform my job. Any advice is appreciated. I am in Duval County in North Florida and I do not have medical coverage.

In Florida, you’re entitled to recover your out of pocket medical bills (and other damages) if the the careless driver’s negligence caused your out of pocket medical expenses. So taking the facts as you state them, the careless driver or any liable party should be responsible for your out of pocket medical bills that are related to the crash.

The careless driver or any liable party can contest the reasonableness and relatedness of your medical bills.

Fortunately, there are many doctors who will treat you on the condition (via written agreement) that they are paid any outstanding balance from the personal injury settlement.

My answer was a very oversimplified answer to your question.

I accept car accident cases for people who live in Duval County, North Florida and throughout the entire state. You can call us at 305-661-9977 to see if I can represent you.

You should speak with a personal injury lawyer immediately. There is a time limit to sue or your claim is forever barred. This is not legal advice. I am not your lawyer.

The information you provided above states that health insurance may be able to cover the remaining 20% of medical bills that the 80% provided by PIP does not, however you also state “PIP may pay more than the health insurer’s approved rate. If PIP pays more than the health insurer’s approved rate, the medical provider should waive the balance.”

In my case my health insurer has stated that because PIP paid out more than the allowable billable amount for my emergency ambulance ride, they will not pay the remainder of the claim for the ride. Is there a Florida statute that speaks to this situation? And how would I get the medical provider (ambulance) to waive the balance?

Firstly, the article should’ve said allowable amount, not “approved rate.” I’ve changed it.

I don’t know if a Florida Statute addresses this situation. I also don’t know if Florida case law addresses it. I also don’t know what the health insurance policy says.

I would have to do legal research. Unfortunately, since you are not a client of mine, I am unable to research it. If you find a statute or law that address this, please let me know.

That said, I would ask the ambulance to waive the balance based on the fact that the PIP paid more than the health insurance company’s allowable rate. Of course, I’d make sure that the ambulance company also billed the health insurance and any other available insurance.

How much money does the health insurer say that you owe the ambulance company?

How money does the ambulance company say that you owe them?

If it was a significant amount of money, I’d ask the health insurer to cite the insurance policy provision or law that they believe doesn’t require them to pay the outstanding balance with the ambulance provider.

If they are incorrect, you can take action against the party(ies) who are incorrect.

My reply only applies to accidents in Florida, which is where I’m licensed.

I wish you good luck. Most importantly, I hope that you feel better.

Disclaimer: My reply is written for general information only. Individual cases demand individual treatment. I am not your lawyer. My reply is not intended as legal advice or opinion. You should speak with a lawyer immediately.

There is a time limit to sue and/or appeal a claim. If you miss the time limit, you forever lose your right to sue or appeal a claim(s).

I am not expressing any opinion on your particular case.

i was wondering who would be in charge of paying my bill if i have back pain after a car accident?

i was recently in a car accident i was going straight and the other car that was coming had a stop sign he said he did not notice it and his car hit the car i was driving and my body went forward and came back to hitting the chair i did not hit the steering wheel ever since that time i been having back problem

the accident was on the 15th of January

Hi Flow,

Thanks for asking your question. I assume that your accident happened in Florida, which is where I am licensed to practice law. My answer only applies to an accident in Florida. I am not your attorney. This is not legal advice. There is a time limit to file a lawsuit. Before I give my response, I want to say that there are many, many exceptions to my answer. Florida car accident cases can be very complex.

My answer assumes that you were not driving a taxi at the time of the accident.

My answer also assumes that you were a resident of Florida at the time of the crash.

If you owned a car at the time of the accident, then you should give your auto and health insurance to any medical providers that you treat with. Your PIP coverage in your auto insurance policy may pay your medical providers up to $10,000, and possibly more if you have extended PIP, for medical bills. If you have medical payments coverage on your auto policy, that may cover the percentage that PIP does not pay.

If you did not own a car, then the PIP & Medpay coverage of a resident relative’s auto insurance policy may cover your medical bills. If you did not own a car or live with a resident relative at the time of the crash, then the PIP coverage of the vehicle that you were driving may pay for your medical bills.

It sounds to me like that other driver was at fault for causing the accident. Did he receive a ticket for causing the accident? You should also make a claim against the bodily injury coverage, if he has any, of his auto insurance for your medical bills as well as other damages. His bodily injury coverage, if he has any, may pay for some of your medical bills as well if he was at fault.

If the other driver was driving someone else’s car, was driving with a learner’s permit, working or performing an errand at the time of the accident, then the owner, employer, person who directed the errand, volunteering agency, person who signed for a learner’s permit, etc. may be responsible for paying your medical bills that PIP adoesn’t cover. There are also additional parties that could be responsible for your medical bills.

I will not get into making a claim for pain and suffering and other damages that you may be entitled to because you have not asked about that.

Have you received medical treatment? If so, what are your injuries?

Call me now at (888) 594-3577 to Get a Free Consultation. There are No Fees or Costs Unless We Recover Money. We accept calls 365 days a year, 7 days a week, 24 hours a day. We also speak Spanish.

I was recently involved in a car accident (in Florida) it was the other drivers fault and they received the tickets. However this person had no insurance I was released from the hospital and now want to follow up with a doctor for I am badly bruised and very sore all over. I am concerned over my chest still hurting ….. This is now day 4…… My question. Is the person who caused the accident still responsible even though they don’t have insurance ….. I have a $500 collision deductible also I will be owing 20% on my car rental bill Have not returned to work yet too much pain and soreness How does this work?

Dear Person who was in a car accident and has pain and soreness:

Thank you for telling me about your accident. I am sorry to hear that you were injured. I hope you feel better.

Unfortunately, I cannot answer your question here. If you want to hire a lawyer, you are more than welcome to call us at 888-594-3577 and we will tell you – for free – whether we can represent you. I suggest that you speak with an attorney immediately. There are at least 11 reasons and benefits to hiring an injury lawyer.

There is a time limit to file a lawsuit. I am not your attorney. This is not legal advice.

I was recently involved in an accident where the driver of another vehicle rear ended my car. He admitted fault, the officer issue him a ticket, the police report cites him at fault, and his insurance company that can be mistaken as gecko has admitted on a recorded statement that they have accepted fault for their driver. My lower and mid back, as well as my neck, sustained injury and I have been sore for a week. I have not seen a doctor or chiropractor because my insurance company told me that I would be liable for the $1000 PIP deductible before insurance pays 80% of the remaining $9,000. I understand that Florida is a “No-Fault” state, but that’s a bunch of bologna. How is it just or fair that this other driver wasn’t paying attention and hit my vehicle, yet I am the one who has to pay for it even though he has insurance too? If he hadn’t hit me, I would not have the injury. I do not feel I should have to pay a dime under the circumstances. What can I do? I can not afford the deductible, much less 20% of the remaining $9000, not do I feel I should have to. However, I need to get checked out because I am sore and it is really effecting my ability to perform my job. Any advice is appreciated. I am in Duval County in North Florida and I do not have medical coverage.

Speakingnvowels:

Thank you for your comment. I’m sorry to hear that you were hurt.

Unfortunately, not all of Florida personal injury laws are fair. Florida’s no fault laws go against intuition, and they are strange.

Warning! There is a very short time period for you to get medical treatment after the car crash, otherwise your PIP won’t pay your medical bills.

In Florida, you’re entitled to recover your out of pocket medical bills (and other damages) if the the careless driver’s negligence caused your out of pocket medical expenses. So taking the facts as you state them, the careless driver or any liable party should be responsible for your out of pocket medical bills that are related to the crash.

The careless driver or any liable party can contest the reasonableness and relatedness of your medical bills.

Fortunately, there are many doctors who will treat you on the condition (via written agreement) that they are paid any outstanding balance from the personal injury settlement.

My answer was a very oversimplified answer to your question.

I accept car accident cases for people who live in Duval County, North Florida and throughout the entire state. You can call us at 305-661-9977 to see if I can represent you.

You should speak with a personal injury lawyer immediately. There is a time limit to sue or your claim is forever barred. This is not legal advice. I am not your lawyer.

The information you provided above states that health insurance may be able to cover the remaining 20% of medical bills that the 80% provided by PIP does not, however you also state “PIP may pay more than the health insurer’s approved rate. If PIP pays more than the health insurer’s approved rate, the medical provider should waive the balance.”

In my case my health insurer has stated that because PIP paid out more than the allowable billable amount for my emergency ambulance ride, they will not pay the remainder of the claim for the ride. Is there a Florida statute that speaks to this situation? And how would I get the medical provider (ambulance) to waive the balance?

Confused by the System:

Thank you for your comment.

Firstly, the article should’ve said allowable amount, not “approved rate.” I’ve changed it.

I don’t know if a Florida Statute addresses this situation. I also don’t know if Florida case law addresses it. I also don’t know what the health insurance policy says.

I would have to do legal research. Unfortunately, since you are not a client of mine, I am unable to research it. If you find a statute or law that address this, please let me know.

That said, I would ask the ambulance to waive the balance based on the fact that the PIP paid more than the health insurance company’s allowable rate. Of course, I’d make sure that the ambulance company also billed the health insurance and any other available insurance.

How much money does the health insurer say that you owe the ambulance company?

How money does the ambulance company say that you owe them?

If it was a significant amount of money, I’d ask the health insurer to cite the insurance policy provision or law that they believe doesn’t require them to pay the outstanding balance with the ambulance provider.

If they are incorrect, you can take action against the party(ies) who are incorrect.

My reply only applies to accidents in Florida, which is where I’m licensed.

I wish you good luck. Most importantly, I hope that you feel better.

Disclaimer: My reply is written for general information only. Individual cases demand individual treatment. I am not your lawyer. My reply is not intended as legal advice or opinion. You should speak with a lawyer immediately.

There is a time limit to sue and/or appeal a claim. If you miss the time limit, you forever lose your right to sue or appeal a claim(s).

I am not expressing any opinion on your particular case.

Great info. Thank you.

You are welcome.

Disclaimer: This article is not legal advice. Always speak with an attorney for your particular situation. There are time limits to sue.